Strategi Take Profit dan Stop Loss Adaptif Berdasarkan Kerangka Waktu Ganda dan Indikator Momentum

Ikhtisar

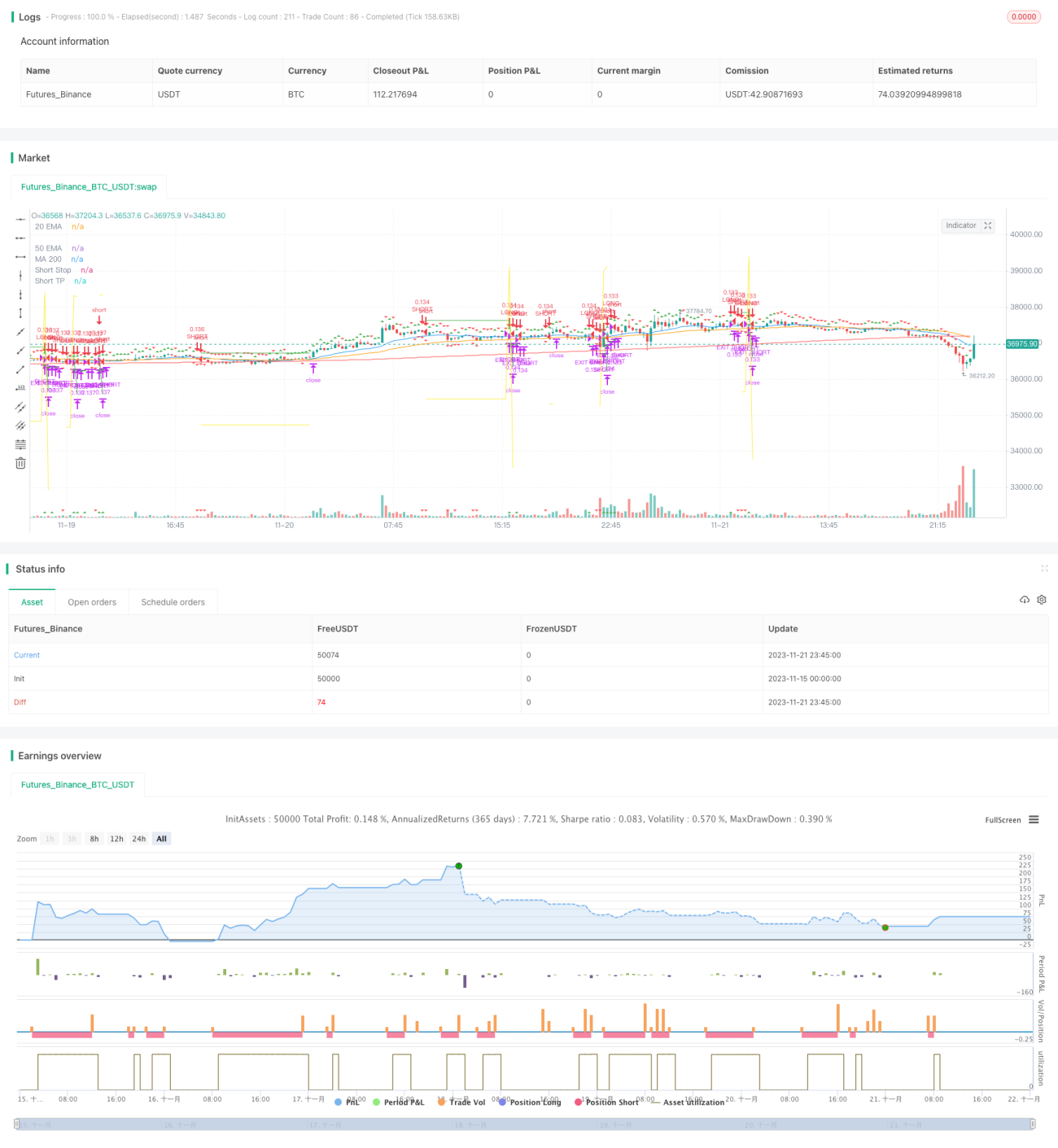

Strategi ini menggunakan kombinasi kerangka waktu ganda dan indikator momentum untuk mencapai take profit dan stop loss yang adaptif. Kerangka waktu utama memantau arah tren, sedangkan kerangka waktu tambahan digunakan untuk mengonfirmasi sinyal. Ketika arah keduanya sejalan, sinyal trading dihasilkan. Setelah masuk pasar, metode take profit progresif digunakan untuk memperbarui level take profit dan stop loss.

Prinsip Strategi

-

Kerangka waktu utama menggunakan indikator regresi linier Squeeze Momentum (SQM) untuk menentukan tren, sedangkan kerangka waktu tambahan menggunakan kombinasi EMA dari indikator SQM untuk menyaring sinyal palsu.

-

Ketika SQM pada grafik utama menembus ke atas dan SQM pada grafik tambahan juga naik, lakukan posisi long; ketika SQM pada grafik utama menembus ke bawah dan SQM pada grafik tambahan juga turun, lakukan posisi short.

-

Setelah masuk, tetapkan level take profit dan stop loss awal berdasarkan parameter input. Ketika harga mencapai level take profit, perbarui level take profit dan stop loss. Caranya: level take profit dinaikkan secara bertahap sesuai rasio yang ditetapkan, sementara level stop loss diturunkan secara bertahap, sehingga tercapai take profit progresif.

Keunggulan Strategi

-

Kerangka waktu ganda menyaring sinyal palsu, memastikan akurasi sinyal.

-

Indikator SQM menentukan arah tren, menghindari gangguan dari kebisingan pasar.

-

Mekanisme take profit dan stop loss adaptif mengunci keuntungan secara maksimal dan mengelola risiko secara efektif.

Analisis Risiko

-

Pengaturan parameter indikator SQM yang tidak tepat dapat menyebabkan terlewatnya titik balik tren, sehingga menimbulkan kerugian.

-

Pemilihan kerangka waktu grafik tambahan yang tidak tepat tidak dapat menyaring kebisingan secara efektif, menghasilkan transaksi yang salah.

-

Jika rentang stop loss diatur terlalu besar, kerugian per perdagangan bisa sangat signifikan.

Arah Optimasi

-

Parameter indikator SQM perlu disesuaikan dengan pasar yang berbeda untuk memastikan sensitivitasnya.

-

Kerangka waktu grafik tambahan juga perlu diuji dengan berbagai periode untuk melihat periode mana yang paling efektif dalam menyaring sinyal.

-

Rentang stop loss dapat diatur sebagai rentang fluktuasi, bukan nilai tetap, sehingga dapat disesuaikan dengan tingkat volatilitas pasar.

Kesimpulan

Secara keseluruhan, strategi ini sangat praktis. Kombinasi kerangka waktu ganda dengan indikator momentum untuk menentukan tren, serta penggunaan metode take profit dan stop loss adaptif, memungkinkan profit yang stabil. Dengan mengoptimalkan parameter indikator SQM, periode grafik tambahan, dan pengaturan rentang stop loss, efektivitas strategi dapat ditingkatkan, sehingga layak untuk diterapkan dan dioptimalkan dalam perdagangan riil.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1