Strategi Pelacakan Piramida Titik Rendah dengan Risiko Rendah

Strategi ini mengidentifikasi titik terendah potensial dalam pergerakan harga dengan menggabungkan berbagai indikator, dan mengurangi risiko dengan membangun posisi secara bertahap menggunakan piramida pelacakan. Strategi ini juga dilengkapi dengan fungsi stop loss, take profit, trailing stop, dll., yang secara efektif dapat mengelola risiko.

Ikhtisar Strategi

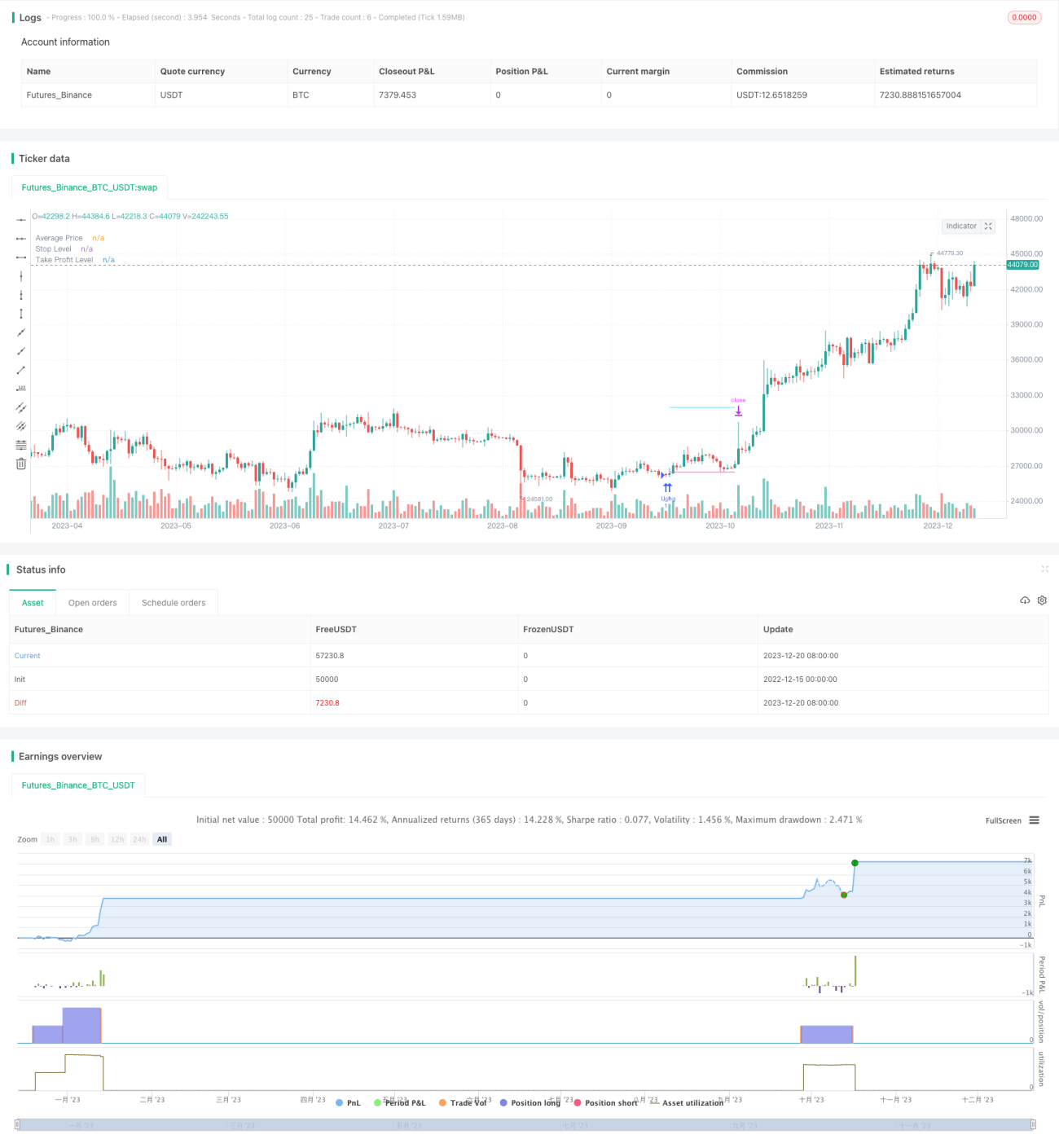

Strategi ini pertama-tama menggunakan selisih antara RSI dan EMA RSI untuk mengidentifikasi titik terendah potensial dalam harga. Untuk menyaring sinyal palsu, strategi ini juga menggabungkan konfirmasi dari moving average dan stochastic multi-timeframe. Setelah sinyal titik terendah dikonfirmasi, posisi long dibangun secara bertahap sedikit di bawah titik tersebut, inilah konsep piramida pelacakan. Strategi ini memungkinkan hingga 12 pesanan pelacakan, di mana jumlah setiap pesanan meningkat secara berurutan, sehingga secara efektif menyebarkan risiko. Semua pesanan keluar mengikuti satu stop loss keseluruhan, dan juga memungkinkan pengaturan take profit terpisah untuk setiap pesanan. Untuk lebih mengendalikan risiko, strategi ini juga menetapkan stop loss keseluruhan berdasarkan persentase ekuitas akun.

Prinsip Strategi

Strategi ini terutama terdiri dari tiga modul: modul identifikasi titik terendah, modul piramida pelacakan, dan modul manajemen risiko.

Modul identifikasi titik terendah menggunakan selisih antara indikator RSI dan EMA-nya untuk mengidentifikasi titik terendah potensial dalam harga. Untuk meningkatkan akurasi, indikator moving average dan stochastic multi-timeframe juga diperkenalkan untuk menyaring sinyal. Sinyal titik terendah hanya akan divalidasi jika harga berada di bawah moving average dan garis K stochastic di bawah 30.

Modul piramida pelacakan adalah inti dari strategi ini. Setelah sinyal titik terendah dikonfirmasi, strategi akan membuka pesanan pertama pada posisi 0,1% lebih rendah dari titik terendah tersebut. Setelah itu, selama harga terus turun dan berada di bawah harga entry rata-rata dengan persentase tertentu, pesanan long tambahan akan terus ditambahkan. Jumlah pesanan baru meningkat secara berurutan, misalnya jumlah pesanan ketiga adalah 3 kali lipat dari pesanan pertama. Metode piramida pelacakan ini dapat meratakan risiko. Strategi ini memungkinkan hingga 12 pesanan pelacakan.

Modul manajemen risiko terutama mencakup tiga aspek. Pertama, stop loss keseluruhan, dihitung berdasarkan harga tertinggi dalam periode tertentu. Semua pesanan akan mengikuti stop loss ini untuk keluar secara bersamaan. Kedua, take profit independen untuk setiap pesanan, yang memungkinkan take profit berdasarkan persentase tertentu dari harga entry. Ketiga, stop loss keseluruhan berdasarkan persentase ekuitas akun, yang merupakan alat manajemen risiko paling kuat.

Keunggulan Strategi

- Mengurangi risiko pesanan individu dan menyebarkan risiko keseluruhan dengan piramida pelacakan

- Kombinasi multi-indikator meningkatkan akurasi identifikasi titik terendah

- Stop loss keseluruhan, take profit, dan trailing stop secara efektif mengelola risiko

- Mekanisme stop loss berdasarkan persentase ekuitas melindungi akun dari kerugian besar

- Dapat menemukan keseimbangan antara risiko dan imbal hasil dengan menyesuaikan parameter

Risiko Strategi

- Akurasi identifikasi titik terendah masih terbatas, dapat melewatkan titik entry optimal atau masuk ke sinyal palsu

- Saat menambah pesanan, mungkin menghadapi pergerakan harga yang tidak menguntungkan, memperberat kerugian

- Membutuhkan periode running yang lebih lama untuk menunjukkan keunggulan strategi

- Pengaturan parameter yang tidak tepat dapat menyebabkan kontrol risiko yang tidak memadai

Untuk mengurangi risiko di atas, optimasi dapat dilakukan dari aspek berikut:

- Mengganti atau menambah indikator untuk meningkatkan akurasi identifikasi titik terendah

- Mengoptimalkan parameter seperti jumlah pesanan, interval, dan besaran take profit untuk mengurangi risiko per pesanan

- Memperpendek rentang stop loss secara tepat untuk melindungi profit

- Menguji berbagai instrumen, pilih instrumen dengan likuiditas baik dan volatilitas tinggi

Arah Optimasi Strategi

Strategi ini masih memiliki ruang untuk optimasi lebih lanjut:

- Mencoba memperkenalkan teknologi yang lebih maju seperti machine learning untuk mengidentifikasi titik terendah

- Menyesuaikan parameter seperti jumlah pesanan dan rentang stop loss secara dinamis berdasarkan kondisi pasar

- Menambahkan strategi stop loss dalam kisaran untuk menghindari kerugian membesar

- Menambahkan mekanisme re-entry

- Mengoptimalkan parameter strategi untuk saham dan mata uang kripto

Kesimpulan

Strategi ini secara efektif mengurangi risiko per pesanan melalui konsep piramida pelacakan, dan fungsi stop loss keseluruhan, take profit, serta trailing stop juga memberikan kontrol risiko yang baik. Namun, masih ada ruang untuk optimasi dalam identifikasi titik terendah. Jika teknologi yang lebih maju dapat diperkenalkan, fungsi penyesuaian parameter dinamis ditambahkan, dan dikombinasikan dengan optimasi parameter, rasio risiko-imbal hasil dari strategi ini akan meningkat secara signifikan.

- 1