Strategi Kombinasi Bollinger Bands Menyusut dan RSI

Ikhtisar

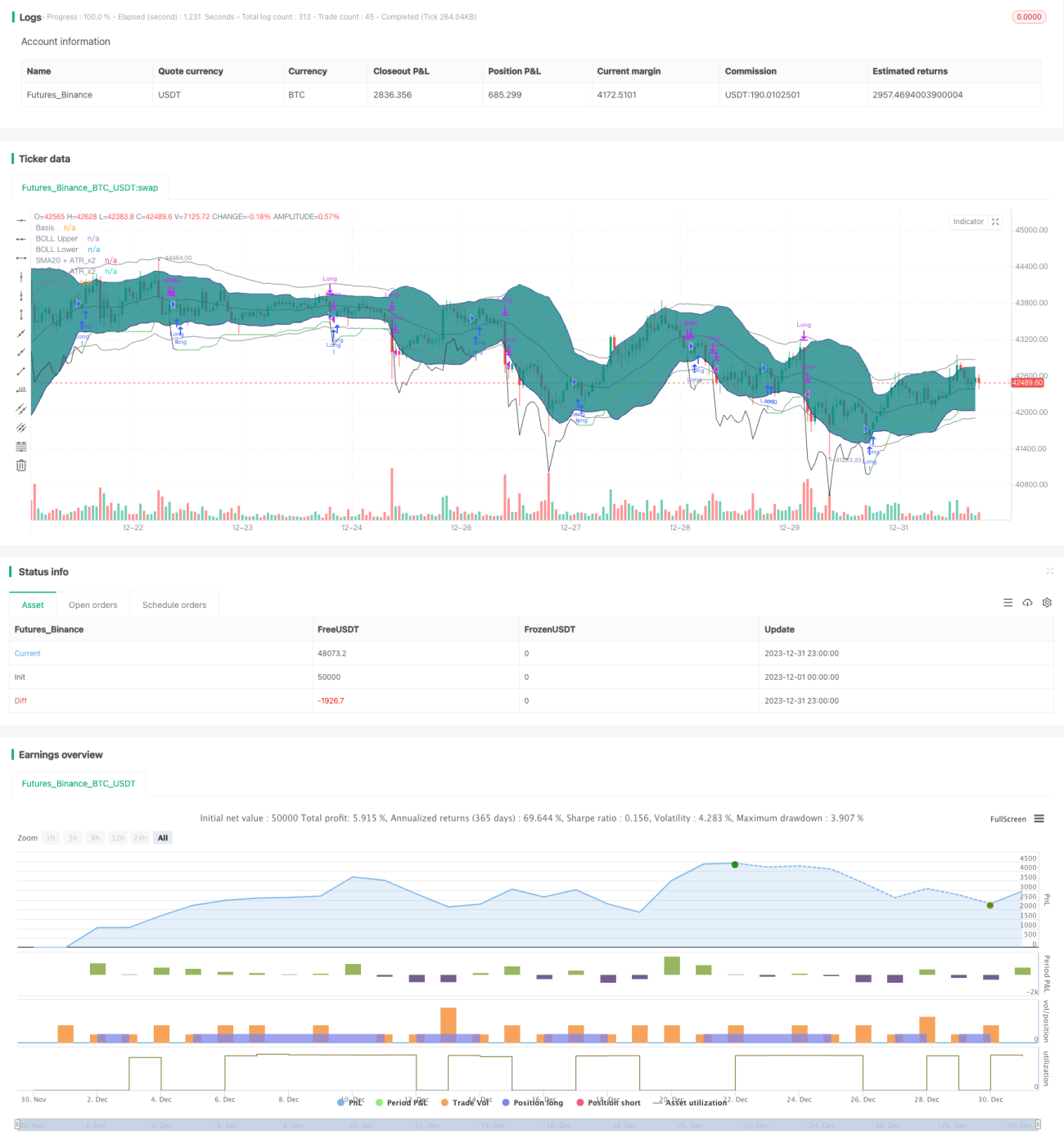

Strategi ini menggabungkan Bollinger Bands dan Relative Strength Index (RSI) untuk mengidentifikasi peluang periode kontraksi Bollinger Bands yang diiringi oleh kenaikan RSI, dan menerapkan stop loss trailing untuk mengendalikan risiko.

Prinsip Strategi

Inti logika perdagangan strategi ini adalah mengidentifikasi kontraksi Bollinger Bands, dan ketika RSI menunjukkan tren naik, menilai bahwa tren berada di tahap awal kenaikan. Secara spesifik, ketika standar deviasi pada jalur tengah Bollinger Bands 20 hari lebih kecil dari ATR*2, kami menilai terjadi kontraksi Bollinger Bands. Sementara itu, jika RSI 10 hari dan 14 hari sama-sama menunjukkan tren naik, maka kami memprediksi harga akan menembus pita atas Bollinger Bands, dan mengambil strategi long.

Setelah masuk pasar, kami menggunakan jarak aman ATR + stop loss yang mengikuti kenaikan harga untuk mengunci keuntungan dan mengendalikan risiko. Ketika harga melampaui garis stop loss atau RSI terlalu panas (RSI 14 hari di atas 70, RSI 10 hari melebihi RSI 14 hari), posisi ditutup.

Analisis Keunggulan

Keunggulan terbesar dari strategi ini adalah menggunakan kontraksi Bollinger Bands untuk menilai periode konsolidasi pasar, dikombinasikan dengan indikator RSI untuk memprediksi arah breakout harga. Selain itu, penggunaan stop loss adaptif alih-alih stop loss tetap memungkinkan penyesuaian fleksibel berdasarkan volatilitas pasar, sehingga memperoleh keuntungan lebih besar dengan tetap menjaga risiko yang terkendali.

Analisis Risiko

Risiko utama dari strategi ini adalah ketika mengidentifikasi kontraksi Bollinger Bands dan kenaikan RSI, pergerakan harga mungkin merupakan breakout palsu. Selain itu, dalam hal stop loss, ketika volatilitas terlalu tinggi, stop loss adaptif mungkin tidak dapat menghentikan kerugian tepat waktu. Risiko ini dapat dikurangi dengan memperbaiki metode stop loss (misalnya stop loss kurva).

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

- Memperbaiki pengaturan parameter Bollinger Bands, mengoptimalkan efek penilaian kontraksi.

- Mencoba parameter periode RSI yang berbeda.

- Menguji efektivitas metode stop loss lainnya (stop loss kurva, stop loss lookback, dll.)

- Menyesuaikan parameter sesuai dengan karakteristik instrumen yang berbeda.

Kesimpulan

Strategi ini secara komprehensif memanfaatkan sifat komplementer dari Bollinger Bands dan RSI, memperoleh rasio drawdown terhadap keuntungan yang baik dengan tetap mengendalikan risiko. Selanjutnya dapat dioptimalkan dari segi metode stop loss, pemilihan parameter, dll., sehingga strategi lebih cocok untuk berbagai instrumen perdagangan.

- 1