Strategi Trading Breakout Dua Arah Berdasarkan Candlestick

Ikhtisar

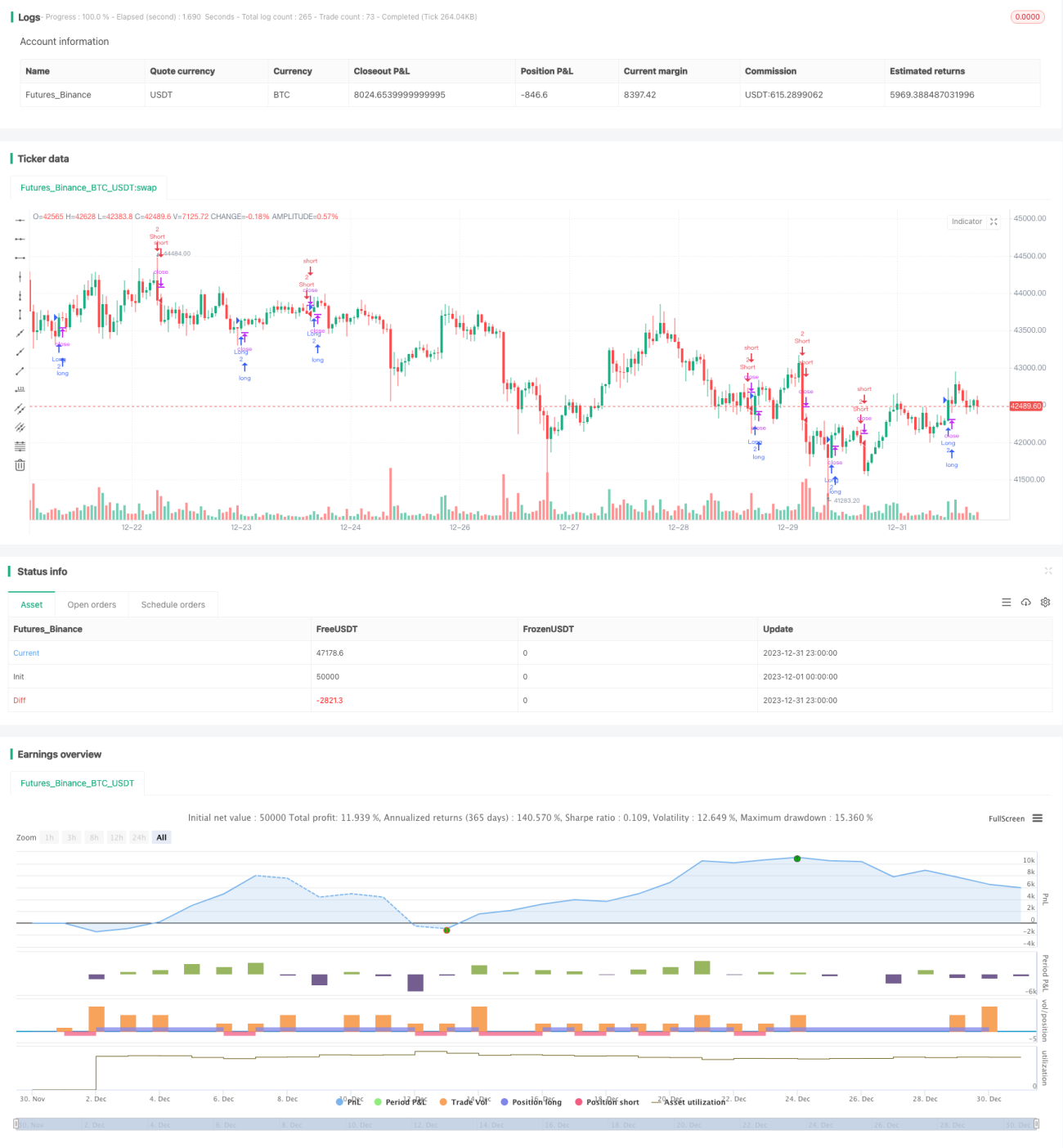

Ini adalah strategi trading breakout dua arah berdasarkan candlestick. Strategi ini akan menghasilkan sinyal trading ketika harga penutupan candlestick saat ini menembus harga tertinggi dan terendah dari dua candlestick sebelumnya.

Prinsip Strategi

Logika dasar dari strategi ini adalah:

-

Mendefinisikan sinyal bullish:

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]. Artinya, harga penutupan candlestick saat ini lebih besar dari harga pembukaan, dan lebih besar dari harga tertinggi dua candlestick sebelumnya, sedangkan harga terendah candlestick saat ini lebih rendah dari harga terendah candlestick sebelumnya. -

Mendefinisikan sinyal bearish:

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]. Artinya, harga penutupan candlestick saat ini lebih kecil dari harga pembukaan, dan lebih kecil dari harga terendah dua candlestick sebelumnya, sedangkan harga tertinggi candlestick saat ini lebih tinggi dari harga tertinggi candlestick sebelumnya. -

Ketika sinyal bullish terpicu, lakukan long; ketika sinyal bearish terpicu, lakukan short.

-

Dapat mengatur level stop loss dan take profit.

Strategi ini memanfaatkan karakteristik breakout dua arah, dengan menembus range harga kunci untuk menentukan perubahan tren, sehingga menghasilkan sinyal trading.

Analisis Keunggulan

Ini adalah strategi breakout yang relatif sederhana dan intuitif, dengan keunggulan sebagai berikut:

-

Logika jelas, mudah dipahami dan diimplementasikan, dengan ambang batas yang rendah.

-

Breakout adalah sinyal trading yang umum, mudah membentuk tren.

-

Dapat melakukan long dan short secara bersamaan, memungkinkan trading dua arah untuk meningkatkan peluang profit.

-

Dapat mengatur stop loss dan take profit secara fleksibel untuk mengendalikan risiko.

Analisis Risiko

Strategi ini juga memiliki beberapa risiko:

-

Risiko trading dua arah cukup besar, memerlukan pemantauan ketat.

-

Breakout rentan terhadap jebakan, dapat menghasilkan sinyal palsu.

-

Pengaturan parameter yang tidak tepat dapat menyebabkan overtrading.

-

Pengaturan stop loss dan take profit yang tidak tepat juga dapat mempengaruhi ruang profit.

Dapat mengoptimalkan parameter dan memilih instrumen yang sesuai untuk mengurangi risiko.

Arah Optimasi

Strategi ini dapat dioptimalkan dari beberapa aspek berikut:

-

Mengoptimalkan parameter, seperti periode breakout, besaran stop loss/take profit, dll.

-

Menambahkan kondisi filter untuk menghindari sinyal salah pada kondisi ranging atau sideway.

-

Menggabungkan indikator tren untuk menghindari rentang konsolidasi.

-

Mengoptimalkan manajemen modal, memperbaiki algoritma posisi.

-

Parameter berbeda untuk instrumen yang berbeda, dapat diuji dan dioptimalkan secara terpisah.

Kesimpulan

Ini adalah strategi sederhana berdasarkan ide breakout dua arah. Memiliki keunggulan logika yang jelas dan mudah diimplementasikan, namun juga memiliki risiko pemantauan tertentu. Dengan optimasi parameter dan kondisi, diharapkan dapat mencapai hasil strategi yang lebih baik.

- 1