Strategi Kuberan: Strategi Konfluensi Penguasaan Pasar

Ikhtisar Strategi

Strategi Kuberan adalah strategi perdagangan yang kuat yang ditulis oleh Kathir. Strategi ini menggabungkan berbagai teknik analisis untuk membentuk pendekatan perdagangan yang unik dan kuat. Dinamai berdasarkan dewa kekayaan Kuberan, strategi ini melambangkan tujuannya untuk memperkaya portofolio para trader.

Kuberan bukan sekadar strategi, tetapi merupakan sistem perdagangan yang komprehensif. Ia menggabungkan analisis tren, indikator momentum, dan indikator volume untuk mengidentifikasi peluang perdagangan dengan probabilitas tinggi. Dengan memanfaatkan sinergi elemen-elemen ini, Kuberan memberikan sinyal masuk dan keluar yang jelas yang cocok untuk trader dari berbagai tingkat keahlian.

Prinsip Strategi

Inti dari strategi Kuberan adalah prinsip konvergensi multi-indikator. Ia menggunakan kombinasi indikator unik yang saling melengkapi untuk mengurangi noise dan sinyal palsu. Secara spesifik, strategi ini menggunakan beberapa komponen kunci berikut:

- Penentuan Arah Tren: Menentukan arah tren saat ini dengan membandingkan harga saat ini dengan level support dan resistance.

- Level Support dan Resistance: Mengidentifikasi level support dan resistance kunci melalui indikator zigzag dan titik pivot.

- Deteksi Divergensi: Mendeteksi divergensi dengan membandingkan pergerakan harga dengan indikator momentum, yang mengindikasikan potensi pembalikan tren.

- Adaptasi Volatilitas: Menyesuaikan level stop loss secara dinamis menggunakan indikator ATR untuk beradaptasi dengan volatilitas pasar yang berbeda.

- Identifikasi Pola Candlestick: Mengkonfirmasi sinyal tren dan pembalikan melalui kombinasi pola candlestick tertentu.

Dengan mempertimbangkan faktor-faktor di atas secara komprehensif, strategi Kuberan dapat beradaptasi secara dinamis di berbagai kondisi pasar, menangkap peluang perdagangan dengan probabilitas tinggi.

Keunggulan Strategi

- Konvergensi Multi-Indikator: Strategi Kuberan memanfaatkan sinergi dari beberapa indikator, secara signifikan meningkatkan keandalan sinyal dan mengurangi gangguan noise.

- Adaptabilitas Tinggi: Dengan menyesuaikan parameter secara dinamis, strategi ini mampu beradaptasi dengan kondisi pasar yang selalu berubah dan tidak mudah gagal.

- Sinyal Jelas: Kuberan memberikan sinyal masuk dan keluar yang jelas, menyederhanakan proses pengambilan keputusan perdagangan.

- Backtest yang Kokoh: Strategi ini telah melalui pengujian ulang historis yang ketat dan menunjukkan kinerja yang stabil di berbagai kondisi pasar.

- Cakupan Luas: Kuberan berlaku untuk berbagai pasar dan instrumen, tidak terbatas pada aset perdagangan tertentu.

Risiko Strategi

- Sensitif terhadap Parameter: Kinerja strategi Kuberan cukup sensitif terhadap pemilihan parameter; parameter yang tidak tepat dapat menyebabkan penurunan kinerja.

- Kejadian Tak Terduga: Strategi ini terutama didasarkan pada sinyal teknis, sehingga kemampuannya untuk merespons kejadian fundamental mendadak terbatas.

- Risiko Overfitting: Jika terlalu banyak data historis dipertimbangkan selama optimasi parameter, strategi mungkin terlalu sesuai dengan masa lalu dan kurang adaptif terhadap pergerakan pasar masa depan.

- Risiko Leverage: Jika leverage yang terlalu tinggi digunakan, terdapat risiko likuidasi saat menghadapi penarikan (drawdown) yang besar.

Untuk mengatasi risiko-risiko di atas, langkah-langkah pengendalian yang tepat dapat diambil, seperti menyesuaikan parameter secara berkala, menetapkan stop loss yang wajar, mengontrol leverage secara moderat, dan memperhatikan perubahan fundamental.

Arah Optimasi

- Optimasi Pembelajaran Mesin: Algoritma pembelajaran mesin dapat diperkenalkan untuk mengoptimalkan parameter strategi secara dinamis, meningkatkan adaptabilitas.

- Memasukkan Faktor Fundamental: Pertimbangkan untuk mengintegrasikan analisis fundamental ke dalam pengambilan keputusan perdagangan guna mengatasi situasi di mana sinyal teknis gagal.

- Manajemen Portofolio: Pada tingkat manajemen modal, strategi Kuberan dapat dimasukkan ke dalam portofolio, membentuk lindung nilai yang efektif dengan strategi lain.

- Optimasi Spesifik Pasar: Sesuaikan dan optimalkan parameter strategi berdasarkan karakteristik instrumen pasar yang berbeda.

- Konversi Frekuensi Tinggi: Ubah strategi menjadi versi perdagangan frekuensi tinggi untuk menangkap lebih banyak peluang perdagangan jangka pendek.

Kesimpulan

Kuberan adalah strategi perdagangan yang kuat, aman, dan andal. Ia dengan cerdik menggabungkan berbagai metode analisis teknis, dan melalui prinsip konvergensi indikator, unggul dalam menangkap tren dan mengidentifikasi titik balik. Meskipun strategi apa pun tidak luput dari risiko, Kuberan telah membuktikan ketangguhannya dalam backtest. Dengan pengendalian risiko dan langkah-langkah optimasi yang tepat, strategi ini diyakini dapat membantu para trader menguasai keunggulan dalam permainan pasar dan mendorong pertumbuhan portofolio yang stabil dalam jangka panjang.

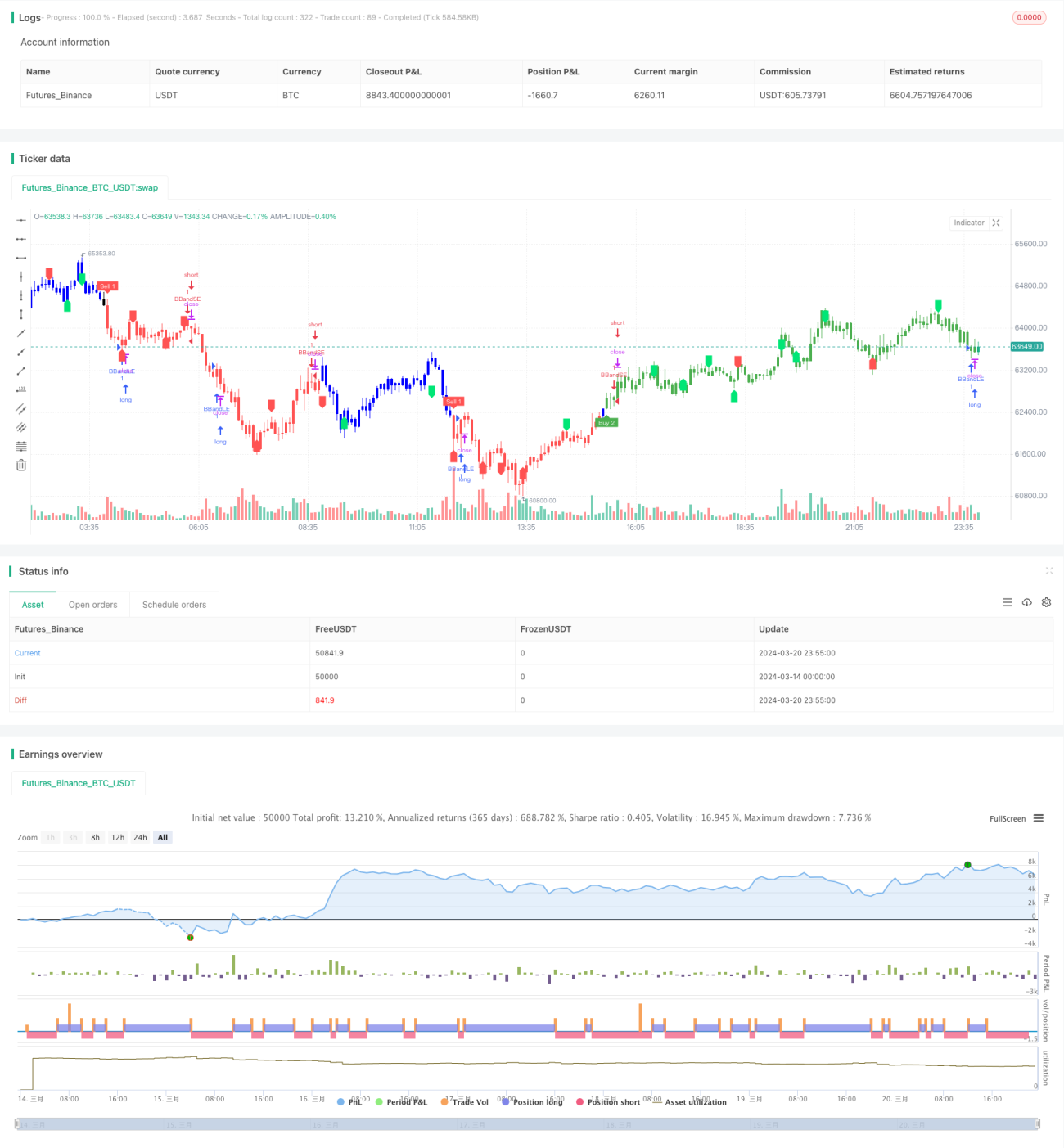

/*backtest

start: 2024-03-14 00:00:00

end: 2024-03-21 00:00:00

period: 5m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © LonesomeThecolor.blue- 1