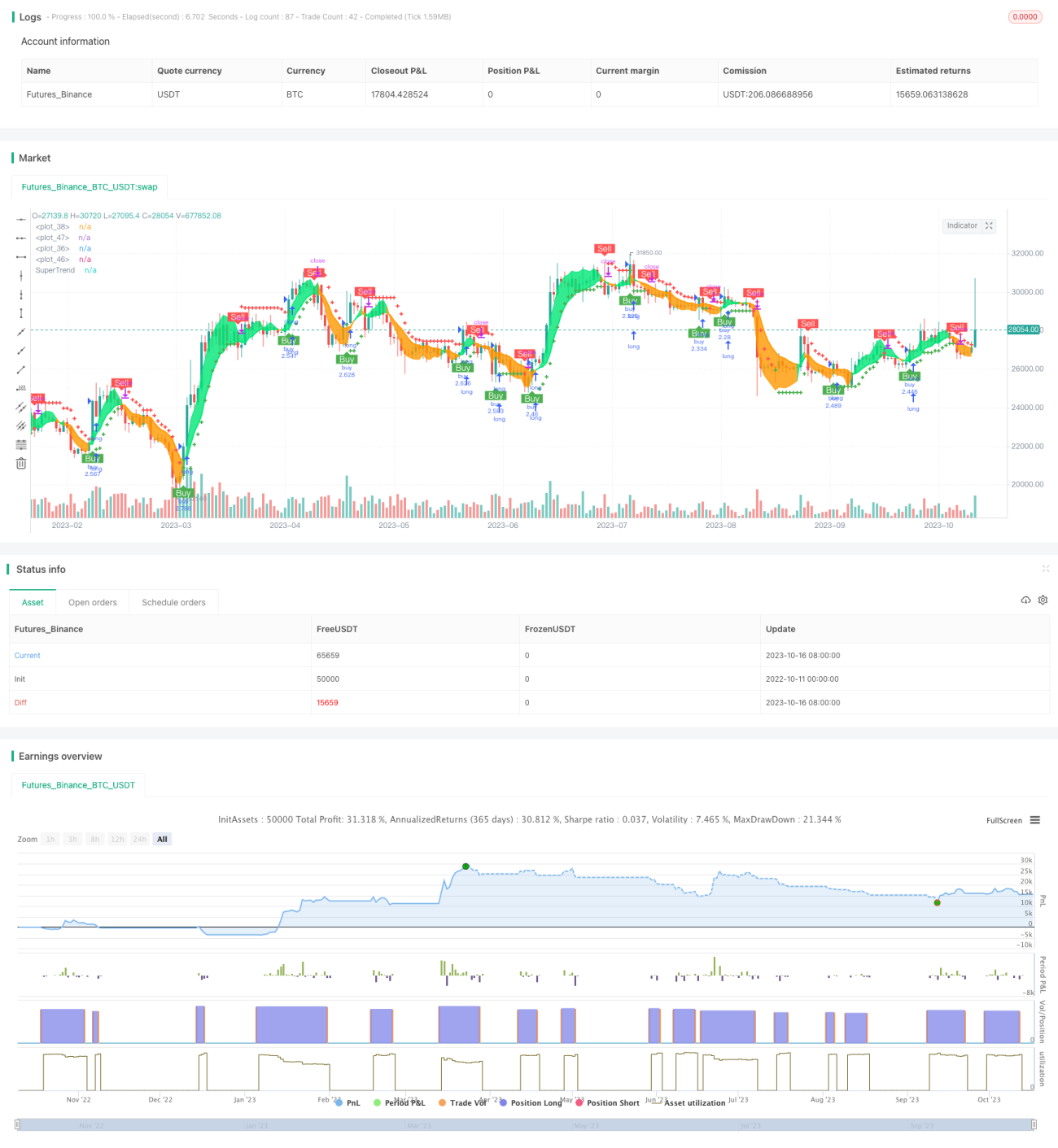

概要

超トレンドV戦略は、移動平均線と標準偏差を活用した短期取引戦略です。Super Trendインジケーターで価格のトレンド方向を判断し、移動平均線によるサポートとレジスタンスを組み合わせてエントリーを行います。同時に標準偏差チャネルを用いて価格の潜在的サポート・レジスタンス領域を予測し、ストップロスとテイクプロフィットの価格帯を設定することで、トレンドフォローと高効率なエグジットを実現する短期取引戦略です。

戦略の原理

まず、Super Trendインジケーターを計算します。Super TrendはATRと価格の関係からトレンドの方向を判断します。価格が上昇トレンドを上回れば強気、下降トレンドを下回れば弱気と見なします。

次に、価格の移動平均線EMAと始値の移動平均線EMAを計算します。価格が移動平均線を上抜け、かつ始値の移動平均線を上回った場合に買いシグナル、価格が移動平均線を下抜け、かつ始値の移動平均線を下回った場合に売りシグナルとします。

続いて、標準偏差を用いて価格チャネルの上限と下限を計算し、平滑化処理を行います。価格が標準偏差の上限を突破した場合にストップロス、標準偏差の下限を突破した場合にテイクプロフィットのシグナルとします。

最後に、異なる時間軸の移動平均線を組み合わせてトレンド方向を判断し、Super Trendインジケーターと連携することで安定したトレンド判断を実現します。

戦略の利点

- Super Trendインジケーターで価格トレンド方向を判断し、トレンド反転による損失を回避

- 移動平均線と始値を組み合わせてエントリータイミングを補助判断し、ダマシのブレイクアウトを防止

- 標準偏差チャネルで価格の潜在的サポート・レジスタンス領域を予測し、ストップロス・テイクプロフィットを設定

- 複数時間軸を組み合わせてトレンド方向を判断し、安定性を向上

戦略のリスク

- Super Trendにラグが生じ、トレンド転換点を見逃す可能性がある

- 移動平均線のクロスシグナルにもラグが生じ、エントリータイミングが不正確になる可能性がある

- 標準偏差チャネルの範囲が固定されすぎて、市場変動をリアルタイムに反映できない

- 複数の時間軸判断が互いに矛盾を生じる可能性がある

リスク解決方法:

- Super Trendのパラメータを適度に短縮し、感度を高める

- 移動平均線の期間を最適化する、または他のインジケーターを追加してエントリーを判断する

- 標準偏差チャネルのパラメータを動的に調整し、市場に合わせた範囲に変更する

- 複数時間軸の判断ロジックを明確にし、矛盾に対処する方法を定める

戦略の最適化方向

- Super Trendのパラメータを最適化し、最適なパラメータ組み合わせを探す

- 他のインジケーターと移動平均線を組み合わせてエントリータイミングを判断する試み

- 標準偏差チャネルのパラメータを動的に調整する試み

- 異なる複数時間軸の組み合わせをテストし、最も適合する時間軸を見つける

- ストップロス・テイクプロフィット戦略を最適化し、戦略の利益空間を拡大

まとめ

超トレンドV戦略は、トレンド、移動平均線、標準偏差チャネルなどのインジケーターの利点を統合し、トレンド方向を安定して判断し、適切なエントリータイミングを選択し、価格帯でストップロス・テイクプロフィットを設定する短期取引戦略を実現しました。パラメータ最適化、インジケーター最適化、ストップロス・テイクプロフィットの最適化などを通じて、戦略の安定性と収益性を高めることができます。その堅固なロジックと厳密な考え方は、学習と研究に値します。

/*backtest

start: 2022-10-11 00:00:00

end: 2023-10-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © theCrypster 2020

//@version=4

strategy(title = "Super trend V Strategy version", overlay = true, pyramiding=1,initial_capital = 1000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0.075)- 1