RSI MACDクロス二重移動平均線追跡戦略

1

Follow

1802

Followers

概要

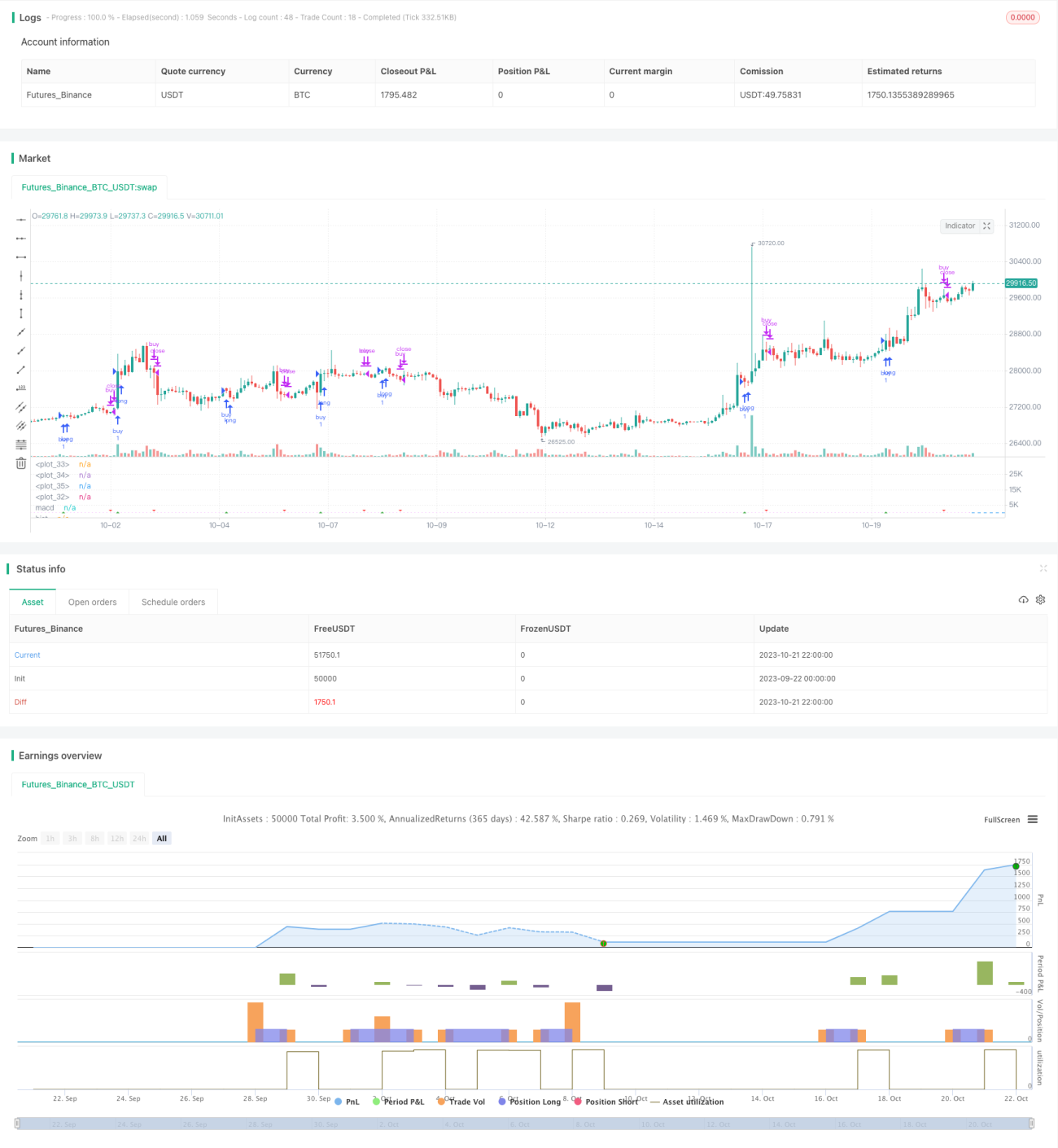

本戦略はRSI指標、MACD指標およびダブル移動平均線を総合的に活用し、トレンドフォローと標準偏差相場のポジショニングを実現します。戦略はRSI指標で買われ過ぎ・売られ過ぎを判断し、MACDで短期・長期移動平均線のクロスによる売買タイミングを特定し、ダブル移動平均線でノイズ取引を一部除去することで、トレンドの中で利益を得ます。

戦略原理

-

RSI指標の計算による買われ過ぎ・売られ過ぎの判断

- 一定期間の上昇・下落変化を計算

- その変化に基づいてRSIを算出

- 買われ過ぎ・売られ過ぎのシグナルを提示

-

MACD指標の計算によるクロス判断

- 短期線、長期線、シグナル線を計算

- 短期線と長期線のクロスで買い・売りを実行

- クロス状況を表示

-

ダブル移動平均線によるフィルター

- 短期線、長期線を算出

- 短期線が長期線を上抜けた場合のみ取引を検討

- トレンドフォローでノイズを除去

-

複数指標を組み合わせたエントリー判断

- RSI、MACD、ダブル移動平均線の複数条件でフィルタリング

- 戦略の安定性を向上

優位性分析

- 複数の指標を組み合わせることで戦略の精度を向上

- トレンドフォローによるノイズ除去で安定性を向上

- RSI指標による買われ過ぎ・売られ過ぎ判断で転換点を捉えやすい

- MACDクロス判断で売買タイミングをシンプルかつ効果的に判断

- ダブル移動平均線フィルターで大部分の非主流方向の取引機会を除去

- パラメータが少なく理解しやすく、初心者が学習・改良しやすい

リスク分析

- 複数指標の組み合わせにより戦略の過剰最適化が生じやすい

- ダブル移動平均線が柔軟性を犠牲にし、一部の機会を逃す可能性

- RSIとMACDのパラメータ選定には注意が必要

- 取引対象のストップロスポイントを考慮し、リスクを管理する必要がある

- 長期的に使用するには市場に合わせたパラメータ調整が繰り返し必要

最適化の方向性

- RSIパラメータを調整し、異なる商品特性に適応させる

- ダブル移動平均線の期間を調整し、トレンドフォロー効果を最適化

- ストップロス戦略を導入し、1回の損失をコントロール

- より多くの指標を組み合わせ、条件のバリエーションを豊富にする

- パラメータ適応モードを開発し、自動的にパラメータを調整する

まとめ

本戦略はRSI、MACD、ダブル移動平均線などの複数の指標を総合的に活用し、トレンドの判断と追跡、機会の多層フィルタリングを実現します。初心者が学習・改良しやすいマルチ指標戦略です。この戦略の優位性はシンプルかつ効率的で、理解しやすく適応しやすい点にあり、パラメータ調整により安定したリターンを得られます。次のステップとして、さらに多くの指標を追加したり、適応型パラメータモードを開発することで、戦略をさらに最適化し、さまざまな市場環境に自動適応できるようにすることが可能です。

Source

Pine

/*backtest

start: 2023-09-22 00:00:00

end: 2023-10-22 00:00:00

period: 2h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// strategy(title="RSI MACD", precision = 6, pyramiding = 1, default_qty_type = strategy.percent_of_equity, default_qty_value = 99, commission_type = strategy.commission.percent, commission_value = 0.25, initial_capital = 1000)

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1