パウエル指数クイックブレイクアウト戦略

概要

本戦略は、RSI指標とローソク実体のEMAを用いた高速ブレイクアウト取引を実現します。RSIの高速形態と大きなローソク実体を利用して反転シグナルを特定します。

戦略の原理

-

RSI指標を計算します。期間は7で、RMAを用いて加速形態を実現します。

-

ローソク実体の大きさのEMAを計算します。期間は30で、実体サイズの基準とします。

-

RSIが下限ライン(デフォルト30)を上抜け、かつ現在のローソク実体が平均実体サイズの1/4より大きい場合、買いポジションを取ります。

-

RSIが上限ライン(デフォルト70)を下抜け、かつ現在のローソク実体が平均実体サイズの1/4より大きい場合、売りポジションを取ります。

-

既にポジションを保有している場合、RSIが再びラインをクロスバックしたときに決済します。

-

RSIの長さ、閾値、参照価格などのパラメータを設定できます。

-

実体サイズEMAの期間、エントリー実体倍率などのパラメータを設定できます。

-

RSIのゴールデンクロス/デッドクロスの本数を設定できます。

優位性分析

-

RSI指標の反転特性を活用し、反転シグナルをタイムリーに捉えることができます。

-

RMAによるRSIの加速形態により、反転に対する感度が向上します。

-

大きなローソク実体によるフィルターを組み合わせることで、小幅なレンジ相場での損切りを回避できます。

-

バックテストデータが十分にあり、信頼性が比較的高いです。

-

パラメータをカスタマイズ可能で、様々な市場環境に適応できます。

-

取引ロジックが明確でシンプルです。

リスク分析

-

RSI指標にはバックテストのバイアスが存在し、実運用での効果は検証が必要です。

-

大きなローソク実体だけでは、十分にレンジ相場をフィルタリングできない可能性があります。

-

デフォルトパラメータが全ての銘柄に適しているわけではなく、最適化が必要です。

-

勝率が高くない可能性があり、連続した損切りの心理的プレッシャーに耐える必要があります。

-

ブレイクアウト失敗のリスクがあり、適切な損切りが求められます。

最適化の方向性

-

RSIパラメータを最適化し、異なる時間足や銘柄に適応できるようにします。

-

ローソク実体EMAの期間を最適化し、実体サイズを平滑化します。

-

エントリー時の実体倍率を最適化し、エントリー頻度を調整します。

-

移動損切りを追加し、勝率を確保します。

-

トレンドフィルターを追加し、逆張り取引を避けます。

-

資金管理戦略を最適化し、1回あたりのリスクをコントロールします。

まとめ

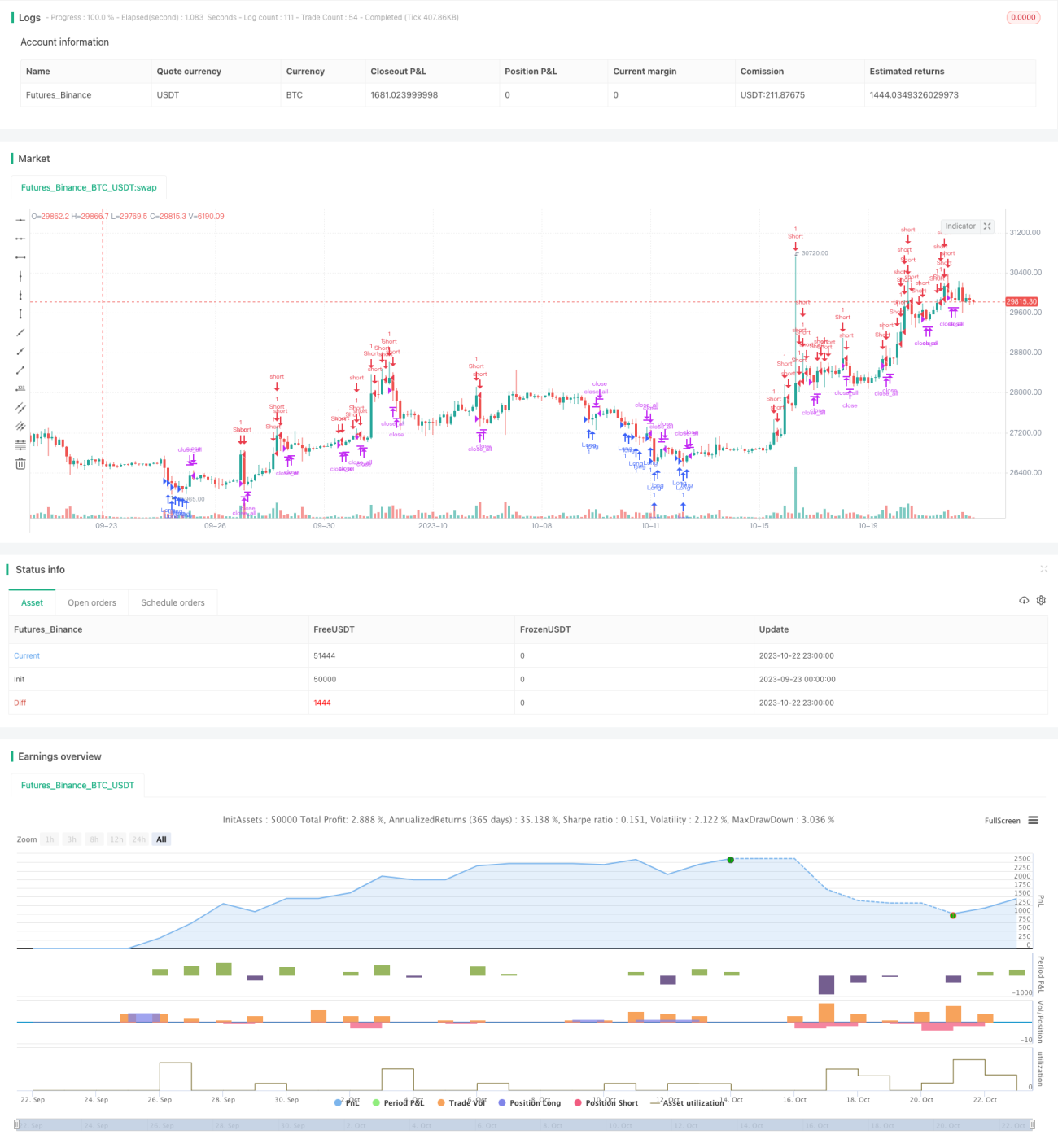

本戦略は全体的に非常にシンプルで直接的な反転戦略です。RSI指標の反転特性と大きなローソク実体の破壊力を同時に活用し、市場のブレイクアウト時に素早くエントリーします。バックテストの結果は良好ですが、実運用での効果はまだ検証が必要であり、使用時にはパラメータの最適化とリスク管理に注意する必要があります。全体的に、本戦略は非常に高い価値を持ち、実運用に適用でき、継続的に最適化できる優れた戦略の一つです。

/*backtest

start: 2023-09-23 00:00:00

end: 2023-10-23 00:00:00

period: 3h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy(title = "Noro's Fast RSI Strategy v1.2", shorttitle = "Fast RSI str 1.2", overlay = true, default_qty_type = strategy.percent_of_equity, default_qty_value = 100, pyramiding = 5)

//Settings- 1