モメンタムアービトラージ戦略のバックテスト分析

一、戦略名

本戦略の主な特徴から、「モメンタムアービトラージ戦略」と命名する。

二、戦略概要

本戦略は、Chandeモメンタムオシレーターを計算し、上下の閾値を設定してロング・ショートシグナルを生成することで、アービトラージの機会を作り出し、利益を獲得する。

三、戦略の原理

コードではまず、パラメータLength、TopBand、LowBandを設定する。Lengthはモメンタムを計算する日数周期、TopBandとLowBandは設定された上下の閾値を表す。

次に、直近Length日の絶対モメンタムxMomを計算し、そのxMomのLength日単純移動平均xSMA_momを計算する。

続いて、Length日間の累積モメンタムxMomLengthを計算する。

次に、モメンタムオシレーターnResを計算する。これはxMomLengthをxSMA_momで割り、Lengthを掛け、さらに100倍した値である。

nResと上下の閾値の大小関係に基づいてロング・ショートの方向を判定し、posに格納する。

最後に、逆取引を有効にするかどうかに応じてposを修正し、取引シグナルpossigを生成し、ロング・ショートのエントリーを発生させる。

四、戦略の優位性

- モメンタム指標を用いてトレンドの潜在的な転換点を識別し、トレンドを捉えやすくする

- 閾値によるフィルタリングを組み合わせ、明確なロング・ショートシグナルを形成し、誤った取引を回避する

- 逆取引の考え方を適用し、反転の機会を得ることができる

- パラメータの調整範囲が広く、異なる銘柄や期間に合わせて最適化できる

- パラメータを視覚的に表示できるため、取引ロジックを把握しやすい

五、戦略のリスク

- モメンタム要因のみを考慮するため、他のテクニカル指標が形成する取引機会を見逃す可能性がある

- モメンタムのブレイクが必ずしもトレンド転換を意味するとは限らず、誤判定のリスクがある

- 逆取引には利益の余地があるが、損失を拡大させる可能性もある

- パラメータの最適化が不適切だと、取引が過剰になったり、最適なエントリーポイントを逃したりする恐れがある

- 突発的な事象による短期的なモメンタムの歪みを適切にフィルタリングする必要がある

トレンドやボラティリティなどの他のテクニカル指標を組み合わせてモメンタムシグナルの信頼性を確認したり、パラメータを調整して取引頻度を下げたり、ストップロスを適度に緩めたりすることでリスクをコントロールできる。

六、戦略の最適化方向

- 他のテクニカル指標によるフィルタリングを追加し、取引シグナルの精度を向上させる

モメンタムシグナルが発生する前に、終値が移動平均線システムの上にあるか、ボラティリティが正常範囲内にあるかを判断し、誤ったシグナルを回避する。

- 銘柄特性に応じてパラメータを最適化する

ボラティリティの高い銘柄では、モメンタム変動の正常閾値範囲を広めに設定し、取引頻度を下げる。

- 異なる時間足でマルチタイムフレーム最適化を行う

日内取引では短い周期のLengthを用いて超短期トレードを行い、週足や月足に基づいてパラメータを調整し、中長期トレンドに重点を置く。

- ダイバージェンス条件を設定する

買いシグナルが発生した場合、価格が以前のボトムより高いという条件を追加し、トレンド反転の偽シグナルを回避する。

七、まとめ

本戦略は主にモメンタム指標を用いて短期トレンドの反転機会を識別し、パラメータフィルタリングを組み合わせて取引シグナルを生成し、トレンド追跡と反転の捕捉を両立し、リスクをコントロール可能としている。マルチタイムフレーム最適化や他のテクニカル指標との組み合わせにより、戦略の取引効果を向上させることができ、さらなる研究と応用に値する。

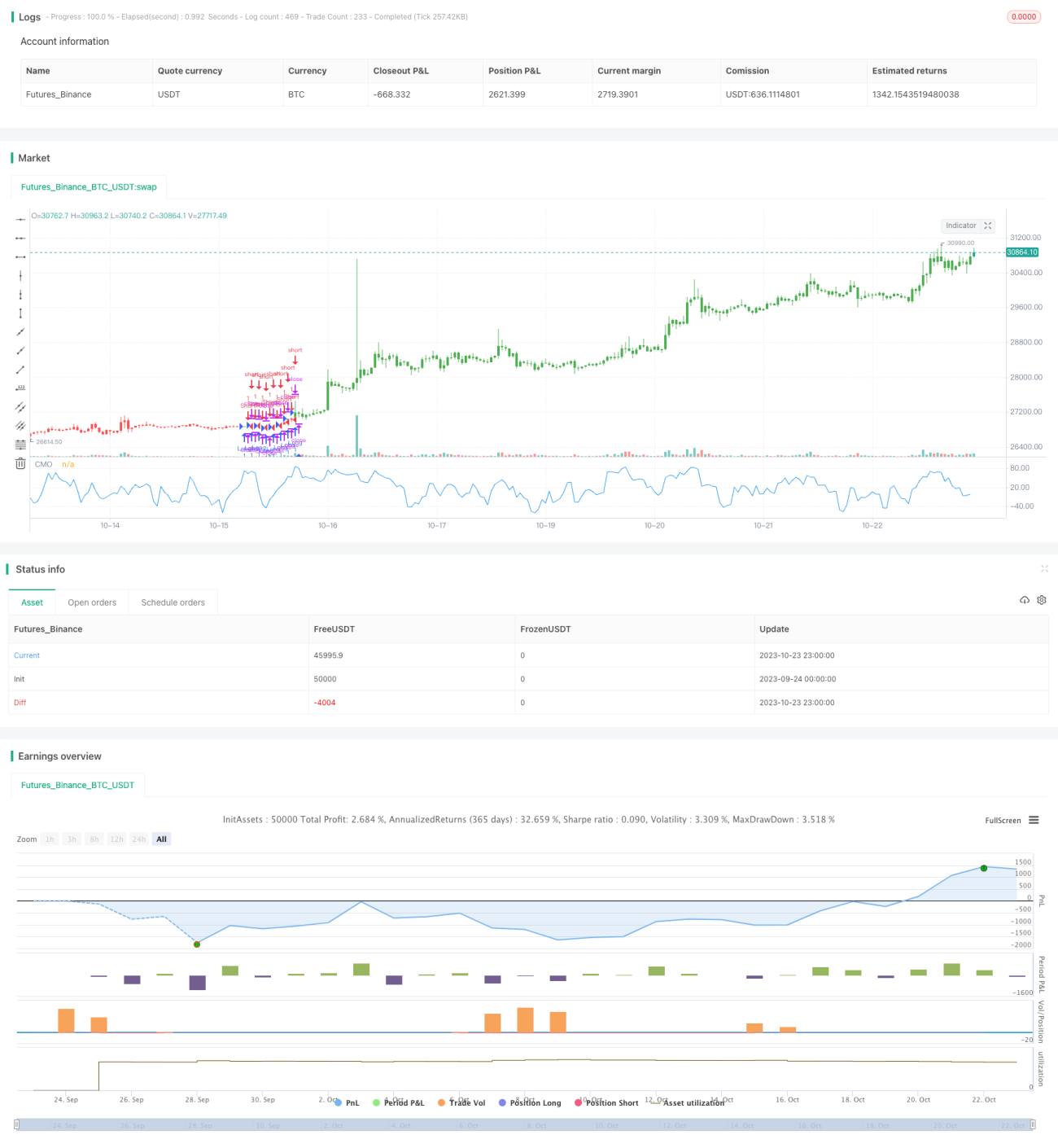

/*backtest

start: 2023-09-24 00:00:00

end: 2023-10-24 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 07/02/2017

// This indicator plots Chande Momentum Oscillator. This indicator was - 1