素数オシレーターに基づく取引戦略

概要

この戦略は、素数オシレーター指標に基づいて市場のトレンドを判断し、それに応じてロング・ショートポジションを構築します。素数オシレーターは、価格付近の最も近い素数と価格の差を計算し、正の値は強気トレンド、負の値は弱気トレンドを示します。この戦略は、価格が乱高下する際に隠れたトレンド情報を捉えることができ、ブレイクアウト取引に有用な指針を提供します。

戦略の原理

この戦略は、まずPrimeNumberOscillator関数を定義し、引数として価格とallowedPercentを取ります。この関数は、価格から正負allowedPercentの範囲内で最も近い素数を探し、両者の差を返します。差が0より大きい場合は強気トレンド、0より小さい場合は弱気トレンドを示します。

次に、戦略内でPrimeNumberOscillator関数を呼び出してxPNO値を計算します。xPNOの正負に基づいてポジションの方向を判断し、reverseFactorを乗算して最終的な取引方向を決定します。取引方向に応じて買い建てまたは売り建てを行います。

この戦略は主に素数オシレーター指標に依存してトレンド方向を判断します。指標自体は比較的粗く、取引シグナルを検証するには他の要素と組み合わせる必要があります。しかし、数学的原理に基づいているため、一定の客観的な指針を提供できます。

優位性の分析

- 数学的原理に基づいており、比較的客観的

- 乱高下の中に隠れたトレンドを識別できる

- パラメータ調整が柔軟で、感度を自由に設定可能

- 実装が簡単で、理解や最適化が容易

リスク分析

- 素数オシレーター指標自体は比較的粗く、誤判定が繰り返し発生する可能性がある

- 他のテクニカル指標と組み合わせて検証する必要があり、単独で使用できない

- パラメータの選択には注意が必要で、大きすぎたり小さすぎたりすると機能しなくなる

- 取引頻度が高くなりすぎる可能性があるため、ポジションサイズの管理が必要

最適化の方向性

- 移動平均線や買われ過ぎ・売られ過ぎなどの指標を組み合わせてシグナルをフィルタリングできる

- ストップロス戦略を追加して、1回あたりの損失を抑える

- 市場状況に応じてallowedPercentパラメータを動的に調整できる

- ボラティリティなどの指標を用いてポジションサイズを制御するなど、ポジション管理を最適化できる

まとめ

この戦略は素数オシレーターの原理に基づいてトレンド方向を判断し、実装が簡単でロジックも明確です。ただし、素数オシレーター自体には一定の限界があるため、慎重に使用する必要があります。他のテクニカル指標を組み合わせてシグナルを検証し、取引リスクを管理することができます。この戦略は数学的取引戦略の代表的な例であり、学習や研究において一定の参考価値があります。

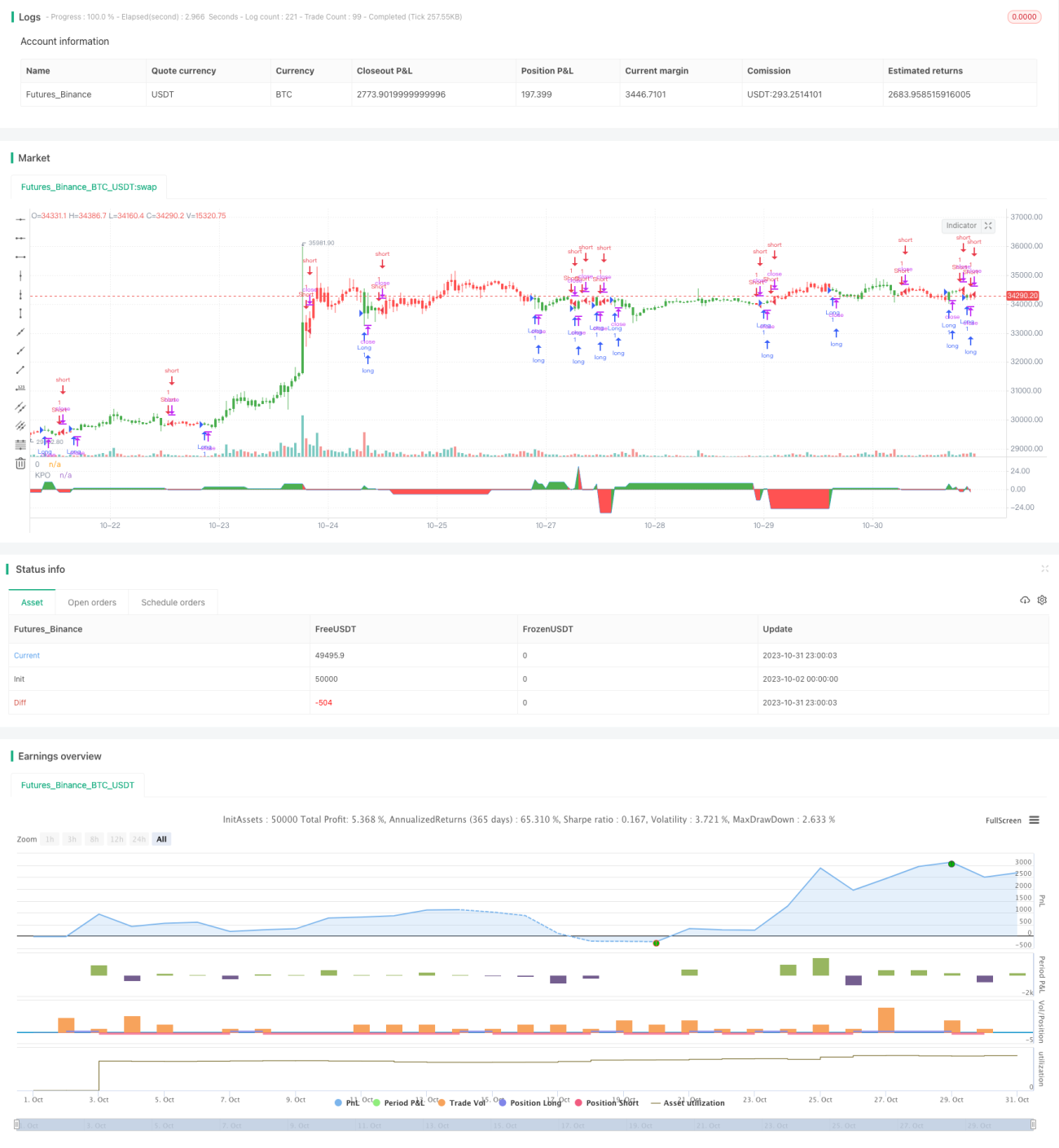

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 29/03/2018

// Determining market trends has become a science even though a high number or people - 1