概要

大幅上昇・大幅下落戦略は、巨大な陽線・陰線を検出してエントリーする戦略です。巨大な陽線を検出した場合は売り、巨大な陰線を検出した場合は買いを行います。ストップロスはシグナルが出たバーの安値(買いの場合は逆)に設定し、利確はストップロスの1倍とします。ユーザーは陽線・陰線の最小サイズ、および過去一定期間の平均バーサイズに対する倍率を定義できます。

戦略の原理

この戦略の核心的なロジックは以下の通りです。

-

現在のローソク足の全変動幅(高値-安値)と実体の大きさ(終値が始値より大きければプラス、小さければマイナス)を計算します。

-

過去N本のローソク足における変動幅の平均値を計算します。

-

現在のローソク足が以下の条件を満たすか判断します:変動幅 >= 平均変動幅 × 倍数 かつ 実体の大きさ >= 変動幅 × 最小実体係数

-

上記条件を満たすとシグナルが発生:陽線なら売り、陰線なら買い。

-

ストップロス・利確の有無を選択可能:ストップロスはシグナルバーの安値+ストップロス係数倍の変動幅、利確はストップロスの1倍。

実体の判断では、線分(ヒゲ)を除外し、十分な力があることを確保します。変動幅の平均を動的に計算することで、固定しきい値では市場変化に適応できない問題を回避します。ストップロス・利確は適切な最大損失率を設定し、係数で調整可能です。

戦略の優位性

この戦略の最大の利点は、質の高いトレンド反転シグナルを捉えられる点です。これは主に2つの判断に基づいています。

-

巨大な陽線・陰線は、それまでのトレンドがすでに強く動いていることを示すため、トレンド全体の構造的な転換点である可能性が高い。

-

変動幅の平均を動的に計算することで、通常を超える異常な変動を確実に捉え、通常の押し目・戻りをフィルタリングできる。

さらに、ストップロス・利確の設定も非常に合理的で、1回の損失を効果的にコントロールできると同時に、利確のリターン率が1であるため、過度な追撃を避けられます。

総じて、この戦略は質の高い構造的転換点を特定し、効率的な取引を実現します。トレンドフォロー型トレーダーに非常に適しており、途中で相場に巻き込まれるリスクを回避できます。

戦略のリスク

この戦略の主なリスクは以下の2点です。

-

大幅上昇・下落がストップロスの連鎖を引き起こし、無効なシグナルとなる可能性がある。

-

ストップロスの設定が甘すぎて、損失を効果的に抑えられない可能性がある。

最初のリスクに対しては、最小変動幅や実体の大きさを増やすことで誤判定率を下げられますが、その分チャンスを逃す可能性もあります。バックテスト結果からバランスの取れたポイントを見つける必要があります。

2つ目のリスクは、ストップロス係数を調整することで最適化できます。ストップロスをサポートラインに近づけられれば、ただしあまりにタイトにしすぎないように注意します。同時に、利確のリターン率を上げて、ストップロスによる損失を補うことも検討します。

戦略の最適化方向

この戦略は以下の点でさらに最適化できます。

-

トレンド方向の判断を追加し、逆張りを避ける。

-

パラメータ設定を最適化し、最適なパラメータの組み合わせを見つける。

-

出来高によるフィルタリングを追加し、大陽線・大陰線の出来高が十分高いことを確認する。

-

さらにフィルタリング条件(例:プラットフォーム、ボリンジャーバンドなど)を追加し、誤判定の確率を減らす。

-

異なる銘柄でのパラメータ効果をテストし、パラメータ最適化を行う。

-

ストップロスのトレーリングを追加し、価格の動きに応じてストップロスを動的に調整する。

-

再エントリーの機会を追加する。つまり、最初のストップロス後に再度エントリーする。

以上の最適化により、この戦略の有効性を高め、実際の利益確率を向上させることができます。十分なバックテストと最適化を行い、最適なパラメータを見つける必要があります。

まとめ

大幅上昇・大幅下落戦略は、巨大な陽線・陰線を捉えることで効率的に利益を上げ、ストップロス・利確も設定されています。質の高い構造的反転の機会を特定し、トレンドトレーダーにとって非常に価値のある情報を提供します。パラメータ最適化やルールの改良により、この戦略は非常に実用的な意思決定補助ツールになり得ます。シンプルな取引ロジックと直接的な経済的意味により、理解しやすく使いやすいのも特徴です。総じて、この戦略は優れたフレームワークを提供しており、さらなる研究と応用に値します。

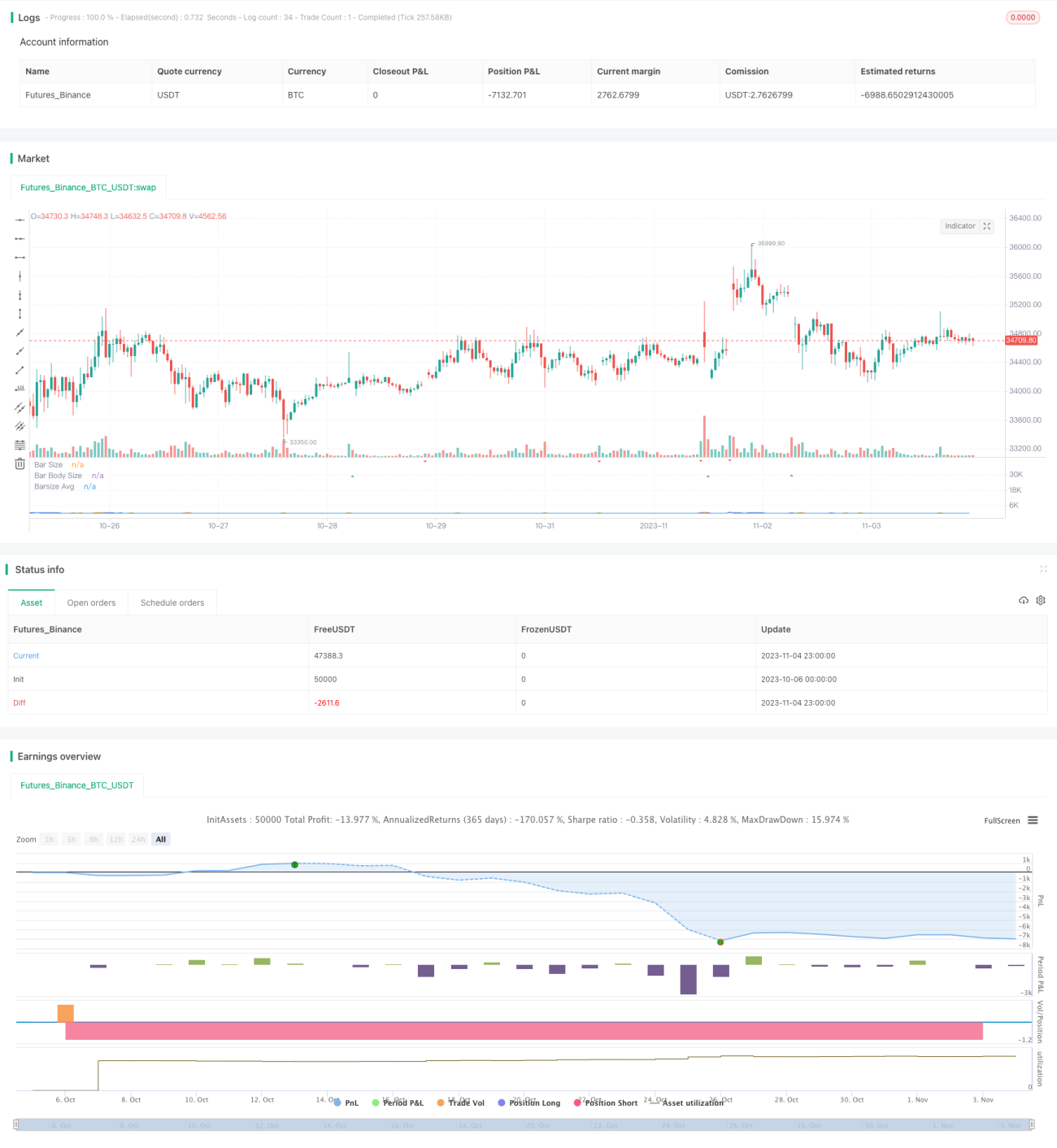

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tweakerID

// This strategy detects and uses big bars to enter a position. When the Big Bar - 1