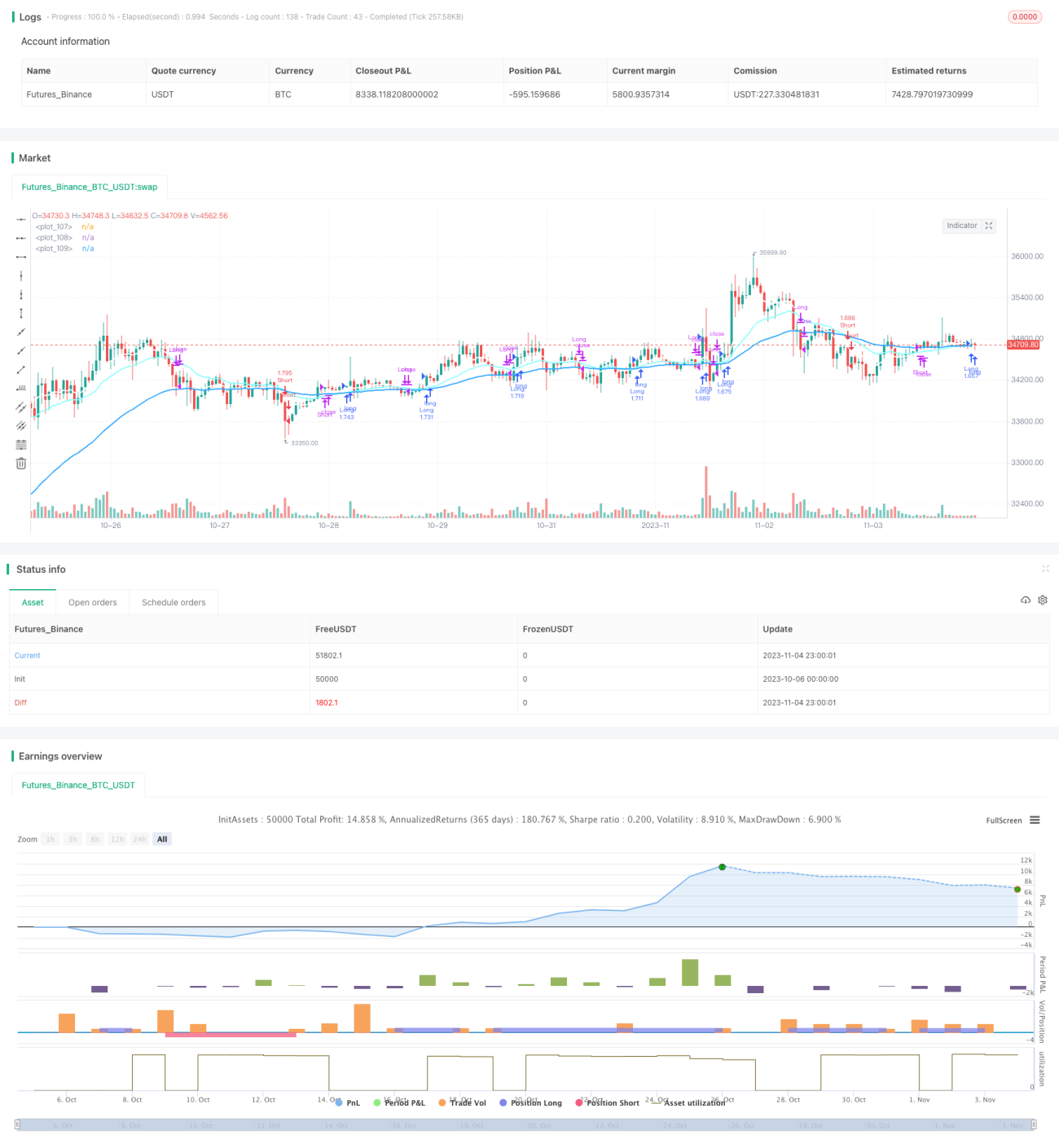

トリプル移動平均チャネル・トレンドフォロー戦略

1

Follow

1802

Followers

概要

本戦略はトリプル移動平均線の組み合わせを採用し、移動平均線の順序関係に基づいてトレンド方向を判断し、トレンド追跡を行います。短期移動平均線、中期移動平均線、長期移動平均線が順に並ぶときにロング、長期移動平均線、中期移動平均線、短期移動平均線が順に並ぶときにショートします。

戦略原理

本戦略では、異なる期間の3本の移動平均線(短期移動平均線、中期移動平均線、長期移動平均線)を使用します。

エントリー条件:

- ロング:短期移動平均線 > 中期移動平均線 > 長期移動平均線の場合、相場は上昇トレンドと判断しロングします。

- ショート:長期移動平均線 < 中期移動平均線 < 短期移動平均線の場合、相場は下降トレンドと判断しショートします。

エグジット条件:

- 移動平均線によるエグジット:3本の移動平均線の順序が逆転した場合にポジションをクローズします。

- 利確・損切りによるエグジット:固定の利確・損切ポイントを設定します。例えば、利確幅を12%、損切幅を1%とし、これらの価格に達したらポジションをクローズします。

本戦略はシンプルかつ直接的で、3本の移動平均線を用いて市場のトレンド方向を判断し、トレンド追跡取引を実現します。トレンドが強い市場に適しています。

優位性分析

- 3本の移動平均線でトレンドを判断し、市場ノイズをフィルタリングし、トレンド方向を識別します。

- 異なる期間の移動平均線を使用することで、トレンド転換点をより正確に判断できます。

- 移動平均線指標と固定の利確・損切りを組み合わせて資金リスクを管理します。

- 戦略の考え方はシンプルかつ直感的で、理解・実装が容易です。

- 移動平均線の期間パラメータを容易に最適化でき、異なる期間の相場に適応できます。

リスクと改善点

- 大きな時間枠では、移動平均線が誤判定を多く発生させ、不要な損失につながる可能性があります。

- 他の指標やフィルター条件を追加し、勝率を向上させることを検討できます。

- 移動平均線の期間パラメータの組み合わせを最適化し、より広範な市場相場に適応させることができます。

- トレンドの強弱を示す指標と組み合わせることで、天井買いや底売りを回避できます。

- 自動ストップロスを追加し、損失の拡大を防ぐことができます。

まとめ

本トリプル移動平均線トレンドフォロー戦略は、全体的な考え方が明確で理解しやすく、移動平均線を用いてトレンド方向を判別し、シンプルなトレンドフォロー取引を実現します。戦略の利点は実装が容易で、移動平均線の期間パラメータを調整することで異なる期間の相場に適応できることです。しかし、一定の誤判定リスクも存在するため、他の指標や条件を追加して最適化し、不要な損失を減らし戦略の勝率を高めることが可能です。総じて、本戦略はトレンド取引に興味がある初心者が学習・実践するのに適しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1