ダブルEMAゴールデンクロストレンド追跡戦略

1

Follow

1802

Followers

概要

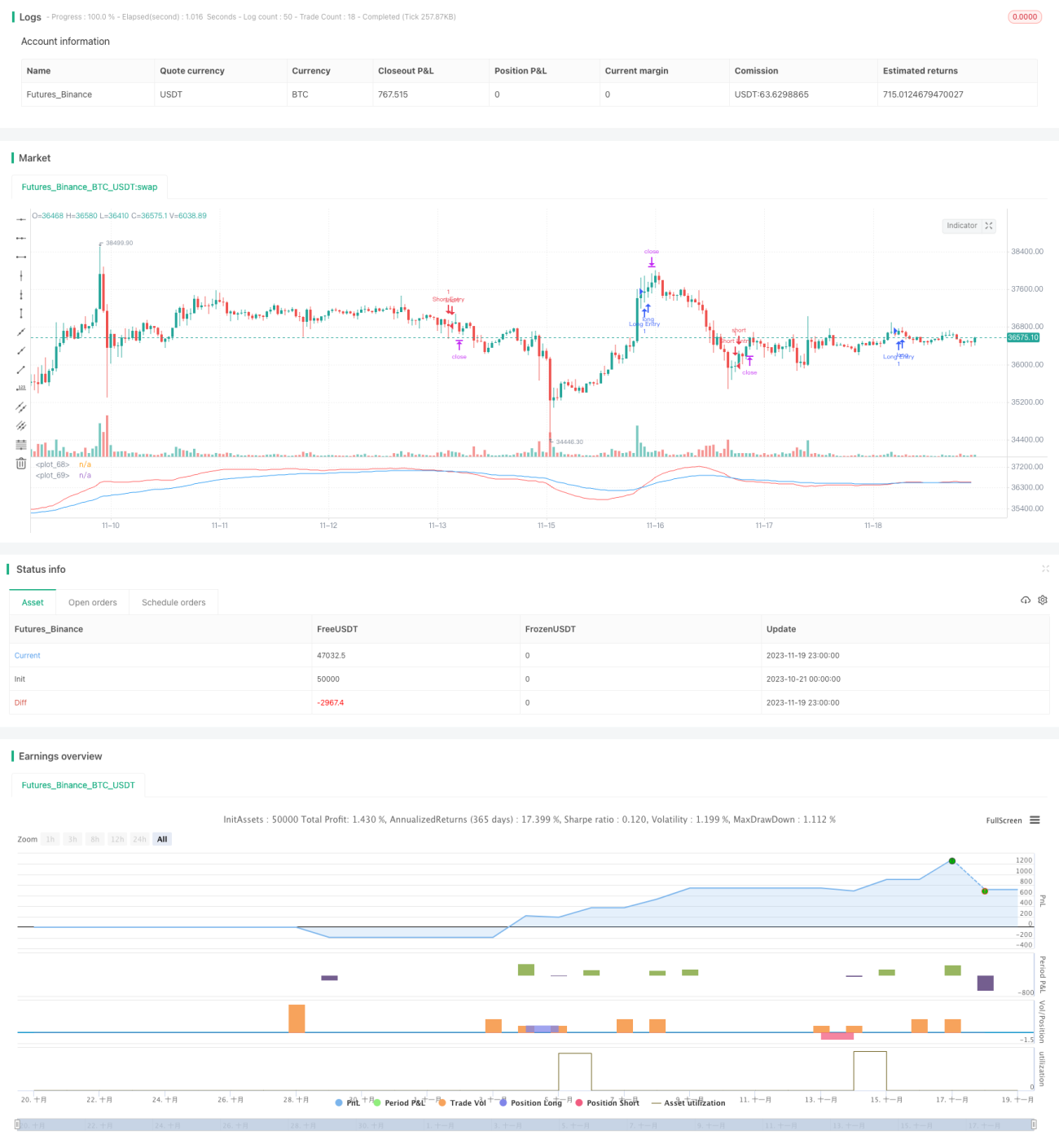

本戦略は、短期EMA(快線EMA)と長期EMA(慢線EMA)を計算し、両者の大小関係を比較することで相場のトレンド方向を判断する、シンプルなトレンド追跡戦略です。短期EMAが長期EMAを上抜けたときに買い、短期EMAが長期EMAを下抜けたときに売る、典型的なデュアルEMAゴールデンクロス戦略です。

戦略の原理

本戦略のコア指標は、短期EMAと長期EMAです。短期EMAの期間は21、長期EMAの期間は55に設定されています。短期EMAは価格変動に素早く反応し、直近の短期的なトレンドを反映します。長期EMAは価格変動への反応が遅く、ノイズをある程度除去し、中長期的なトレンドを反映します。

短期EMAが長期EMAを上抜けた場合、短期トレンドが上昇に転じ、中長期トレンドに転換が生じる可能性があることを示す、買いシグナルです。短期EMAが長期EMAを下抜けた場合、短期トレンドが下落に転じ、中長期トレンドに転換が生じる可能性があることを示す、売りシグナルです。

短期EMAと長期EMAの比較により、短期と中長期の二つの時間軸におけるトレンド転換点を捉えることができ、典型的なトレンド追跡戦略です。

戦略のメリット

- 考え方がシンプルで明確であり、理解と実装が容易

- パラメータ調整が柔軟で、短期EMAと長期EMAの期間をカスタマイズ可能

- ATRによるストップロス・利益確定の設定が可能で、リスクをコントロールできる

戦略のリスク

- デュアルEMAのクロスポイントの選択が適切でない可能性があり、最適なエントリーポイントを逃すリスクがある

- 相場がレンジ相場の場合、無効なシグナルが複数回発生し、損失リスクが生じる可能性がある

- ATRパラメータの設定が適切でない場合、ストップロス・利益確定が甘すぎたり、逆に厳しすぎたりする可能性がある

リスク対策:

- EMA短期・長期のパラメータを最適化し、最適なパラメータ組み合わせを探索する

- フィルター機構を追加し、レンジ相場における無効なシグナルを回避する

- ATRパラメータをテスト・最適化し、ストップロス・利益確定の設定を適切にする

戦略の最適化方向

- 統計的手法に基づき、異なるEMA期間パラメータの安定性をテストする

- フィルター条件を追加し、他の指標と組み合わせて無効なシグナルを回避する

- ATRパラメータを最適化し、最適なストップロス・利益確定比率を得る

まとめ

本戦略は、短期EMAと長期EMAのクロスにより相場のトレンドを判断するもので、シンプルで明確、実装も容易です。同時にATRを組み合わせてストップロス・利益確定を設定し、リスクをコントロールできます。パラメータ最適化やフィルター条件の追加により、戦略の安定性と収益性をさらに高めることができます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1