モメンタムとトレンド判断を組み合わせたマルチファクター・クオンツ取引戦略

1

Follow

1802

Followers

概要

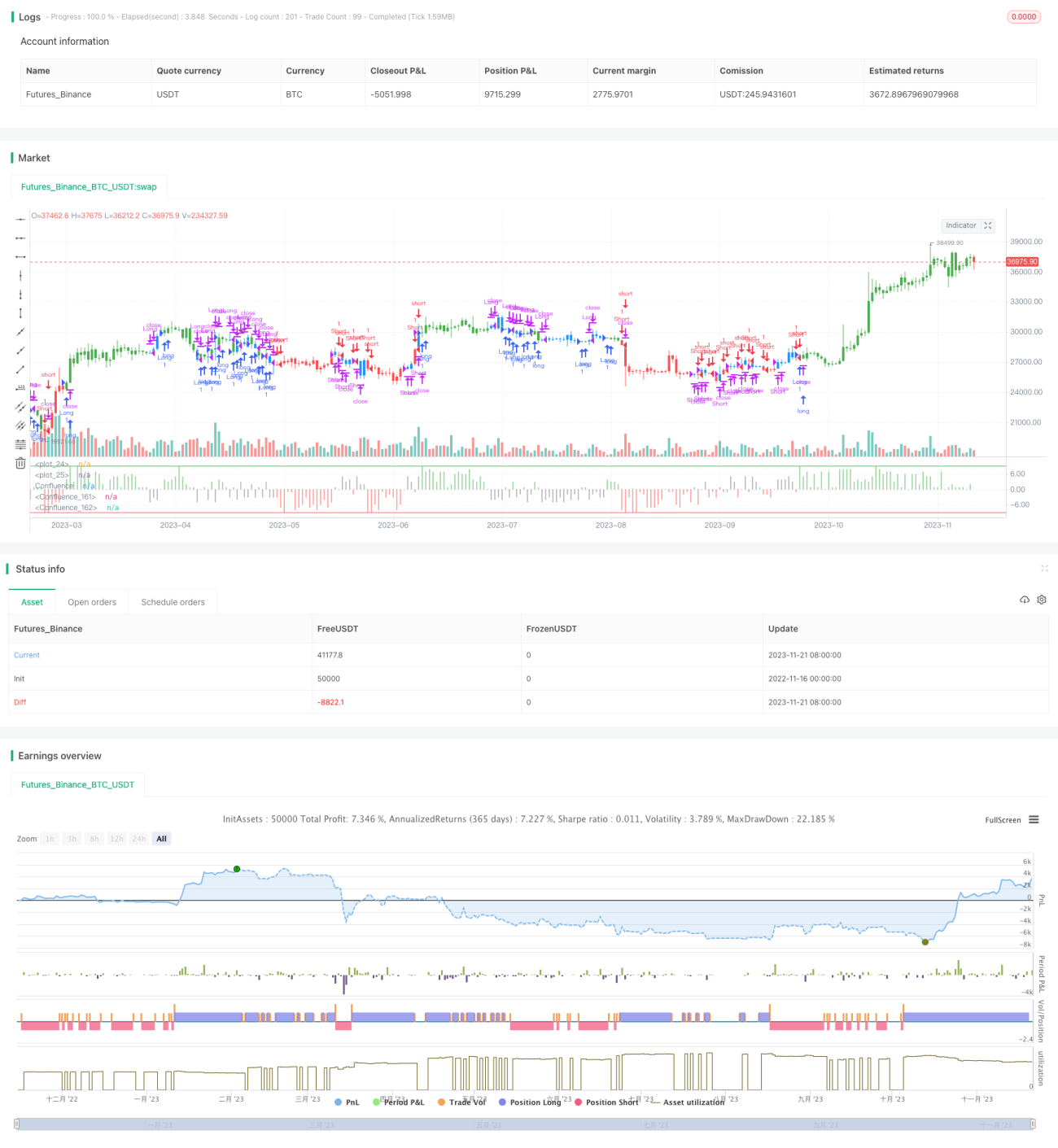

本戦略は、モメンタム指標とトレンド指標を組み合わせた多因子判断型の定量取引戦略です。複数の移動平均線の数学的組み合わせを計算し、市場の全体的なトレンドとモメンタムの方向性を判断し、閾値条件に基づいて取引シグナルを発出します。

戦略の原理

- 複数の移動平均線とモメンタム指標の計算

- ハーモニクス平均線、短期平均線、中期平均線、長期平均線など、複数の移動平均線を計算

- 各平均線間の差を計算し、価格変化のトレンドを反映

- 各平均線の1次導関数を計算し、価格変化のモメンタムを反映

- サイン・コサイン指標を計算し、トレンドの方向性を判断

- 取引シグナルの総合判断

- モメンタム指標、トレンド指標などの多因子を加重計算

- 結果値が閾値からどの程度離れているかに基づき、現在の市場状態を判断

- 買い・売りの取引シグナルを発出

優位性分析

- 多因子判断によるシグナル精度の向上

- 価格、トレンド、モメンタムの複数要素を総合的に考慮

- 各因子に異なる重みを設定可能

- パラメータ調整が可能で、様々な市場に対応

- 平均線パラメータ、取引レンジの境界をカスタマイズ可能

- 異なる時間足や市場環境に適応可能

- コード構造が明確で、理解しやすい

- 命名規則に従い、コメントが充実

- 二次開発や最適化が容易

リスク分析

- パラメータ最適化が困難

- 最適なパラメータを見つけるために大量の過去データによるバックテストが必要

- 取引頻度が高くなりすぎる可能性

- 多因子の組み合わせ判断により、過剰な取引が発生する可能性

- 効果が市場との相関性に大きく依存

- トレンド判断戦略は、非合理的な行動の影響を受けやすい

改善方向

- ストップロスロジックの追加

- 非合理的な行動による大きな損失を回避可能

- パラメータ設定の最適化

- 最適なパラメータ組み合わせを模索し、戦略の安定性を向上

- 機械学習要素の追加

- 深層学習を用いて現在の市場状態を判定し、戦略判断を補助

まとめ

本戦略は、モメンタム指標とトレンド指標を組み合わせた多因子により市場状態を判断し、設定された閾値に基づいて取引シグナルを発出します。戦略の強みは、カスタマイズ性が高く、様々な市場環境に適応できる点、および理解しやすい点です。弱みとしては、パラメータ最適化が困難で、取引頻度が過剰になる可能性があり、効果が市場との相関性に強く依存する点が挙げられます。今後は、ストップロスの追加、パラメータ最適化、機械学習などの手段によるさらなる改善が期待されます。

Source

Pine

/*backtest

start: 2022-11-16 00:00:00

end: 2023-11-22 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 14/03/2017

// This is modified version of Dale Legan's "Confluence" indicator written by Gary Fritz.Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1