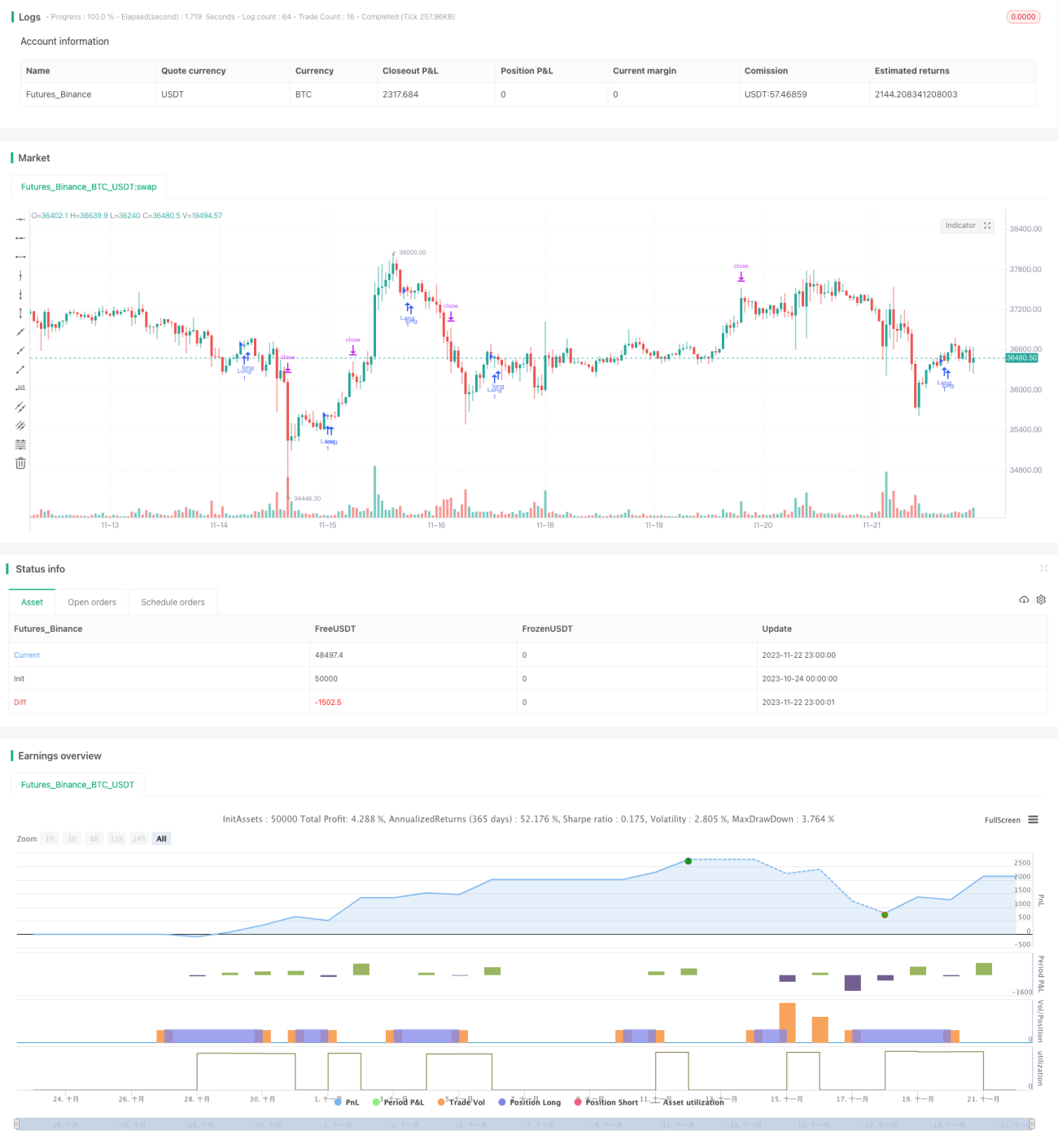

出来高・価格指標に基づく多空均衡取引戦略

概要

本戦略は、マルチタイムフレームの出来高・価格指標を組み合わせた取引戦略です。相対力指数(RSI)、平均真のレンジ(ATR)、単純移動平均線(SMA)、およびカスタムの出来高・価格条件を総合的に用いて、潜在的なロングシグナルを識別します。一定の売られ過ぎ条件、出来高・価格指標のクロス、価格のブレイクアウトなどの条件が満たされた場合、本戦略はロングポジションを建てます。同時に、ストップロスとテイクプロフィットを設定し、各トレードのリスク・リワード比を管理します。

戦略の原理

本戦略は主に以下の重要なポイントに基づいています。

- RSIが売られ過ぎラインを下回り、直近10本のローソク足内で連続して売られ過ぎ状態にある場合、売られ過ぎシグナルと見なします。

- 複数の出来高・価格条件を定義し、これらの条件が同時に満たされた場合にのみ、出来高・価格指標がロングシグナルを発すると判断します。

- 終値が下から上へ13期間のSMAを突破した場合、価格のブレイクアウトシグナルと見なします。

- ATRの短期期間が長期期間を下回ることも、後押しシグナルとなります。

- 上記の複数指標シグナルを総合して、最終的なロング判断を行います。

具体的には、本戦略はRSI指標に期間と売られ過ぎラインのパラメータを設定し、それらに基づいてRSI値を計算します。RSI指標が連続して複数のローソク足で売られ過ぎラインを下回った場合、売られ過ぎシグナルが発生します。

また、本戦略は3つの出来高閾値を定義し、異なる時間周期のデータに基づいて複数の出来高・価格条件を設定します。例えば、90期間の出来高値が49期間の出来高値の1.5倍より大きい場合などです。これらの出来高・価格条件が同時に満たされた場合、出来高・価格指標のロングシグナルが発せられます。

価格に関して、本戦略は13期間のSMAを計算し、価格がSMAを上抜けてからのローソク足本数を集計します。価格が下から上へSMAを突破し、突破後のローソク足本数が5本未満の場合、価格のブレイクアウトシグナルと見なします。

ATR期間パラメータに関して、本戦略は短期期間5と長期期間14のATRを指定します。短期ATRが長期ATRを下回る場合、市場のボラティリティが急速に縮小していることを示し、後押しのロングシグナルとして機能します。

最終的に、本戦略は上記の複数の買い条件(売られ過ぎ、出来高・価格指標、価格ブレイクアウト、ATR指標)を総合的に考慮します。これらの条件が同時に満たされた場合、最終的なロングシグナルが発生し、ロングポジションを建てます。

戦略の優位性

本戦略には以下の優位性があります。

-

マルチタイムフレームの出来高・価格指標判断により精度が向上します。単一周期の出来高・価格データだけでなく、複数の異なる周期の出来高・価格条件のクロスオーバーを評価することで、出来高の集中度をより正確に判断できます。

-

売られ過ぎ+出来高・価格+価格の三重判断メカニズムにより、買いシグナルの信頼性が確保されます。売られ過ぎは最も基本的な買いタイミングの選択を提供し、さらに出来高・価格と価格の指標クロスが買いタイミングに追加の確認を与えるため、信頼性が高まります。

-

ストップロスとテイクプロフィットの設定により、個々のトレードのリスクを厳格に管理します。ストップロスとテイクプロフィットのパラメータは個人のリスク選好に応じて調整可能で、利益の最大化を追求しつつ、各トレードのリスクを合理的にコントロールします。

-

複数指標による統合判断により柔軟性が向上します。一部の指標に障害や誤りが発生した場合でも、他の指標に依存して一定の継続的な運用能力を確保できます。

リスクと対策

本戦略には以下のリスクも存在します。

-

パラメータ設定のリスク。各種指標のパラメータ設定は判断結果に直接影響し、不適切なパラメータは取引シグナルに偏りを生じさせる可能性があります。パラメータの合理的な値は慎重に検証する必要があります。

-

利益幅の限界。複数の指標を統合して判断する戦略として、シグナル発生頻度は比較的保守的であり、単位時間あたりの取引回数が少なくなり、利益幅に一定の制限があります。

-

指標の乖離リスク。一部の指標がロングシグナルを発する一方で、別の指標がショートシグナルを発する場合、戦略は最適な判断を下せません。これは指標間の乖離の可能性を事前に特定し、解決する必要があります。

戦略の最適化方向

本戦略は以下の点からさらに最適化できます。

-

機械学習モデルによる判断補助の追加。出来高・価格およびボラティリティ特徴のモデルを訓練し、人手で設定されたパラメータを補助することで、パラメータの動的最適化を実現できます。

-

テイクプロフィット戦略の高度化。例えば、変動するテイクプロフィット、分割テイクプロフィット、トレーリングテイクプロフィットなどを設定することで、利益確定の柔軟性を高め、各トレードの収益をさらに向上させることができます。

-

板情報データの導入評価。ローソク足の出来高・価格データに加えて、深い買い・売り板データを組み合わせることで、ポジション分布を判断し、追加の参考シグナルを得ることができます。

-

他の指標統合のテスト検証。本戦略は主にRSI、ATR、SMAなどの指標を統合していますが、ボリンジャーバンド、KDJなどの他の指標の組み合わせを試し、取引シグナルのソースを多様化・最適化することも可能です。

まとめ

本戦略は、RSI、ATR、SMA、およびカスタムの出来高・価格条件を総合的に用いて、潜在的なロングタイミングを識別します。マルチタイムフレームの出来高・価格指標判断、三重シグナル確認メカニズム、ストップロス・テイクプロフィットによるリスク管理といった優位性を持ちます。一方で、パラメータ設定のリスクや利益幅の制限などの問題にも注意が必要です。今後、本戦略は機械学習による補助、テイクプロフィット戦略の最適化、板情報データの導入、指標統合の拡張などにより、さらに改善できます。

- 1