1

Follow

1802

Followers

概要

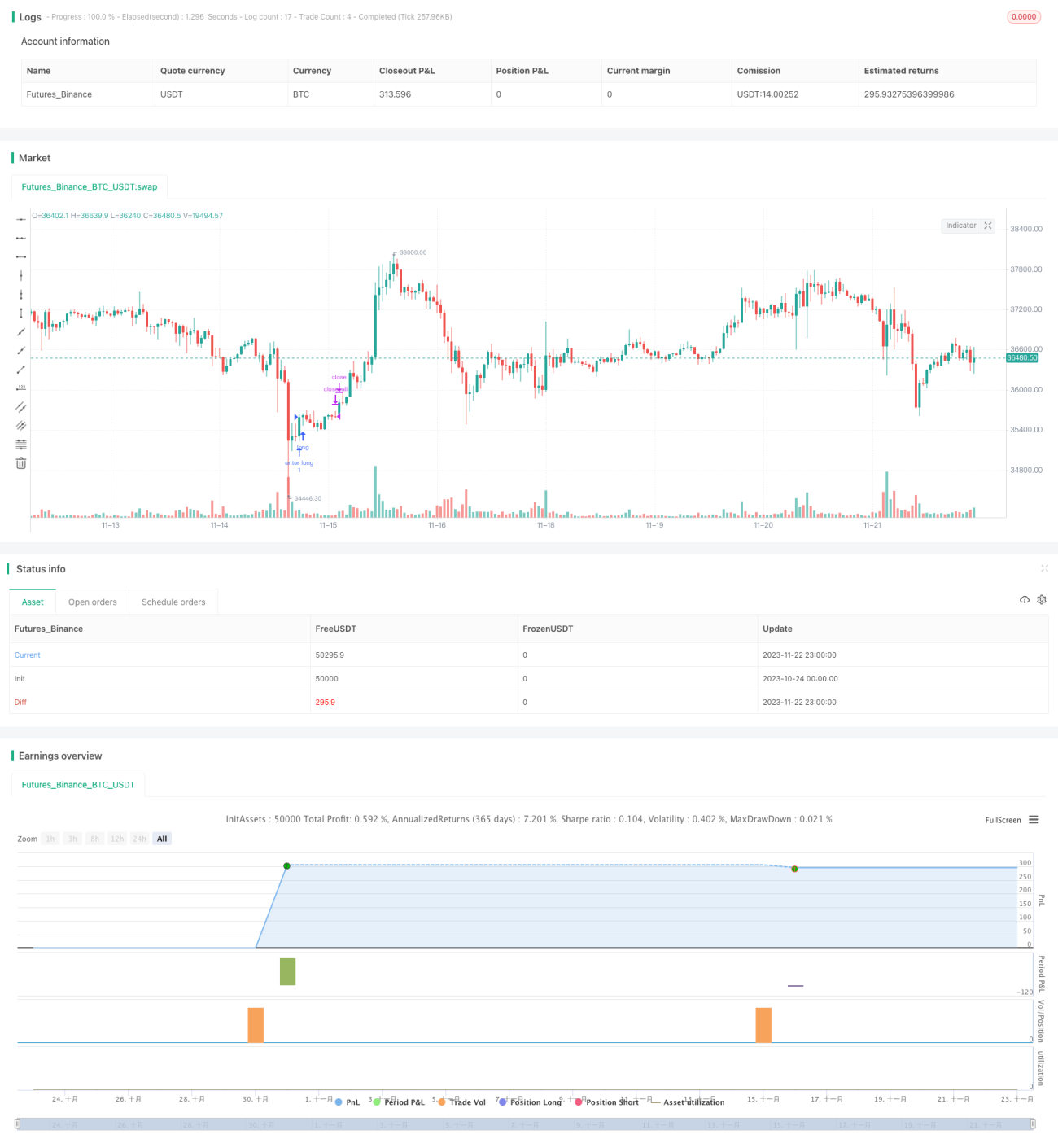

反転キャッチ戦略は、ボラティリティ指標であるボリンジャーバンドとモメンタム指標であるRSIを組み合わせた反転取引戦略です。ボリンジャーバンドのチャネルとRSIの買われすぎ/売られすぎラインをシグナルとして設定し、トレンド方向が転換するタイミングで反転の機会を捉えて取引を行います。

戦略の原理

本戦略は、主要なテクニカル指標としてボリンジャーバンドを使用し、補助的にRSIなどのモメンタム指標で取引シグナルを検証します。具体的なロジックは以下の通りです。

- 大周期のトレンド方向を判断し、上昇トレンドか下降トレンドかを判定します。50日EMAと21日EMAのゴールデンクロス・デッドクロスを用いて判断します。

- 下降トレンドにおいて、価格が上昇してボリンジャーバンドの下限を突破し、かつRSI指標が売られすぎゾーンから反発しゴールデンクロスが出現した場合、売られすぎゾーンで底値が固まったと判断し、買いシグナルとします。

- 上昇トレンドにおいて、価格が下落してボリンジャーバンドの上限を突破し、かつRSI指標が買われすぎゾーンから下落しデッドクロスが出現した場合、買われすぎゾーンで調整が始まったと判断し、売りシグナルとします。

- 上記の買い・売りシグナルはすべて同時に満たされる必要があり、偽シグナルを排除します。

優位性分析

本戦略には以下の優位性があります。

- ボラティリティ指標とモメンタム指標を組み合わせているため、シグナルの信頼性が高い。

- 反転取引はリスクが比較的小さく、短期売買に適している。

- プログラム化のルールが明確であり、自動売買の実装が容易。

- トレンド取引と組み合わせることで、レンジ相場での無秩序なエントリーを回避できる。

リスク分析

本戦略には以下のリスクも存在します。

- ボリンジャーバンドのチャネル突破による偽シグナルのリスクがあり、RSI指標によるフィルターが必要。

- 反転失敗のリスクがあるため、適切な損切りが必要。

- 反転のタイミングを正確に捉えられないリスクがあり、早期参入や最適なポイントを逃す可能性がある。

以上のリスクに対しては、損切りの位置を設定してリスクエクスポージャーをコントロールするとともに、パラメータを最適化してボリンジャーバンドの期間やRSIパラメータを調整することができます。

最適化の方向性

本戦略は主に以下の方向で最適化が可能です。

- ボリンジャーバンドのパラメータを最適化し、期間の長さと標準偏差の大きさを調整して最適なパラメータ組み合わせを探す。

- 移動平均線の期間を最適化し、トレンド判断に最適な期間の長さを決定する。

- RSIのパラメータを調整し、最適な買われすぎ・売られすぎ領域の範囲を探す。

- KDJやMACDなどの他の指標を追加し、エントリー理由を豊富にする。

- 機械学習アルゴリズムを追加し、AI技術を活用して最適なパラメータを自動的に探索する。

まとめ

反転キャッチ戦略は、全体的に見て効果の高い短期取引戦略です。トレンド判断と反転シグナルを組み合わせることで、レンジ相場での偽シグナルをフィルタリングしつつ、トレンド相場でトレンドに対抗することを避け、リスクをコントロールできます。パラメータやモデルを継続的に最適化することで、より良い戦略効果を得ることができます。

Source

Pine

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This is an Open source work. Please do acknowledge in case you want to reuse whole or part of this code.

// Please see the documentation to know the details about this.

//@version=5Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1