低点ピラミッド低リスク追跡戦略

本戦略は、異なる指標を組み合わせて価格変動中の潜在的な底値を特定し、ピラミッドトラッキングにより段階的に建玉を積み上げることでリスクを低減します。また、ストップロス、利確、トレーリングストップなどの機能を組み合わせ、リスクを効果的に制御できます。

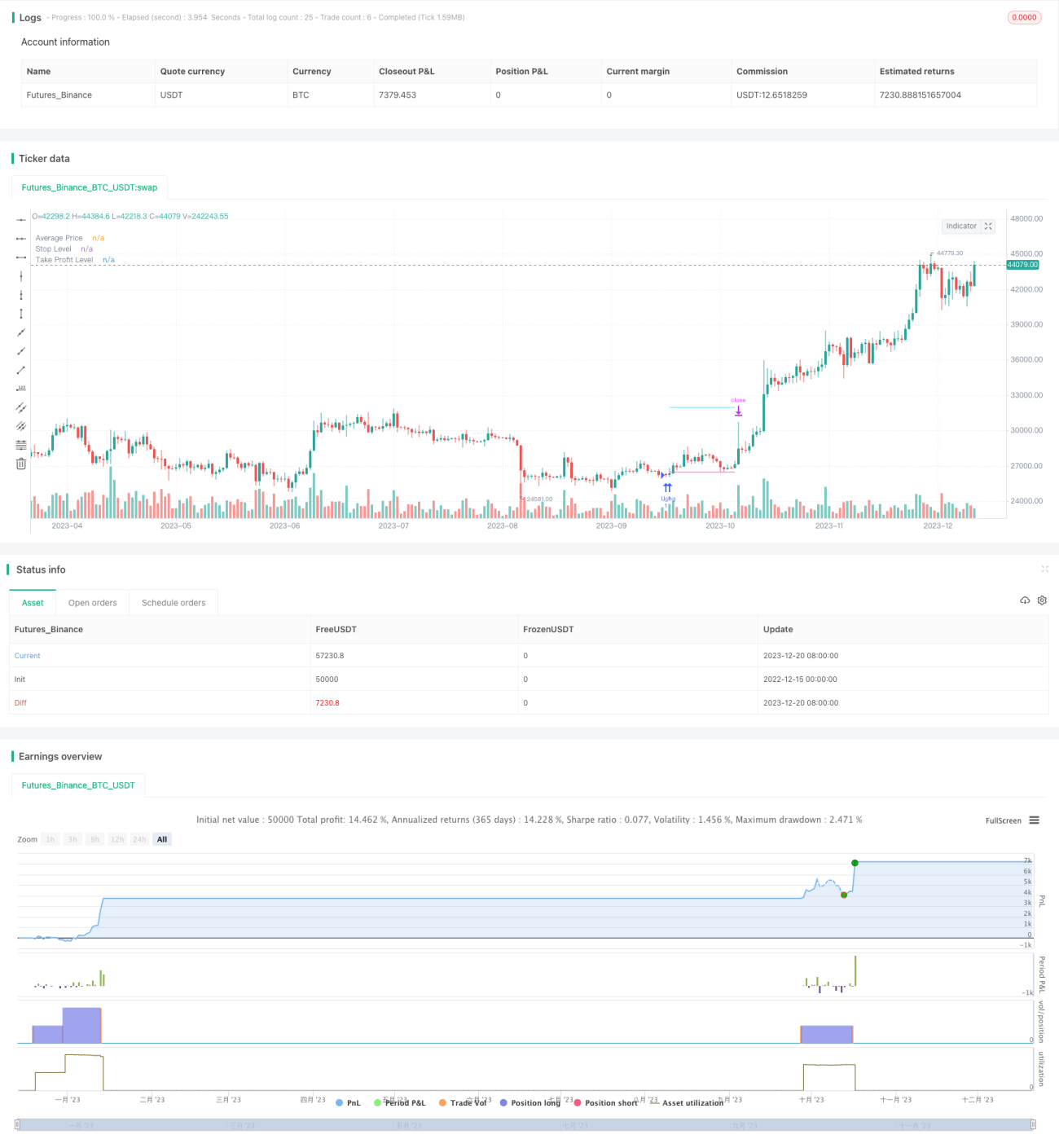

戦略概要

本戦略はまず、RSIとEMA RSIの差を利用して価格の潜在的な底値を特定します。偽のシグナルを除去するため、移動平均線やマルチタイムフレームのストキャスティクス指標も組み合わせて確認を行います。底値シグナルが確認されると、そのポイントよりやや低い位置に段階的に買い注文を入れていきます。これがトラッキングピラミッドの考え方です。最大12件のトラッキング注文を許容し、各注文の数量は順に増加していくため、リスクを効果的に分散できます。すべての注文は全体のストップロスに従って決済され、さらに各注文ごとに個別の利確を設定することも可能です。リスクをさらに制御するため、口座残高のパーセンテージに基づく全体ストップロスも設定しています。

戦略の原理

本戦略は主に、底値識別モジュール、ピラミッドトラッキングモジュール、リスク制御モジュールの3つの部分で構成されています。

底値識別モジュールでは、RSI指標とそのEMAの差を利用して価格の潜在的な底値を識別します。精度を高めるため、移動平均線指標とマルチタイムフレームのストキャスティクス指標も導入し、シグナルをフィルタリングします。価格が移動平均線より低く、かつストキャスティクスのK線が30未満の場合にのみ、底値シグナルが有効と判断されます。

ピラミッドトラッキングモジュールが本戦略の核です。底値シグナルが確認されると、その底値よりさらに0.1%低い位置に最初の注文を入れます。その後、価格が下落し続け、平均エントリー価格よりも一定の割合低くなった場合、買い注文を追加していきます。新たな注文の数量は順に増加し、例えば3番目の注文は最初の注文の3倍の数量となります。このピラミッドトラッキング方式によりリスクを平均化できます。本戦略では最大12件のトラッキング注文を許容しています。

リスク制御モジュールは主に3つの側面から構成されます。第一に全体ストップロスで、最近の一定期間内の最高値に基づいて計算されたストップロス水準です。すべての注文はこのストップロス水準に従って同時に決済されます。第二に各注文ごとの独立した利確で、エントリー価格に対する一定割合での利確が可能です。第三に口座残高比率に基づく全体ストップロスで、最も強力なリスク制御手段です。

戦略のメリット

- ピラミッドトラッキングにより個別注文のリスクを低減し、同時に全体リスクを分散

- 複数指標の組み合わせにより底値識別の精度を向上

- 全体ストップロス、利確、トレーリングストップ機能によりリスクを効果的に制御

- 残高比率によるストップロス機能で口座を大きな損失から保護

- パラメータ調整によりリスクとリターンのバランスを見つけられる

戦略のリスク

- 底値識別の精度にはまだ限界があり、最適なエントリーポイントを逃したり、偽シグナルに引っかかる可能性がある

- 注文追加時に不利な相場に遭遇し、損失が拡大するリスクがある

- 戦略のメリットを発揮するには長めの運用期間が必要

- パラメータ設定を誤るとリスク制御が不十分になる可能性がある

上記のリスクを低減するため、以下の点から最適化が可能です。

- 指標の変更や追加により、底値識別の精度を高める

- 注文数量、間隔、利確幅などのパラメータを最適化し、個別注文のリスクを低減する

- ストップロス幅を適切に短縮し、利益を保護する

- 異なる銘柄でテストし、流動性が高く変動の大きい銘柄を選択する

戦略の最適化方向性

本戦略にはさらなる最適化の余地があります。

- 機械学習などより高度な技術を導入して底値を識別する試み

- 市場の状態に応じて注文数量やストップロス幅などのパラメータを動的に調整

- ボックス内ストップロス戦略を追加し、損失拡大を防ぐ

- 再エントリー機能の追加

- 株式や暗号通貨の銘柄における戦略パラメータの最適化

まとめ

本戦略は、ピラミッドトラッキングの考え方により個別注文のリスクを効果的に低減し、全体ストップロス、利確、トレーリングストップなどの機能もリスク制御に優れた役割を果たしています。ただし、底値識別などにはまだ最適化の余地があり、より高度な技術の導入や動的パラメータ調整機能の追加、パラメータ最適化により、本戦略のリスク・リターン比は大幅に向上するでしょう。

- 1