クオンツモデルに基づいてカスタマイズされた高効率なクオンツ取引戦略

概要

本戦略は、定量モデルに基づいてカスタマイズされた、高効率な定量取引戦略です。戦略はModelius Volumeモデルを基本モデルとして使用し、その上で拡張と最適化が施されています。この戦略はマーケット内の定量取引機会を捉え、安定した利益を実現できます。

戦略の原理

本戦略の中核はModelius Volumeモデルです。このモデルは価格と取引量の変化を利用して、マーケットにおける定量取引機会を識別します。具体的には、戦略はclose価格、open価格、最高値、最安値を組み合わせ、一定のルールに従って現在のローソク足の方向を計算します。ローソク足の方向が変化した際に、取引量の大小によって定量取引機会の質を判断します。さらに、戦略はSAR指標と移動平均線指標を組み合わせ、エントリーとイグジットのタイミングを補助的に判断します。

基本的な取引ロジックは、指標が負の値から正の値にブレイクした場合にロング、正の値から負の値にブレイクした場合にショートとします。また、戦略にはストップロス、利確、トレーリングストップが設定されており、リスクを管理します。

優位性分析

本戦略の最大の利点は、Modelius Volumeモデルを活用することで定量取引機会を効果的に識別できる点です。従来のテクニカル指標と比較して、このモデルは取引量の変化により注目しており、現在の高頻度定量取引において非常に実用的です。さらに、戦略のエントリールールは比較的厳格であり、定量取引機会を逃すリスクを抑えつつ、不要なエントリーの確率も最小限に抑えることができます。

リスク分析

本戦略の主なリスクは、Modelius Volumeモデル自体がノイズを完全に回避できないことです。市場に異常な変動が発生した場合、取引シグナルに誤りが生じる可能性があります。また、戦略内のパラメータ設定も最終結果に影響を与えます。

リスクを管理するためには、パラメータを適切に調整し、他の指標と組み合わせて補助判断を行うことが可能です。また、ストップロスや利確の位置を適切に設定することも必要です。

最適化の方向性

本戦略にはまだ最適化の余地があります。例えば、機械学習アルゴリズムを組み合わせてパラメータ設定を動的に最適化することが考えられます。あるいは、感情分析などの指標を組み合わせて判断の精度を高めることも可能です。また、異なる銘柄間の相関関係を研究し、マルチ銘柄アービトラージモデルを構築することも検討できます。

まとめ

総じて、本戦略はModelius Volume定量モデルの利点を活用し、操作性の高い定量取引戦略を設計しています。パラメータ調整、モデル拡張、機械学習などを通じて最適化・向上させることができ、実際の取引で良好な安定収益を得ることが期待できます。

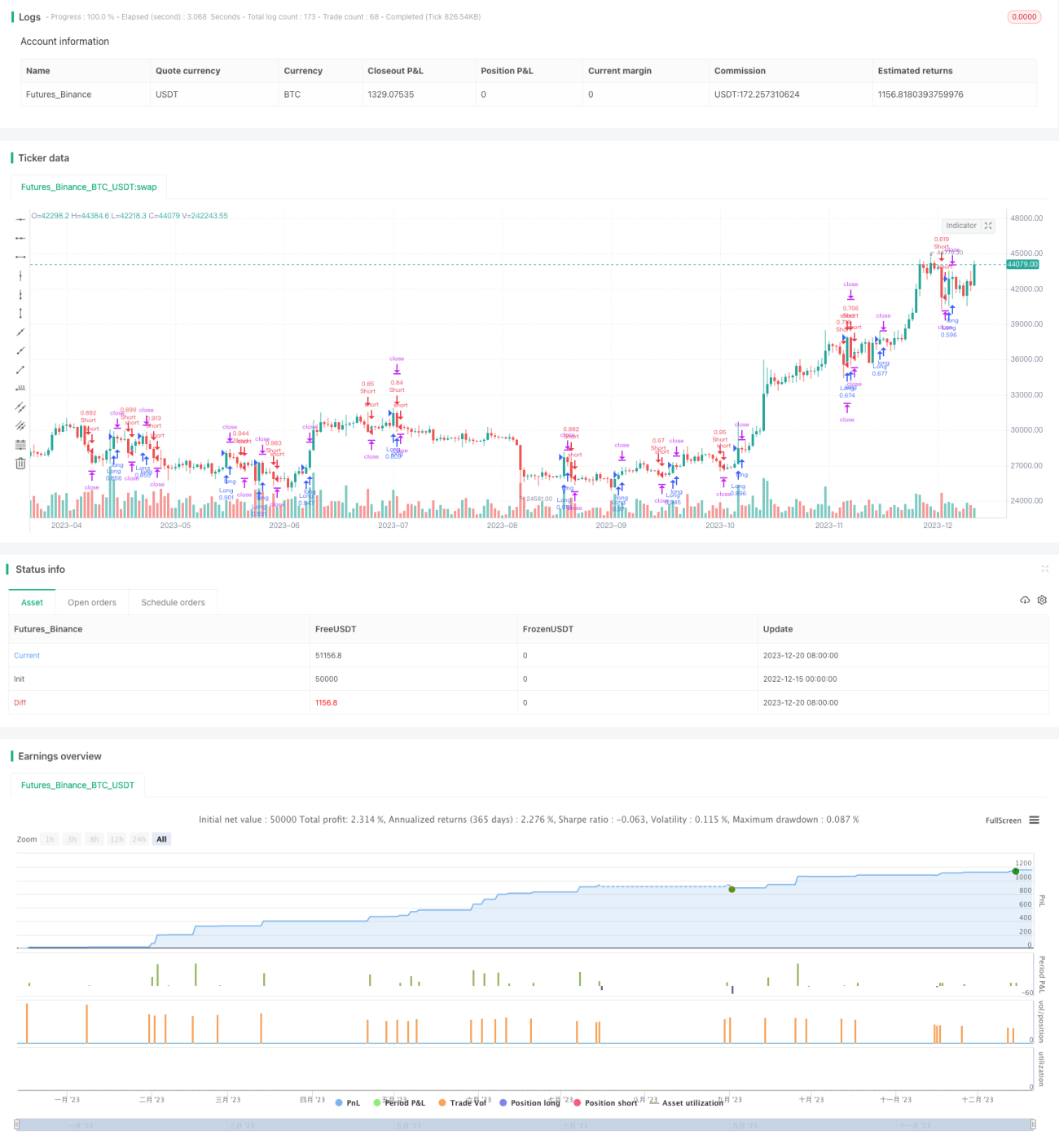

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

strategy(title="strategy modelius volume model ", shorttitle="mvm",overlay=true, calc_on_order_fills=true, default_qty_type=strategy.percent_of_equity, default_qty_value=50, overlay=false)

- 1