ダイナミックCCIサポート・レジスタンス戦略

1

Follow

1802

Followers

概要

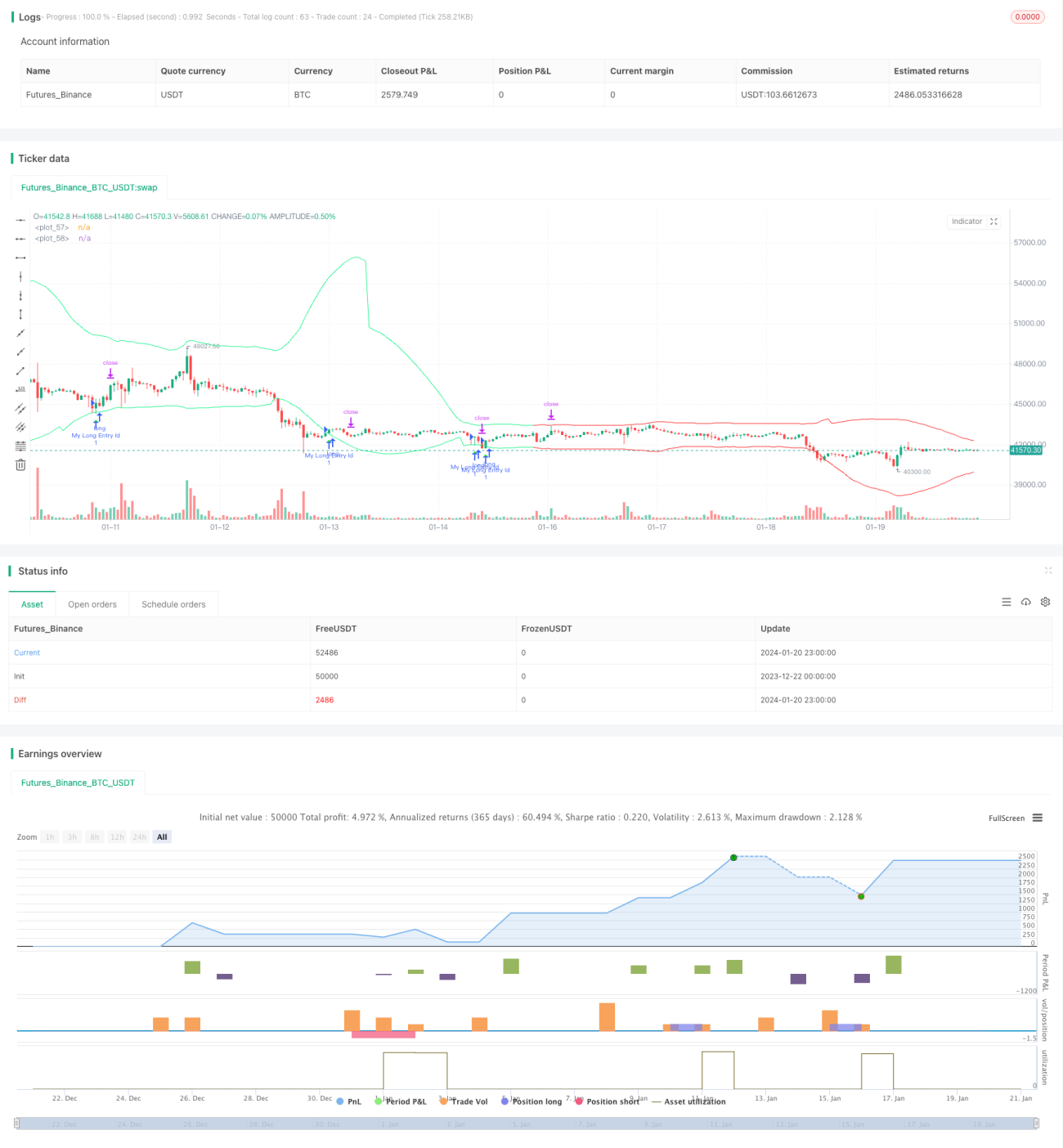

本戦略はCCI指標のピボットポイントを用いて動的サポートラインとレジスタンスラインを計算し、トレンド判断を組み合わせて買い・売りシグナルを探します。CCIの反転特性とトレンド追従能力を融合し、中期トレンド中の反転ポイントを捉えて利益を上げることを目的としています。

戦略原理

CCI指標は市場が過度に弱気または強気かを示し、80と-80の極限値を用いて市場が買われすぎ・売られすぎの状態かを判断できます。本戦略はこの特性を利用し、左右50本のローソク足のピボットポイントを計算して上部ピボットポイントと下部ピボットポイントを求め、それにバッファを加減して動的レジスタンスラインとサポートラインを構築します。

終値が始値より高く、かつ上部サポートラインより低い場合に買いシグナルを生成し、終値が始値より低く、かつ下部レジスタンスラインより高い場合に売りシグナルを生成します。非主流トレンド方向のシグナルをフィルタリングするため、EMAとスロープ指標を併用して現在の主流トレンド方向を判断します。トレンドが強気と判断された場合のみ買い、弱気と判断された場合のみ売りを行います。

ストップロスと利確はATR指標に基づき動的に計算されるため、リスク管理も合理的です。

優位性分析

- CCI指標の反転特性を利用し、反転ポイント付近で売買することで利益獲得確率を高める。

- トレンド判断と組み合わせることで逆張りを避け、損失を軽減する。

- 動的ストップロス・利確設定によりリスク管理がより合理的。

- CCI周期やバッファサイズなどのパラメータをカスタマイズ可能で、様々な市場環境に対応。

リスク分析

- CCI指標は偽シグナルを発生しやすいため、トレンドフィルターとの組み合わせが必要。

- 反転が必ず成功するとは限らず、損失が発生する可能性がある。

- パラメータ設定が不適切だと、取引が過剰になったり機会を逃したりする可能性。

パラメータ最適化やストップロス幅の調整などによりリスクを低減できます。また、本戦略は他の指標の補助ツールとしても活用でき、取引シグナルに完全依存する必要はありません。

最適化の方向性

- バッファサイズを最適化し、異なるボラティリティの市場に対応する。

- ATRの周期パラメータを最適化し、より正確な動的ストップロス・利確を実現する。

- 異なるCCIパラメータ設定を試す。

- 他のタイプのトレンド判断指標の効果を検証する。

まとめ

本戦略はCCI指標の買われすぎ・売られすぎの選別能力とトレンド判断によるフィルタリング確認を統合しており、実践的な価値があります。動的ストップロス・利確により、実際の運用でもリスクを管理できます。パラメータ最適化と改善により、さらなる効果が期待できます。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1