複数のテクニカル指標に基づくモメンタムトレンド戦略

1

Follow

1802

Followers

概要

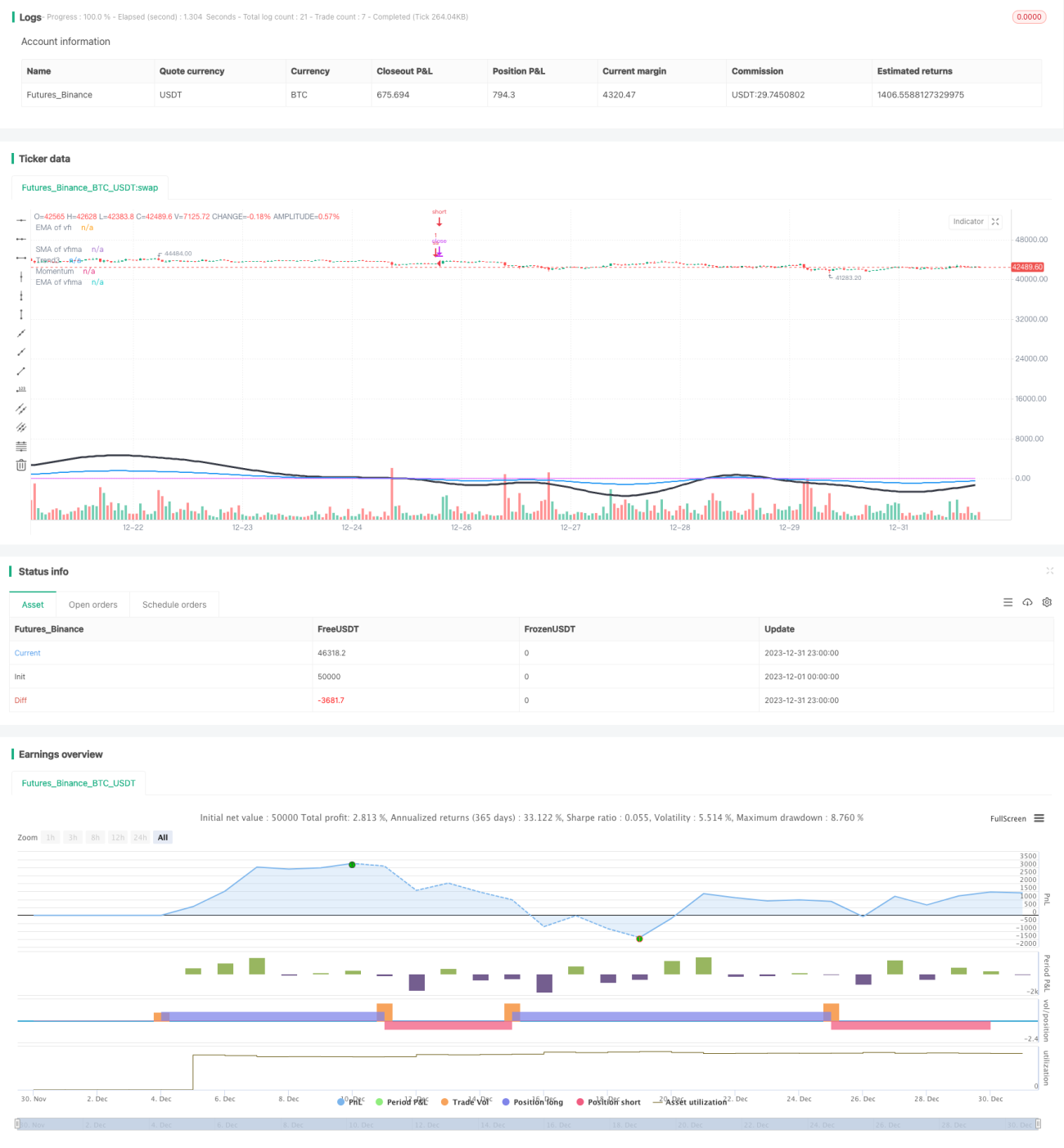

本戦略は、移動平均線、相対力指数(RSI)、出来高変動指数(VFI)、真実強度指数(TSI)など、複数のテクニカル指標を総合的に活用し、市場の全体的なモメンタムと方向性を判断して中長期的な価格動向を捉えます。

戦略の原理

- 高速線RSI(7日)、通常線RSI(14日)、低速線RSI(50日)の移動平均線を計算し、RSIの強気・弱気トレンドとモメンタムを判断します。

- VFIとVFIの移動平均線であるEMA(25日)、SMA(25日)を計算し、市場への資金流入・流出状況を判断します。

- TSIの長期平均線と短期平均線の比率を計算し、市場のトレンド強度を判断します。

- RSI、VFI、TSIの結果を統合し、市場の全体的なモメンタムの方向性を導き出します。

- 市場に下落モメンタムが存在すると判断された場合にショートし、モメンタムが反転したと判断された場合にショートポジションを手仕舞います。

優位性分析

- 複数の指標を組み合わせることで、市場全体のモメンタムとトレンドをより包括的かつ正確に判断できます。

- VFIが市場の資金流入・流出状況を反映するため、逆張り取引を回避できます。

- TSIがレンジ相場をフィルタリングするため、シグナルの信頼性が高まります。

- 全体的に、本戦略の信頼性は高く、勝率も良好です。

リスク分析

- 複数指標の組み合わせによりパラメータ設定が複雑であり、最適なパラメータを見つけるには繰り返しテストが必要です。

- エントリーとイグジットの戦略がシンプルで、指標が提供する情報を十分に活用できず、超短期間での反転による損失が発生する可能性があります。

- レンジ相場では、誤ったシグナルや小規模な逆行損失が発生しやすくなります。

最適化の方向性

- 指標のパラメータ組み合わせを最適化し、最適なパラメータを見つけます。

- イグジットルールを追加し、指標状況を利用して反転を判断して手仕舞います。

- 利益保護メカニズムを追加し、レンジ相場での小損失を削減します。

まとめ

本戦略は複数の指標を統合して市場全体のモメンタムを判断し、市場に下落モメンタムが存在する場合にショートして利益を得ます。本戦略の信頼性は高いものの、エントリーとイグジットの仕組みが比較的シンプルであり、指標情報が十分に活用されていません。パラメータの継続的な最適化とイグジットルールの強化により、戦略の安定性と収益性をさらに向上させることができます。

Source

Pine

//@version=2

//credit to LazyBear, Lewm444, and others for direct and indirect inputs/////////////////////////////////

//script is very rough, publishing more for collaborative input value than as a finished product/////////

strategy("Momo", overlay=true)

length = input( 50 )

overSold = input( 50 )

overBought = input( 65 )

price = ohlc4

/////////////////////////////////////////////////////macd/////////////////////////////////////////////////

fastLength = input(12)Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1