収縮ボリンジャーバンドとRSIのコンビネーション戦略

概要

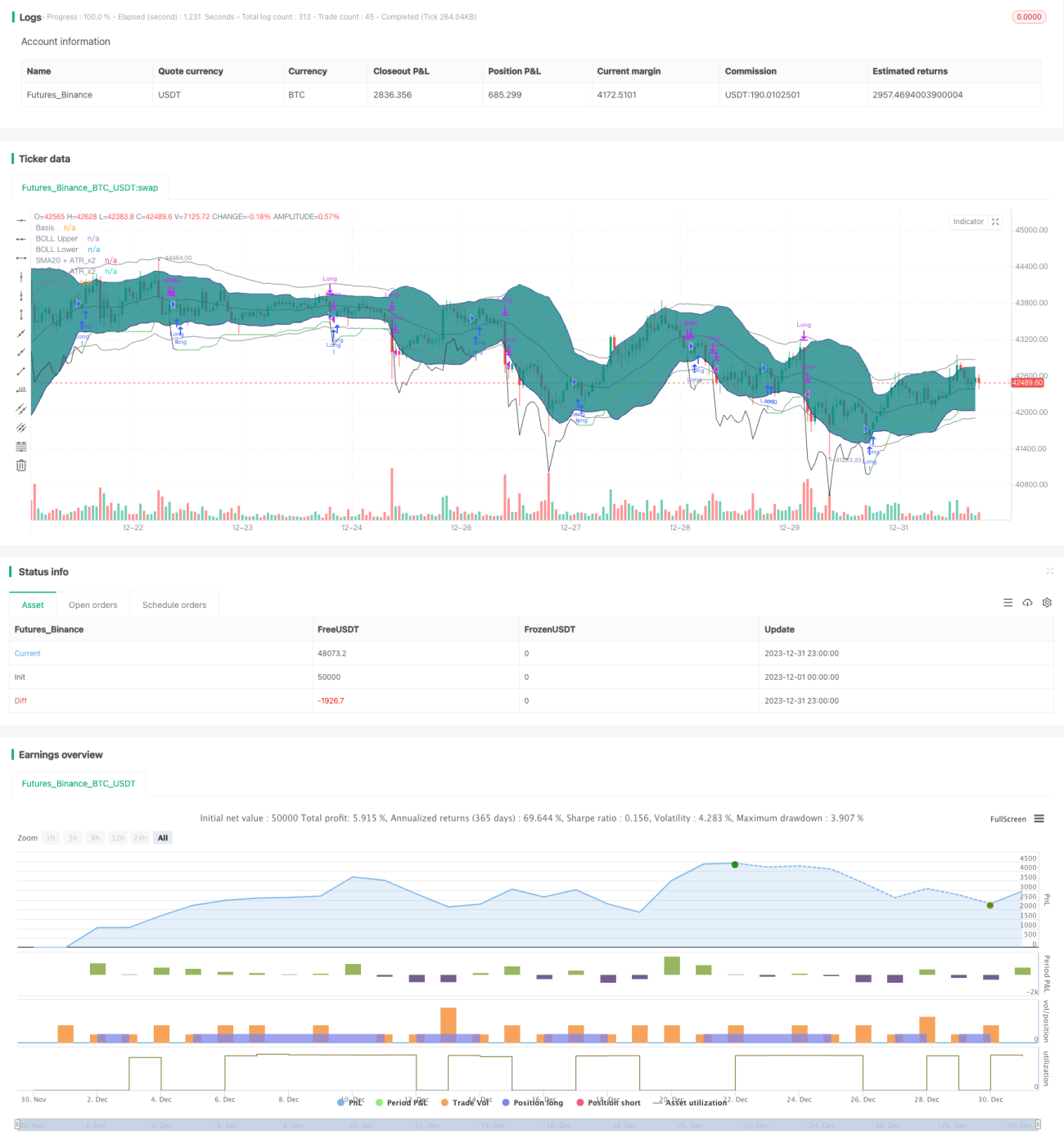

本戦略は、ボリンジャーバンドと相対力指数(RSI)を組み合わせ、バンド収縮期にRSI上昇が確認されたタイミングを捉え、トレンドフォロー型のストップでリスク管理を行います。

戦略の仕組み

本戦略の取引ロジックの中核は、ボリンジャーバンドの収縮を識別し、RSIが上昇基調にあるときにトレンドが上昇初期段階にあると判断する点にあります。具体的には、20日間のボリンジャーバンド中央線における標準偏差がATR×2を下回る場合にバンド収縮と判定します。同時に、10日と14日のRSIがいずれも上昇傾向にあれば、価格が間もなくボリンジャーバンドの上限を突破すると予想し、買いポジションを取ります。

ポジションエントリー後は、ATRによる安全距離に加え、価格上昇に伴うトレーリングストップで利益を確定しリスクを管理します。価格がストップラインを割り込むか、RSIが過熱状態(14日RSIが70超、10日RSIが14日RSIを上回る)になった場合に決済します。

優位性分析

本戦略の最大の優位性は、ボリンジャーバンドの収縮を用いて相場の整理局面を判断し、RSI指標と組み合わせることで価格のブレイク方向を予測する点にあります。また、固定ストップではなく適応型ストップを採用しているため、市場の変動に応じて柔軟に調整でき、リスクを適切に管理しながらより大きなリターンを得ることが可能です。

リスク分析

本戦略の主なリスクは、ボリンジャーバンド収縮とRSI上昇を認識した際に、相場が偽のブレイクアウトである可能性があることです。また、ストップロスに関しては、変動が大きすぎる場合に適応型ストップが間に合わない恐れがあります。このリスクは、ストップ方式の改良(例:カーブストップ)によって低減できます。

最適化の方向性

本戦略は以下の点から最適化が可能です。

- ボリンジャーバンドのパラメータ設定を改善し、収縮判定を最適化する

- 異なるRSIの期間パラメータを試す

- 他のストップ方式(カーブストップ、トレーリングストップなど)の効果を検証する

- 銘柄の特性に応じてパラメータを調整する

まとめ

本戦略は、ボリンジャーバンドとRSIの補完性を活用し、リスク管理を考慮しながら良好なリスク対収益比を実現しています。今後はストップ方式やパラメータ選択などを最適化することで、より多様な取引銘柄に適用可能となります。

- 1