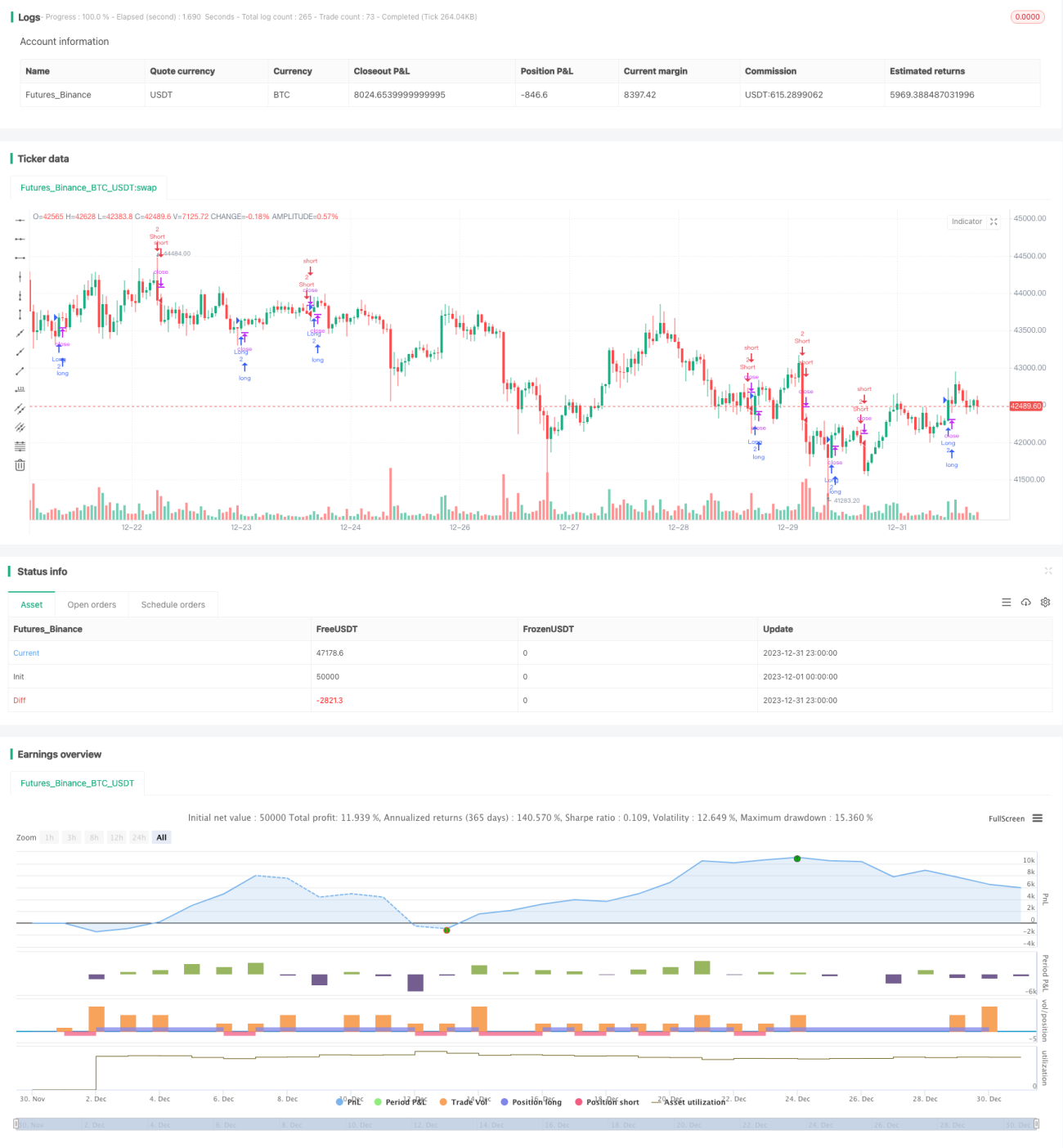

K線に基づく双方向ブレイクアウト取引戦略

概要

これは、ローソク足に基づく双方向ブレイクアウト取引戦略です。現在のローソク足の終値が、前の2本のローソク足の高値と安値の両方を超えたときに、取引シグナルを生成します。

戦略の原理

本戦略の基本的なロジックは以下の通りです。

-

強気シグナルの定義:

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]。すなわち、現在のローソク足の終値が始値より大きく、かつ前の2本のローソク足の高値よりも大きく、現在のローソク足の安値が前のローソク足の安値よりも低い。 -

弱気シグナルの定義:

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]。すなわち、現在のローソク足の終値が始値より小さく、かつ前の2本のローソク足の安値よりも小さく、現在のローソク足の高値が前のローソク足の高値よりも高い。 -

強気シグナルが発生したら買い、弱気シグナルが発生したら売り。

-

ストップロスと利確ラインを設定可能。

本戦略は、重要な価格帯のブレイクアウトを利用してトレンドの変化を判断し、取引シグナルを生成する、双方向ブレイクアウトの特徴を活用しています。

メリット分析

比較的シンプルで直感的なブレイクアウト戦略であり、以下のようなメリットがあります。

-

ロジックが明確で、理解・実装が容易であり、敷居が低い。

-

ブレイクアウトは一般的な取引シグナルであり、トレンドが形成されやすい。

-

買いと売りの両方を行うことができるため、双方向取引により利益獲得の機会が増える。

-

ストップロスと利確を柔軟に設定でき、リスク管理が可能。

リスク分析

本戦略には以下のようなリスクも存在します。

-

双方向取引はリスクが大きく、綿密な監視が必要。

-

ブレイクアウトはダマシに遭いやすく、偽のシグナルが発生する可能性がある。

-

パラメータ設定が不適切な場合、過剰取引につながる恐れがある。

-

ストップロスや利確の設定が不適切だと、利益幅に悪影響を及ぼす。

パラメータの最適化や適切な銘柄選別により、リスク軽減が可能です。

最適化の方向性

本戦略は以下の点で最適化が可能です。

-

パラメータの最適化(ブレイクアウト期間パラメータ、ストップロス・利確の幅など)。

-

フィルター条件を追加し、レンジ相場やダマシによる誤シグナルを回避。

-

トレンド指標と組み合わせ、揉み合い範囲を避ける。

-

資金管理の最適化、ポジションサイズアルゴリズムの改良。

-

銘柄ごとにパラメータが異なるため、個別にテスト・最適化を行う。

まとめ

本戦略は、双方向ブレイクアウトの考え方に基づくシンプルな戦略です。ロジックが明確で実装が容易という利点がある一方、一定の監視リスクも伴います。パラメータや条件の最適化を通じて、良好な戦略効果が期待できます。

- 1