動的追加建て戦略に基づく

1

Follow

1802

Followers

概要

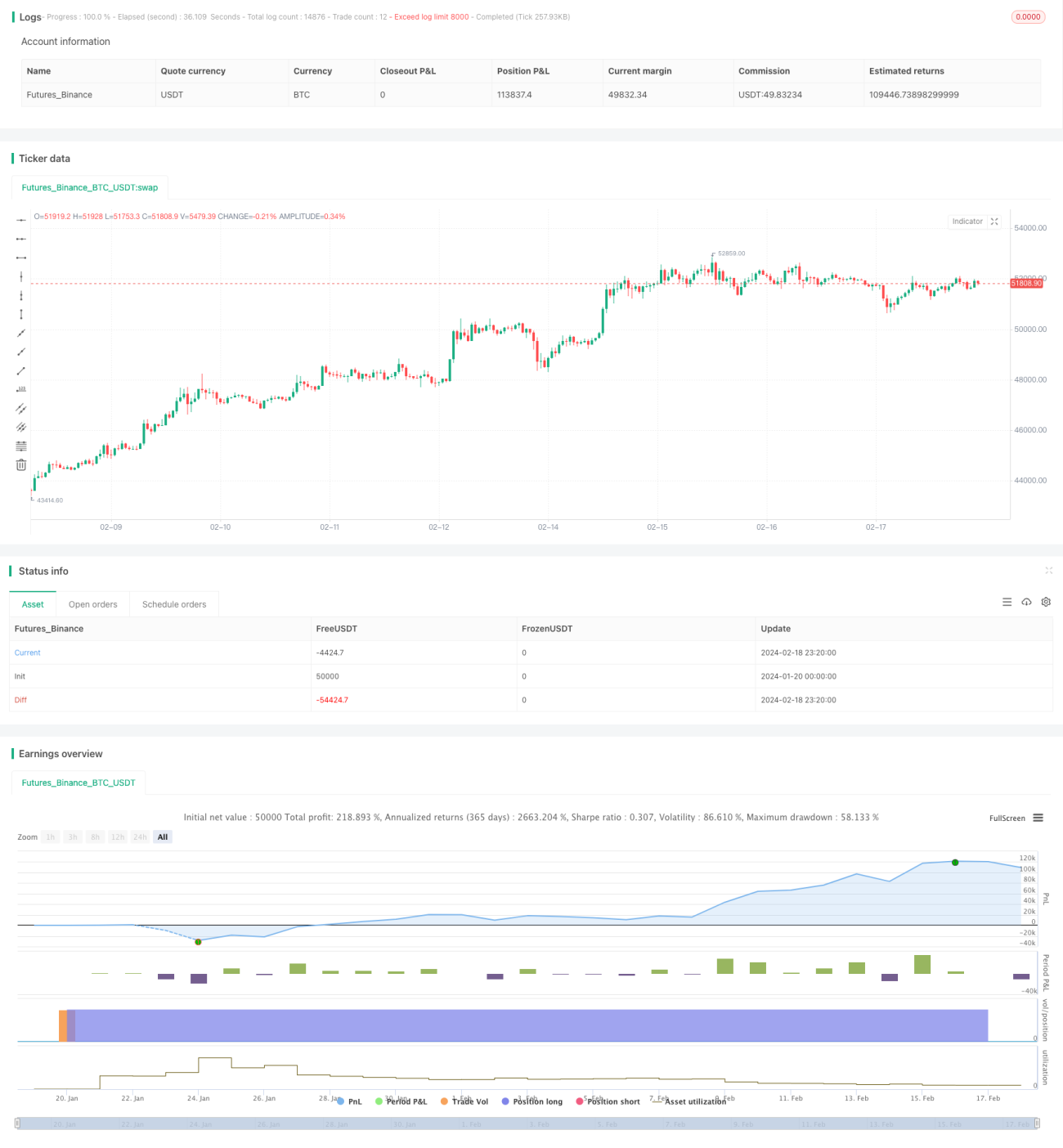

本戦略の主なアイデアは、システムシグナルに基づいて動的にポジションを追加し、強気相場で徐々にポジションを構築することで、リスクを管理し、平均エントリー価格を低く抑えることです。

戦略の仕組み

本戦略ではまず、開始資金とDCA設定割合を設定します。各ローソク足の終値時点で、価格変動に基づいて調整後の設定割合を計算します。価格が上昇した場合は割合を引き下げ、価格が下落した場合は割合を引き上げます。これにより、価格が低いときにポジションを増やすことができます。次に、調整後の割合と残りの資金に基づいて注文サイズを計算します。各ローソク足の終了時に、開始資金を使い切るまでポジションを追加する注文を出します。

これにより、相場変動に合わせてリスクを管理し、平均エントリー価格を低く抑えることができます。同時に、平均エントリー価格と中央値価格を集計することで、現在のエントリー状況を判断できます。

メリット分析

本戦略には以下のメリットがあります。

- 相場下落時にはポジションを増やし、相場上昇時にはポジションを減らすことで、リスクをコントロールできる。

- 中央値価格よりも低い平均エントリー価格を達成でき、より高い収益余地を得られる。

- 強気相場の変動相場に適しており、良好なリスク・リターン比を得られる。

- 開始資金とDCA割合を事前に設定することで、一度の追加ポジションの資金量を管理し、過大なリスクを回避できる。

- 平均エントリー価格と中央値価格の統計情報を提供し、エントリーの良し悪しを直感的に判断できる。

リスク分析

本戦略には以下のリスクも存在します。

- 相場が急落した場合、戦略はポジションを追加し続けるため、大きな資金損失を招く可能性がある。ストップロスを設定することでリスクを抑えられる。

- 相場が急上昇した場合、追加ポジションの幅が減少し、上昇の大部分を逃す可能性がある。その場合は他のシグナルを利用して迅速なLSI(レバレッジ戦略?)を行う必要がある。

- パラメータ設定が適切でない場合もリスクが生じる。開始資金が大きすぎる、DCA割合が高すぎると損失が拡大する。

最適化の方向性

本戦略は以下の点で最適化が可能です。

- ストップロスロジックを追加し、大幅下落時にはポジション追加を停止する。

- ボラティリティなどの指標に基づいてDCA割合を動的に調整する。

- 機械学習モデルを追加し、価格変動を予測してポジション追加の判断を支援する。

- 他のテクニカル指標と組み合わせて市場構造を判断し、構造の転換点でポジション追加を停止する。

- 資金管理モジュールを追加し、口座資金状況に応じて毎回の追加資金を動的に調整する。

まとめ

本戦略は非常に実用的な動的ポジション追加戦略です。相場の変動に合わせて柔軟にポジションを調整し、強気相場で低い平均エントリー価格を実現できます。また、リスクを管理するためのパラメータ設定が組み込まれています。他のテクニカル指標やモデルと組み合わせることで、さらなる効果が期待できます。本戦略は長期投資による利益を追求する投資家に適しています。

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1