圧縮指標に基づくマルチタイムフレーム取引戦略

概要

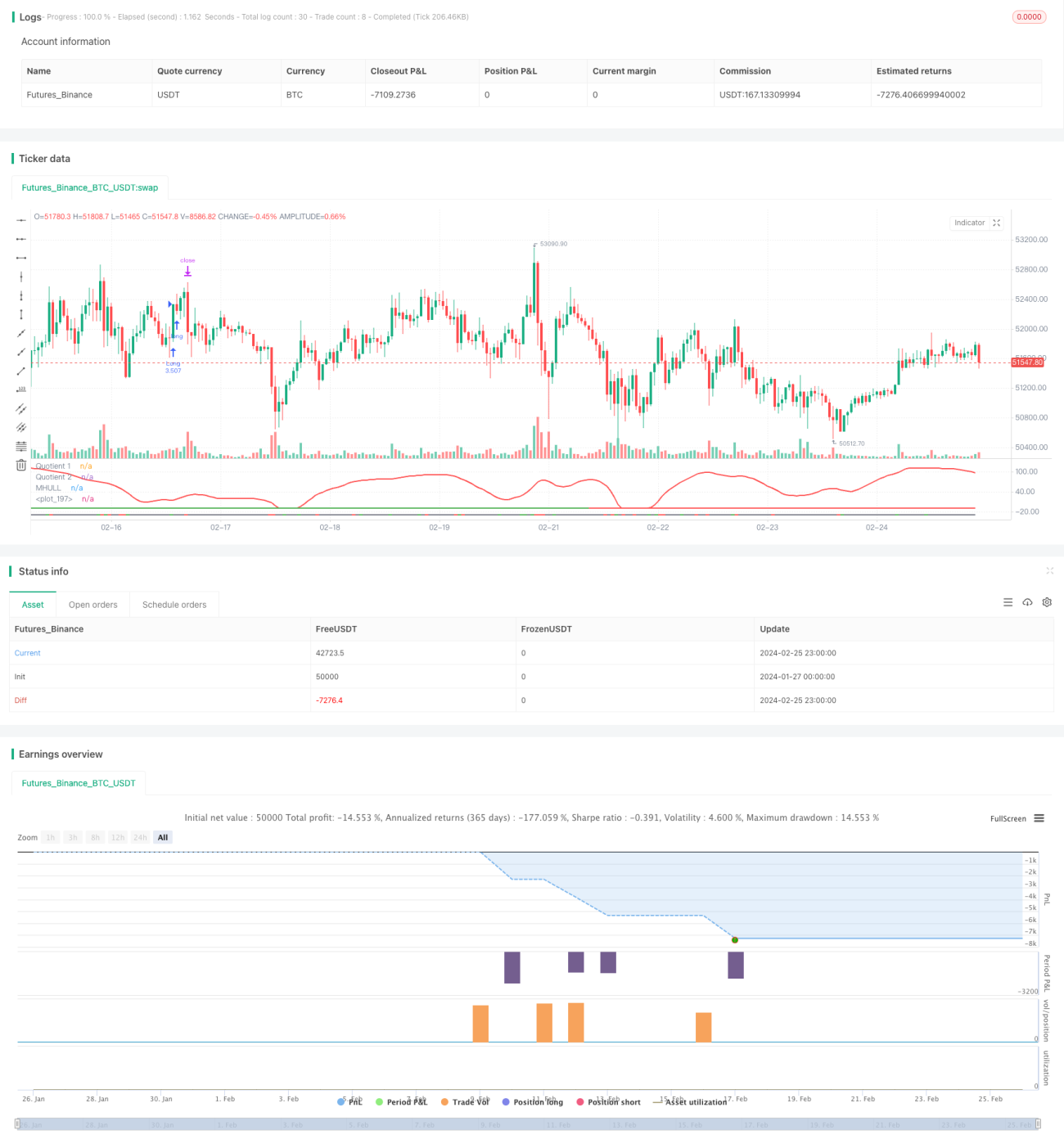

本戦略は、ブームハンター(Boom Hunter)、ハルスイート(Hull Suite)、ボラティリティオシレーター(Volatility Oscillator)の3つの指標を組み合わせ、マルチタイムフレームでトレンド追跡とブレイクアウト取引を行う定量戦略です。本戦略は、ビットコインなど、高いボラティリティと突発的な価格変動を特徴とするデジタルアセットに適しています。

原理

本戦略の核となるロジックは、以下の3つの指標に基づいています。

-

ブームハンター(Boom Hunter): インジケーター圧縮技術を利用したオシレーターで、2つの指標(Quotient1とQuotient2)のクロスにより買いシグナルと売りシグナルを判断します。

-

ハルスイート(Hull Suite): 平滑化移動平均線の一種で、中央線と上下のバンドの関係からトレンド方向を判断します。

-

ボラティリティオシレーター(Volatility Oscillator): 価格変動の情報を定量化するオシレーター指標です。

本戦略のエントリーロジックは、ブームハンターの2つのQuotient指標が上向きまたは下向きにクロスすると同時に、価格がハル中央線をブレイクし、上バンドまたは下バンドとダイバージェンスを起こし、かつボラティリティ指標が買われすぎ・売られすぎの領域にあることです。これにより、偽のブレイクアウトシグナルをフィルタリングし、エントリーの精度を高めます。

ストップロスは、一定期間(デフォルト20本のローソク足)の最低谷または最高峰を検索して設定し、利益はストップロスのパーセンテージに構成された利確倍率(デフォルト3倍)を掛けて取得します。ポジションサイズは、口座総資産のパーセンテージ(デフォルト3%)と特定銘柄のストップロス幅に基づいて計算されます。

利点

- 圧縮指標技術を利用して価格から主要な取引シグナルを抽出し、勝率を向上

- 複数の指標を組み合わせて検証することで、偽のブレイクアウトを回避し、トレンド方向を正確に判断

- 動的なストップロスと利確設定により、リスクを管理したトレンド追跡が可能

- ボラティリティ指標を採用し、高ボラティリティ環境での取引を確保

- マルチタイムフレーム分析により、戦略の安定性を向上

リスク

- ブームハンター指標が圧縮により歪み、誤ったシグナルを発生させる可能性がある

- ハルスイートの中央線はラグが生じ、価格変動にタイムリーに追従できない

- ボラティリティが低下すると取引機会を逃したり、損失ポジションの手仕舞いを引き起こす可能性がある

解決方法:

- 圧縮指標のパラメータを調整し、指標の感度のバランスを取る

- EHMAなどの指数移動平均線を中央線の代わりに使用してみる

- 他の判断指標を追加し、ボラティリティによる誤ったシグナルを回避する

最適化

本戦略は以下の観点から最適化が可能です。

-

パラメータ最適化: 期間の長さや圧縮係数などの指標パラメータを変更し、最適なパラメータ組み合わせを追求する

-

タイムフレーム最適化: 異なる時間足(1分、5分、30分など)をテストし、最も適した取引時間足を見つける

-

ポジション最適化: 取引ごとのポジションサイズと比率を変更し、最適な資金活用方法を見つける

-

ストップロス最適化: 取引ペアごとにストップロス位置を調整し、最適なリスクリワード比を実現する

-

条件最適化: 指標のフィルタリング条件を増減し、より正確なエントリータイミングを得る

まとめ

本戦略は、ブームハンター、ハルスイート、ボラティリティオシレーターの3つの指標を組み合わせて運用することで、マルチタイムフレームでのトレンド追跡取引を実現し、価格の突発的な動きを効果的に識別することができ、高いボラティリティを持つデジタルアセットに適しています。本戦略はリスクが管理可能であり、パラメータ、フィルター条件、ストップロスなどの多面的な最適化により、実戦性と拡張性に優れています。

- 1