双方向トレーリングストップ移動平均トレンド戦略

概要

本戦略は、スーパートレンド、SSLハイブリッドベースラインチャネル、QQEモメンタム指標を組み合わせ、双方向のポジションに対してトレーリングストップを適用し、中長期トレンドを捉えることを目的とします。

戦略の原理

本戦略は主に以下の要点に基づいています:

- スーパートレンド指標を使用して全体的なトレンド方向を判断し、エントリーのタイミングを補助します。

- SSLハイブリッドベースラインチャネルに基づき具体的なエントリーポイントを判断します。チャネルブレイクアウトを基本的なエントリーシグナルとします。

- QQE指標のロング・ショートクロスをエントリーの副確認シグナルとして利用します。

- ATR指標を使用してストップロスとテイクプロフィットの水準を計算します。

- パーセンテージリスク管理と動的ストップロス調整戦略を採用し、一取引あたりのリスクを制御します。

エントリーロジックは、スーパートレンドが転換し、価格がベースラインチャネルをブレイクし、さらにQQE指標が対応方向にクロスした場合のみエントリーします。

この組み合わせ指標システムにより、エントリータイミングを効果的に制御し、レンジ相場での無駄なエントリーを回避できます。

決済ロジックは比較的シンプルで、スーパートレンドの転換、またはストップロス・テイクプロフィットのトリガーをもってポジションをクローズします。

優位性分析

本戦略の最大の利点は、複数の指標を組み合わせることで、偽のブレイクアウトを効果的にフィルタリングし、無効な取引の発生確率を低減できることです。

また、パーセンテージストップロスを採用して一取引あたりの損失リスクをコントロールする点が、本戦略の大きな特長です。

ATRでストップロス水準を計算し、設定可能なストップロス倍率を組み合わせることで、各取引のリスクを明確に把握できます。これはリスク管理において極めて重要です。

さらに、最大許容損失率を設定することで、全体の損失を制限することも可能です。

本戦略ではトレーリングストップを使用して利益を確定する点も、収益を強化する重要な要素です。

リスク分析

本戦略の最大のリスクは、複合シグナルが誤ったシグナルを発する可能性があることです。複数の指標によるフィルタリングを採用していますが、どの指標も完全に誤りを避けることはできません。

スーパートレンドで偽のブレイクアウトが発生した場合や、QQEで誤ったシグナルが形成された場合、本戦略は容易にエントリーしてしまい、ストップロスがトリガーされるリスクが高まります。

また、この戦略はオーバーフィッティングのリスクにも直面します。パラメータ設定は慎重に行い、過去データへの過度な依存を避ける必要があります。

ATR期間、ストップロス倍率、パーセンテージリスクなど、重要なパラメータの設定に注意が必要です。これらのパラメータは銘柄ごとに個別に調整する必要があります。

最適化の方向性

本戦略にはさらなる改善の余地があります:

- KD指標など、より多くの指標を補助判断に加えるテストが可能です。

- 異なるパラメータ設定下での安定性を検証できます。

- 機械学習手法に基づくパラメータ自動最適化を試すことができます。

- 適応型ストップロス機構を導入し、市場のボラティリティに応じてストップロス幅を調整できます。

- ストップロス後に再度エントリーするロジックを追加し、機会損失を減らすことができます。

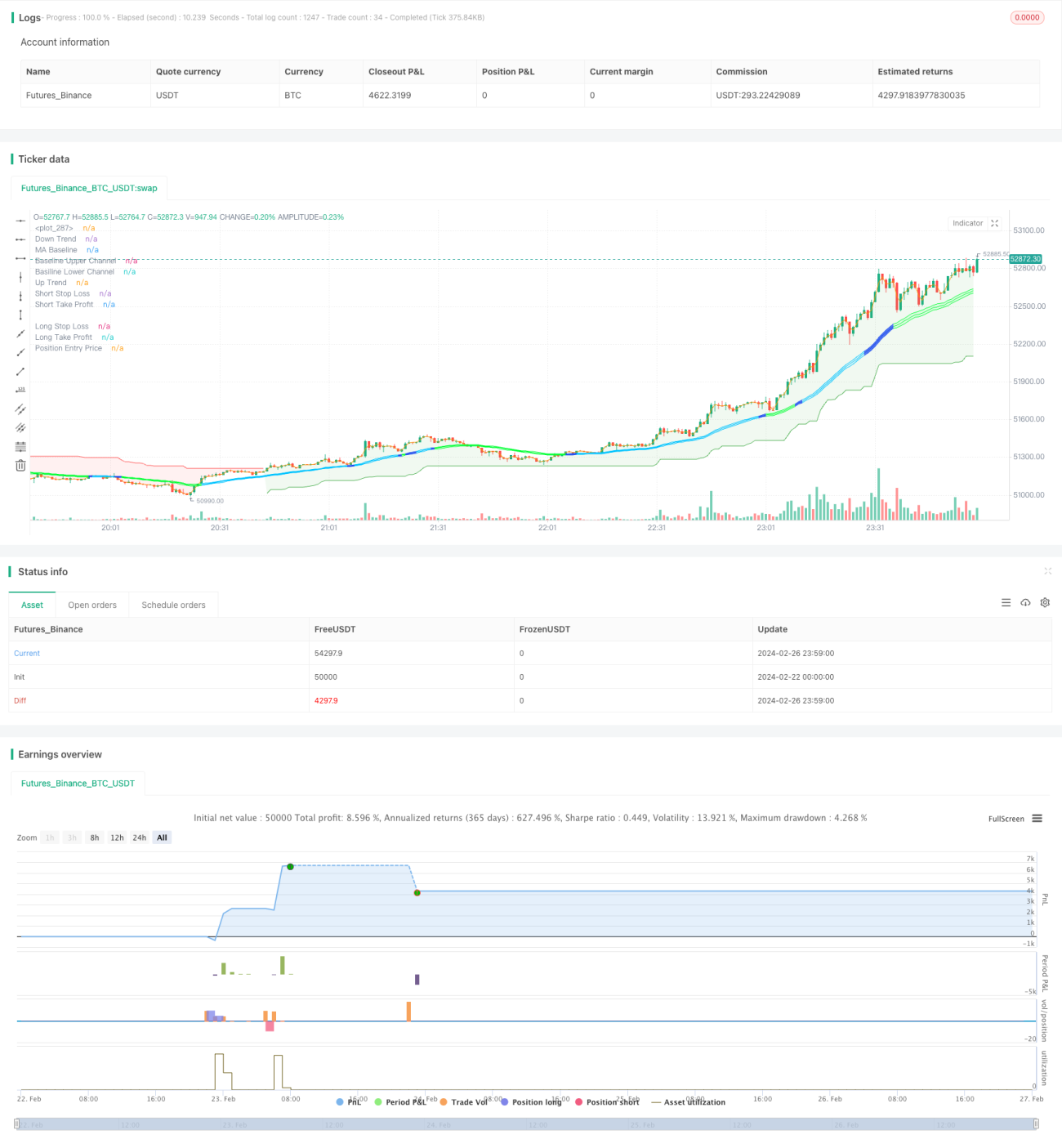

/*backtest

start: 2024-02-22 00:00:00

end: 2024-02-27 00:00:00

period: 1m

basePeriod: 1m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © fpemehd

// Thanks to W3MCT - @simonFUTURE2 w3mct.com -

// @version=5- 1