개요

급등급락 전략은 거액의 양선(양봉)과 음선(음봉)을 감지하여 진입하는 전략입니다. 거액의 양선이 감지되면 공매도를, 거액의 음선이 감지되면 매수를 실행합니다. 손절매는 신호를 발생시킨 캔들의 저점에 설정하며(매수의 경우 반대), 이익 실현은 손절매의 1배로 설정됩니다. 사용자는 양선과 음선의 최소 크기와 과거 특정 기간 평균 캔들 크기의 배수를 정의할 수 있습니다.

전략 원리

해당 전략의 핵심 로직은 다음과 같습니다.

-

현재 캔들의 총 변동 범위(고가-저가)와 실체 크기(종가가 시가보다 크면 양, 그 반대면 음)를 계산합니다.

-

과거 N개 캔들 내 변동 폭의 평균값을 계산합니다.

-

현재 캔들이 다음 조건을 충족하는지 판단합니다: 변동 범위 >= 평균 변동 폭 x 배수 AND 실체 크기 >= 변동 범위 x 최소 실체 계수

-

위 조건을 충족하면 신호가 발생합니다: 양선 -> 공매도, 음선 -> 매수

-

손절매 및 이익 실현 설정을 선택적으로 활성화할 수 있습니다. 손절매는 신호 캔들 저점에 손절매 계수 곱하기 변동 폭을 더한 값이며, 이익 실현은 손절매의 1배로 설정됩니다.

실체 판단 과정에서 선분을 필터링하여 충분한 힘이 있는지 확인합니다. 동적 평균 변동 폭을 계산함으로써 고정 임계값이 시장 변화에 적응하지 못하는 문제를 방지합니다. 손절매 및 이익 실현 설정은 합리적인 하락률을 보장하며 계수 조정이 가능합니다.

전략 장점

이 전략의 가장 큰 장점은 고품질의 추세 반전 신호를 포착한다는 점이며, 이는 두 가지 판단에 기반합니다.

-

거액의 양선과 음선은 해당 추세 초기에 이미 강하게 움직였음을 나타내므로, 전체 추세의 구조적 전환점일 가능성이 높습니다.

-

동적 평균 변동 폭을 계산하여 정상 수준을 초과하는 비정상적인 변동을 포착함으로써 일반적인 조정 흐름을 걸러냅니다.

또한 손절매 및 이익 실현 설정이 매우 합리적이며, 단일 손실을 효과적으로 제어할 수 있습니다. 동시에 이익 실현 수익률이 1이므로 과도한 추격 매수/매도를 피할 수 있습니다.

전반적으로 이 전략은 고품질의 구조적 전환점을 성공적으로 식별하여 효율적인 거래를 가능하게 합니다. 이는 추세 추종 트레이더에게 매우 적합하며, 중간 과정에서 갇히는 것을 방지할 수 있습니다.

전략 위험

이 전략의 주요 위험은 두 가지 측면에서 발생합니다.

-

급등급락이 손절매 촉발로 인해 발생하여 유효하지 않은 신호를 형성할 수 있습니다.

-

손절매 설정이 너무 느슨하여 손실을 효과적으로 제어하지 못할 수 있습니다.

첫 번째 위험은 최소 변동 폭과 실체 크기를 증가시켜 오판률을 걸러낼 수 있지만, 일부 기회를 놓칠 수도 있습니다. 백테스트 결과를 바탕으로 균형점을 찾아야 합니다.

두 번째 위험은 손절매 계수를 조정하여 손절매를 지지선에 더 가깝게 설정함으로써 최적화할 수 있지만, 너무 좁게 설정해서는 안 됩니다. 또한 손실을 보상하기 위해 이익 실현 수익률을 높이는 것도 고려해야 합니다.

전략 최적화 방향

이 전략은 다음과 같은 추가 최적화가 가능합니다.

-

추세 방향 판단을 추가하여 역추세 거래를 피합니다.

-

매개변수 설정을 최적화하여 최적의 매개변수 조합을 찾습니다.

-

거래량 필터를 추가하여 큰 양선과 음선의 거래량이 충분히 높은지 확인합니다.

-

플랫폼, 볼린저 밴드 등과 같은 추가 필터 조건을 도입하여 오판 확률을 줄입니다.

-

다양한 종목의 매개변수 효과를 테스트하고 매개변수 최적화를 수행합니다.

-

손절매 추적을 추가하여 가격 움직임에 따라 손절매를 동적으로 조정합니다.

-

재진입 기회를 추가하여 최초 손절매 후 다시 진입할 수 있도록 합니다.

위와 같은 최적화를 통해 이 전략의 효율성을 높여 실제 수익 확률을 개선할 수 있습니다. 충분한 백테스트와 최적화를 통해 최적의 매개변수를 찾아야 합니다.

요약

급등급락 전략은 거액의 양선과 음선을 포착하여 효율적인 수익을 실현하며, 손절매 및 이익 실현 설정을 갖추고 있습니다. 이 전략은 고품질의 구조적 반전 기회를 성공적으로 식별하여 추세 트레이더에게 매우 유용한 정보를 제공할 수 있습니다. 매개변수 최적화 및 규칙 최적화를 통해 이 전략은 매우 실용적인 보조 의사 결정 도구가 될 수 있습니다. 단순한 거래 논리와 직관적인 경제적 의미 덕분에 이해하고 활용하기 쉽습니다. 전반적으로 이 전략은 훌륭한 전략 프레임워크를 제공하며, 심층 연구 및 적용 가치가 있습니다.

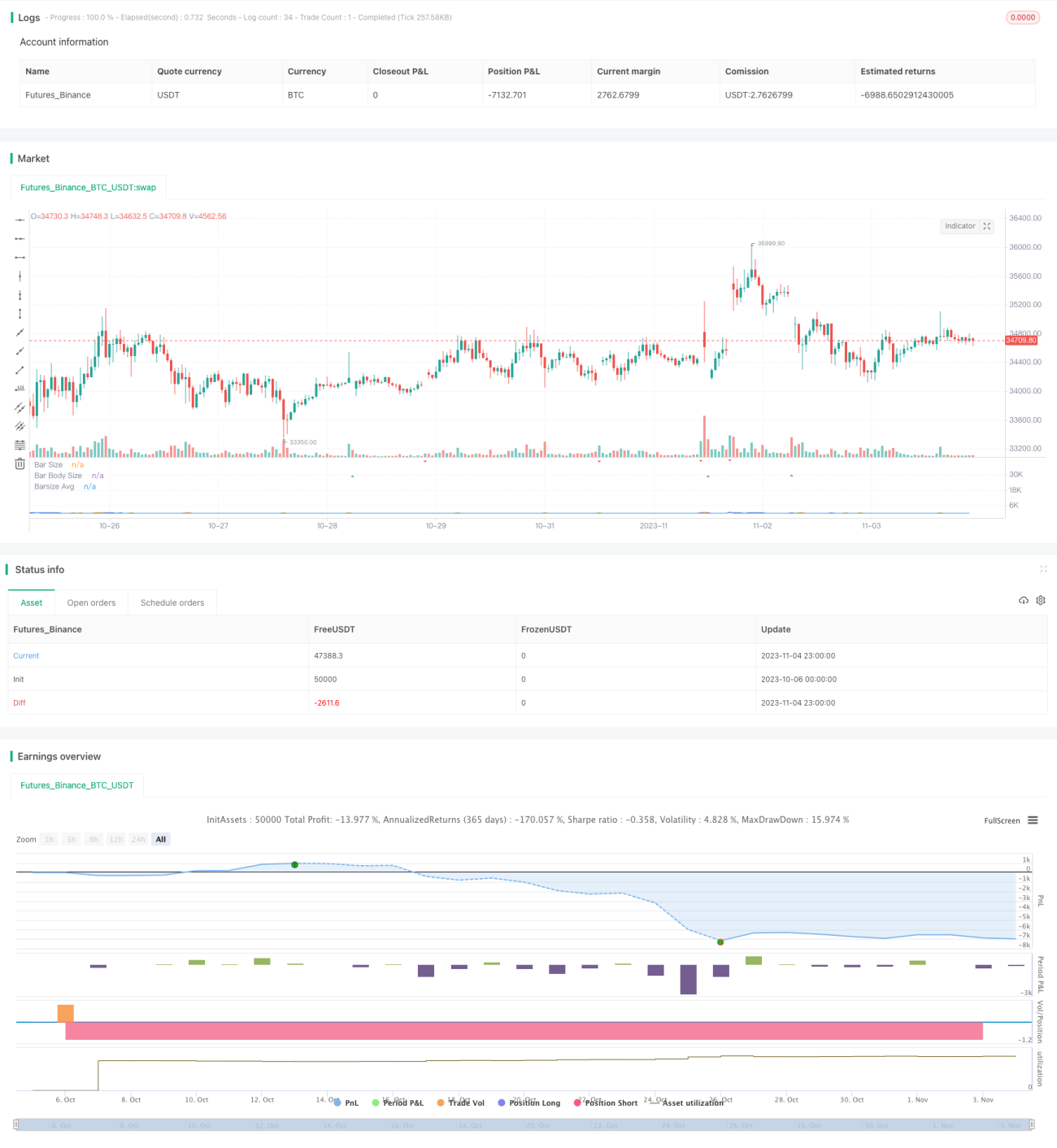

/*backtest

start: 2023-10-06 00:00:00

end: 2023-11-05 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This source code is subject to the terms of the Mozilla Public License 2.0 at https://mozilla.org/MPL/2.0/

// © tweakerID

// This strategy detects and uses big bars to enter a position. When the Big Bar - 1