개요

본 전략은 역전 전략과 볼린저 밴드 강세 전략을 결합하여 복합 거래 신호를 생성, 추세 추종과 역전 포착의 이중 기능을 구현합니다.

전략 원리

역전 부분

추천의 《나는 어떻게 선물 시장에서 3배 수익을 냈는가》 183페이지의 역전 전략 로직에 따라: 종가가 전일 종가보다 2일 연속 상승하고, 9일 스토캐스틱 지표의 슬로우 라인이 50 미만일 때 매수; 종가가 전일 종가보다 2일 연속 하락하고, 9일 스토캐스틱 지표의 패스트 라인이 50 초과일 때 매도합니다.

강세 부분

알렉산더 엘더 박사의 볼린저 밴드 강세 지표 활용: 13일 지수이동평균선으로 시장 가치 합의를 나타내며, 매수 강세 지표는 구매자가 가격을 가치 합의 이상으로 끌어올리는 능력을, 매도 강세 지표는 판매자가 가격을 가치 합의 이하로 끌어내리는 능력을 반영합니다. 매수 강세 지표는 당일 최고가에서 13일 지수이동평균선을 뺀 값, 매도 강세 지표는 당일 최저가에서 13일 지수이동평균선을 뺀 값으로 계산됩니다.

본 전략은 강세 지표의 임계값을 0으로 설정, 즉 강세 지표가 0보다 크면 거래 신호를 발생시킵니다.

복합 신호

역전 전략과 강세 전략의 거래 신호가 일치할 때 최종 거래 신호가 생성됩니다. 매수 신호는 역전 신호 매수와 강세 신호 매수의 복합, 매도 신호는 역전 신호 매도와 강세 신호 매도의 복합입니다.

장점 분석

본 전략은 종합형 전략으로, 역전 전략과 추세 추종 전략을 동시에 사용하여 거래 신호를 형성, 반등 포착과 추세 추종의 이점을 모두 갖습니다.

역전 부분은 갭 발생 후 역전 기회를 포착할 수 있습니다. 강세 부분은 추세가 존재할 때만 포지션을 열 수 있도록 보장합니다. 둘을 결합하면 가짜 돌파를 효과적으로 필터링하고 물리는 것을 방지할 수 있습니다.

매개변수 최적화의 유연성이 크며, 다양한 종목과 주기에 맞춰 조정하여 최적의 매개변수 조합을 찾을 수 있습니다.

리스크 분석

역전 전략과 강세 전략이 동시에 매수 또는 매도 신호를 낼 확률이 낮아 신호 발생 빈도가 높지 않을 수 있으며, 어느 정도 신호 희소성 리스크가 존재합니다.

역전 부분은 장 중 조정을 역전 기회로 오인하여 조기 진입할 수 있습니다. 강세 부분은 일부 역전 기회를 놓칠 수 있습니다. 두 전략을 결합하면 이러한 리스크를 어느 정도 완화할 수 있습니다. 추후 추세 판단 모듈을 도입하여 추가 최적화를 고려할 수 있습니다.

최적화 방향

- 다양한 매개변수 조합을 시도하여 최적의 매개변수 탐색

- 추세 판단 모듈 추가, 명확한 추세 없이 반복적인 포지션 구축 방지

- 손절매 전략 도입 고려, 개별 손실 통제

요약

본 전략은 추세 추종과 역전 거래의 특성을 모두 포함하여 종합형 전략 중에서도 뛰어난 성능을 자랑합니다. 매개변수 최적화를 통해 안정적인 수익을 기대할 수 있습니다. 동시에 신호 희소성과 오판 리스크에 주의해야 하며, 추후 추세 판단 및 손절매 모듈 도입 등을 통해 최적화하여 실전 성능을 더욱 향상시킬 수 있습니다.

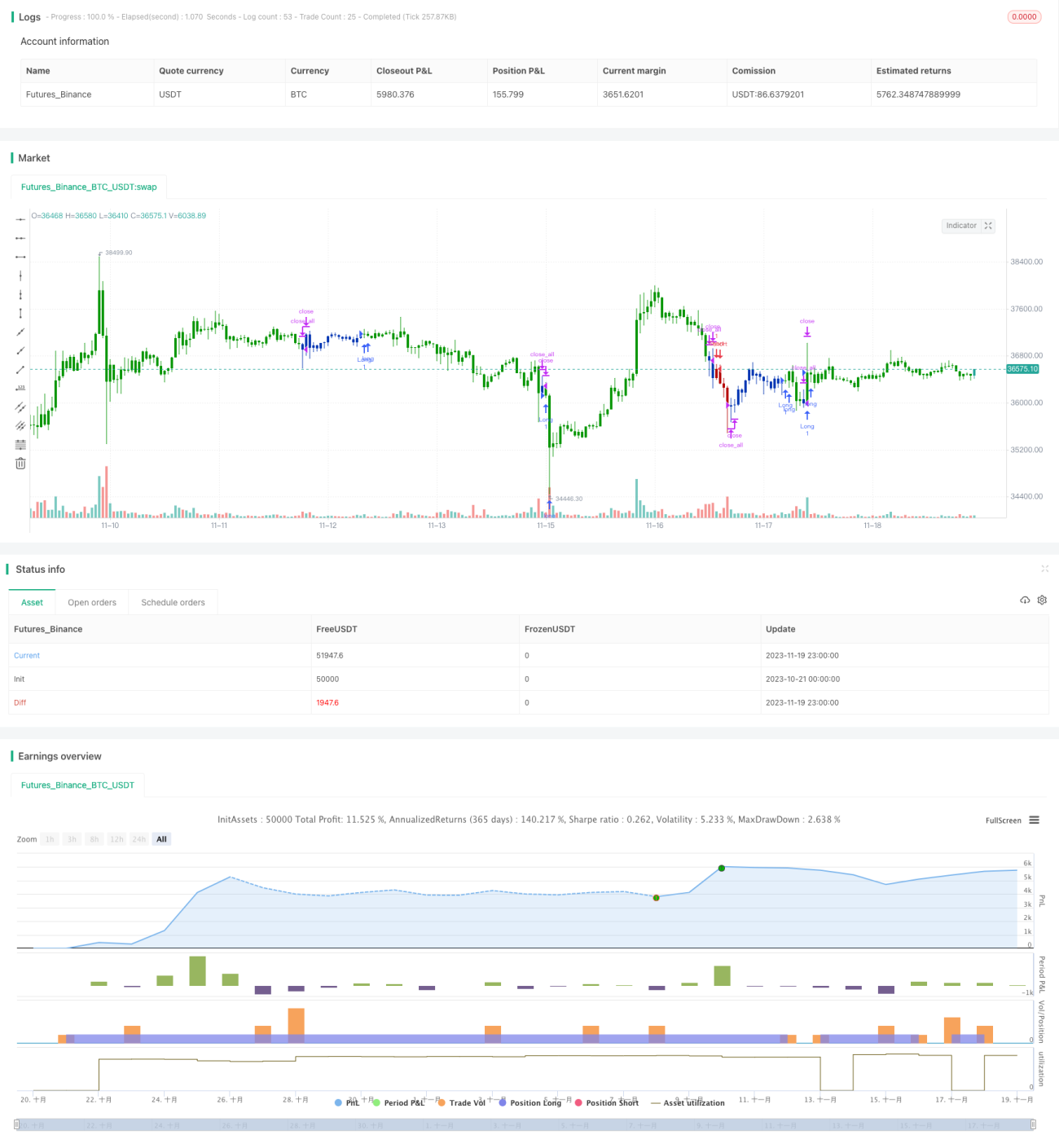

/*backtest

start: 2023-10-21 00:00:00

end: 2023-11-20 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 15/06/2020

// This is combo strategies for get a cumulative signal. - 1