1

Follow

1802

Followers

개요

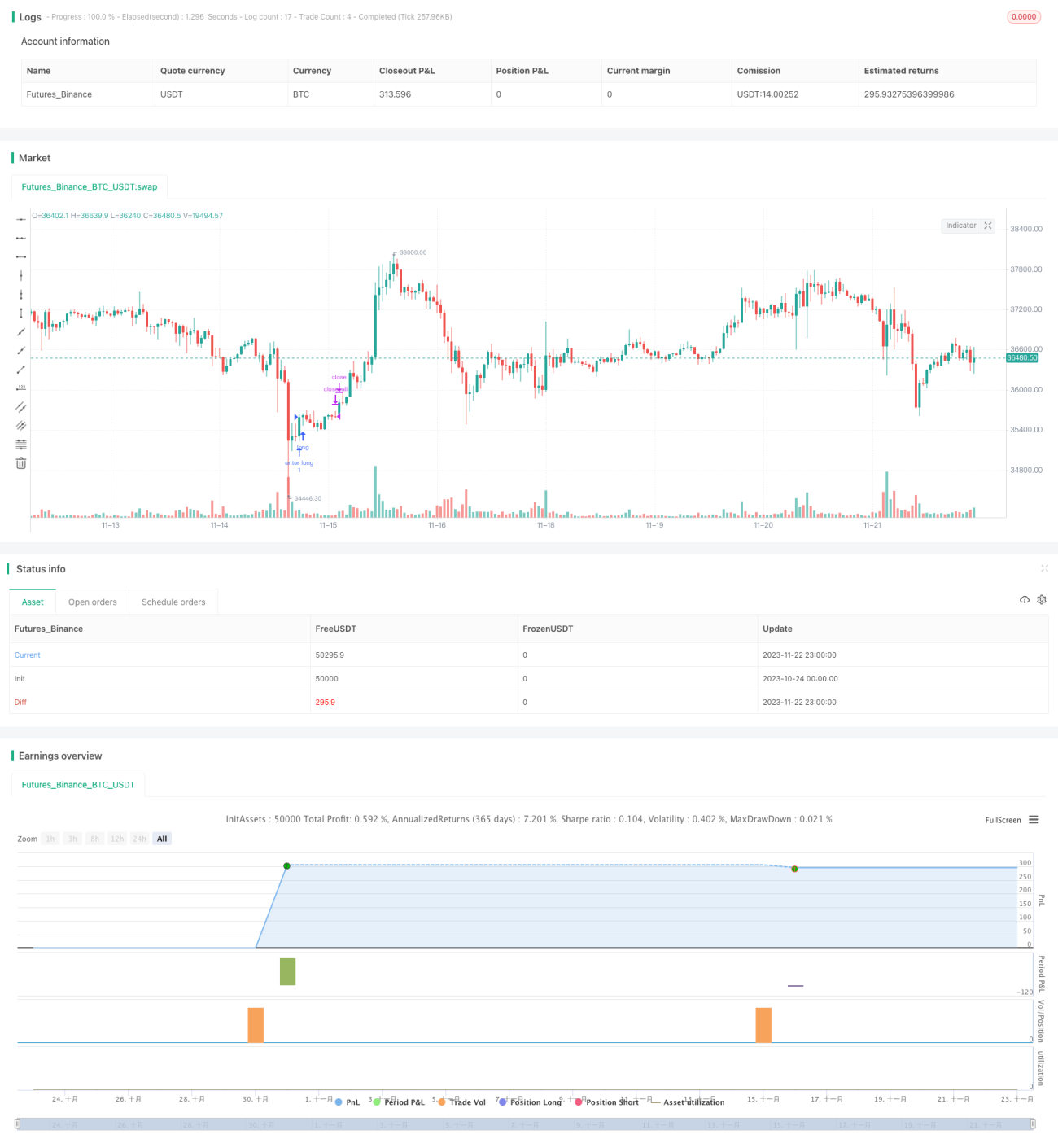

역전 캐치 전략은 변동성 지표인 볼린저 밴드와 모멘텀 지표인 RSI를 결합한 역전 거래 전략입니다. 볼린저 밴드 채널과 RSI의 과매수/과매도선을 신호로 설정하여 추세 방향이 전환될 때 역전 기회를 찾아 거래합니다.

전략 원리

해당 전략은 볼린저 밴드를 주요 기술 지표로 사용하고, RSI와 같은 모멘텀 지표를 통해 거래 신호를 검증합니다. 구체적인 로직은 다음과 같습니다.

- 큰 주기의 추세 방향을 판단하여 상승 추세인지 하락 추세인지 결정합니다. 50일 EMA와 21일 EMA의 골든 크로스/데드 크로스를 사용하여 판단합니다.

- 하락 추세에서 가격이 볼린저 하단 밴드를 돌파하여 상승하고, 동시에 RSI 지표가 과매도 영역에서 막 반등하여 골든 크로스 패턴이 나타나면, 과매도 영역에서 바닥이 형성된 것으로 판단하여 매수 신호로 간주합니다.

- 상승 추세에서 가격이 볼린저 상단 밴드를 돌파하여 하락하고, 동시에 RSI 지표가 과매수 영역에서 막 하락하여 데드 크로스 패턴이 나타나면, 과매수 영역에서 조정이 시작된 것으로 판단하여 매도 신호로 간주합니다.

- 위의 매수 및 매도 신호는 반드시 동시에 충족되어야 하며, 가짜 신호를 방지합니다.

장점 분석

해당 전략은 다음과 같은 장점이 있습니다.

- 변동성 지표와 모멘텀 지표를 결합하여 신호의 신뢰도가 비교적 높습니다.

- 역전 거래는 리스크가 상대적으로 적어 단기 거래에 적합합니다.

- 프로그램화된 규칙이 명확하여 자동 거래를 구현하기 쉽습니다.

- 추세 거래와 결합하여 변동성 장에서 무분별한 진입을 방지합니다.

리스크 분석

해당 전략에는 다음과 같은 리스크도 존재합니다.

- 볼린저 밴드 채널의 가짜 신호 돌파 리스크가 있으며, RSI 지표로 필터링해야 합니다.

- 역전 실패 리스크가 있으므로 적시에 손절매해야 합니다.

- 역전 시점을 정확히 포착하지 못할 리스크가 있어 조기 진입 또는 최적 지점을 놓칠 수 있습니다.

위 리스크에 대해 손절매 위치를 설정하여 리스크 노출을 통제하고, 매개변수를 최적화하여 볼린저 밴드 주기나 RSI 매개변수를 조정할 수 있습니다.

최적화 방향

해당 전략은 주로 다음과 같은 방향으로 최적화할 수 있습니다.

- 볼린저 밴드 매개변수 최적화: 주기 길이와 표준편차 크기를 조정하여 최적의 매개변수 조합을 찾습니다.

- 이동평균선 주기 최적화: 추세 판단을 위한 최적의 주기 길이를 결정합니다.

- RSI 매개변수 조정: 최적의 과매수/과매도 영역 범위를 찾습니다.

- KDJ, MACD 등 다른 지표를 추가하여 시스템 진입 이유를 풍부하게 합니다.

- 머신러닝 알고리즘을 추가하여 AI 기술을 활용해 최적의 매개변수를 자동으로 찾습니다.

요약

역전 캐치 전략은 전반적으로 효과가 좋은 단기 거래 전략입니다. 추세 판단과 역전 신호를 결합하여 변동성 장의 가짜 신호를 필터링하고 추세 장에서 추세와의 대립을 피하며 리스크를 통제할 수 있습니다. 매개변수와 모델을 지속적으로 최적화하면 더 나은 전략 성과를 얻을 수 있습니다.

Source

Pine

/*backtest

start: 2023-10-24 00:00:00

end: 2023-11-23 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// This is an Open source work. Please do acknowledge in case you want to reuse whole or part of this code.

// Please see the documentation to know the details about this.

//@version=5Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1