볼린저 밴드와 RSI 조합 전략

개요

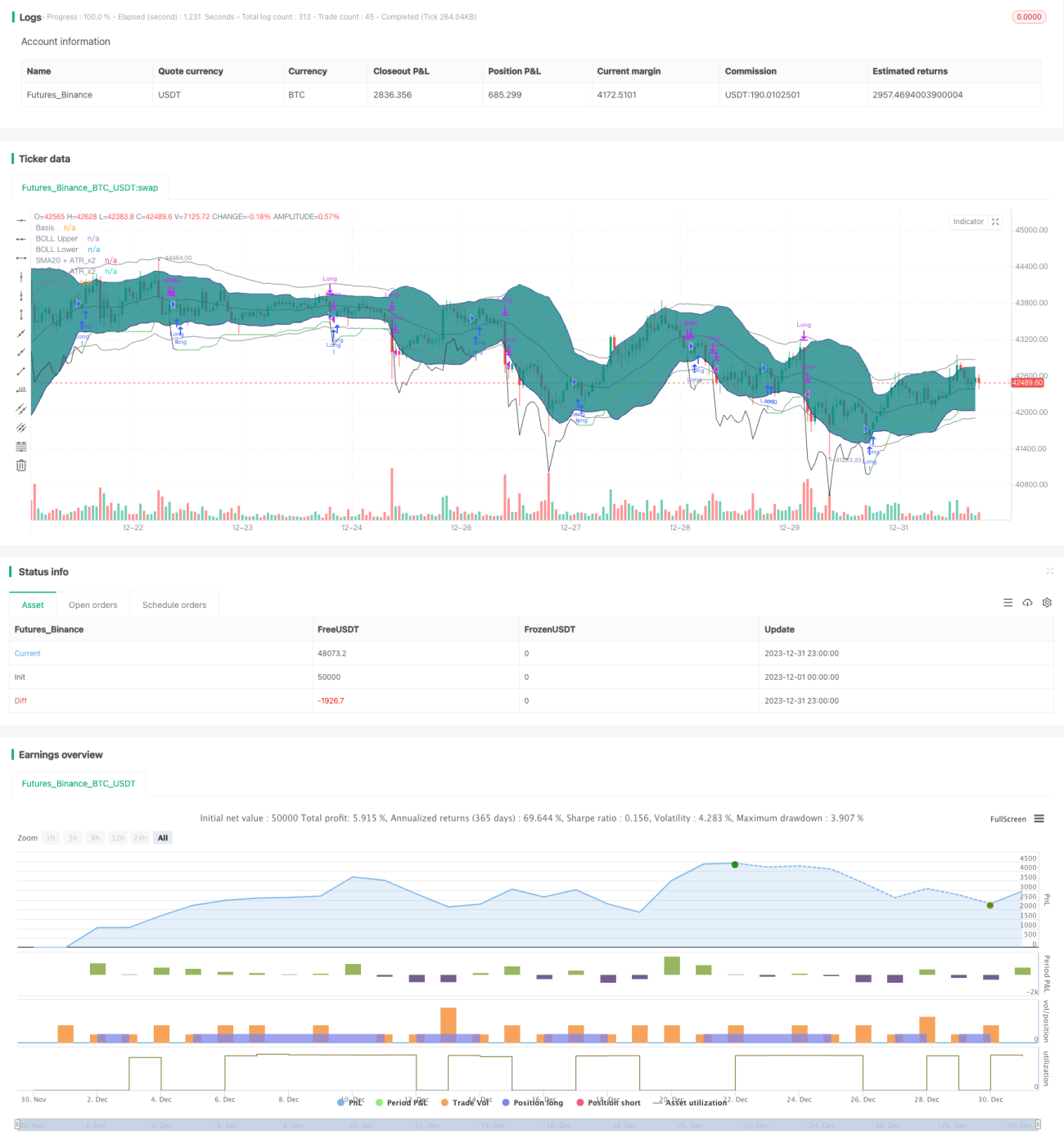

본 전략은 볼린저 밴드와 상대강도지수(RSI)를 조합하여 사용하며, 볼린저 밴드 수축 구간과 RSI 상승 기회를 식별하고, 추세 추종 손절매를 적용하여 위험을 관리합니다.

전략 원리

이 전략의 거래 논리 핵심은 볼린저 밴드의 수축을 식별하고, RSI가 상승세일 때 추세가 상승 초기 단계에 있음을 판단하는 데 있습니다. 구체적으로, 20일 볼린저 밴드 중앙선 위의 표준편차가 ATR*2보다 작을 때 볼린저 밴드가 수축했다고 판단합니다. 동시에 10일 및 14일 RSI가 모두 상승 추세라면, 가격이 곧 볼린저 밴드 상단을 돌파할 것으로 예측하여 매수 전략을 취합니다.

포지션 진입 후에는 ATR 안전 거리와 가격 상승에 따른 손절매 방식을 사용하여 이익을 확보하고 위험을 통제합니다. 가격이 손절매 라인을 초과하거나 RSI가 과열(14일 RSI가 70을 초과하고, 10일 RSI가 14일 RSI를 초과)되면 청산합니다.

장점 분석

본 전략의 가장 큰 장점은 볼린저 밴드 수축을 활용하여 시장의 횡보 국면을 판단하고, RSI 지표를 결합하여 가격 돌파 방향을 예측하는 데 있습니다. 또한 고정 손절매 대신 적응형 손절매를 사용하여 시장 변동성에 따라 유연하게 조정함으로써 위험 통제가 가능한 범위 내에서 더 큰 수익을 얻을 수 있습니다.

위험 분석

본 전략의 주요 위험은 볼린저 밴드 수축과 RSI 상승을 식별할 때 허위 돌파(가짜 돌파)가 발생할 가능성에 있습니다. 또한 손절매 측면에서 변동성이 너무 클 경우 적응형 손절매가 적시에 손절하지 못할 수 있습니다. 손절매 방식을 개선(예: 곡선 손절매)하여 이 위험을 줄일 수 있습니다.

최적화 방향

본 전략은 다음과 같은 측면에서 최적화할 수 있습니다.

-

볼린저 밴드 매개변수 설정을 개선하여 수축 판단 효과 최적화

-

다양한 RSI 주기 매개변수 시도

-

다른 손절매 방식(곡선 손절매, 후행 손절매 등)의 효과 테스트

-

각 종목 특성에 따라 매개변수 조정

요약

본 전략은 볼린저 밴드와 RSI의 상호 보완성을 종합적으로 활용하여 위험을 통제하는 가운데 우수한 하락률 대비 수익 비율을 얻습니다. 향후 손절매 방식, 매개변수 선택 등을 최적화하여 전략이 다양한 거래 종목에 더 적합하도록 할 수 있습니다.

- 1