동적 포지션 추가 전략에 기반한

개요

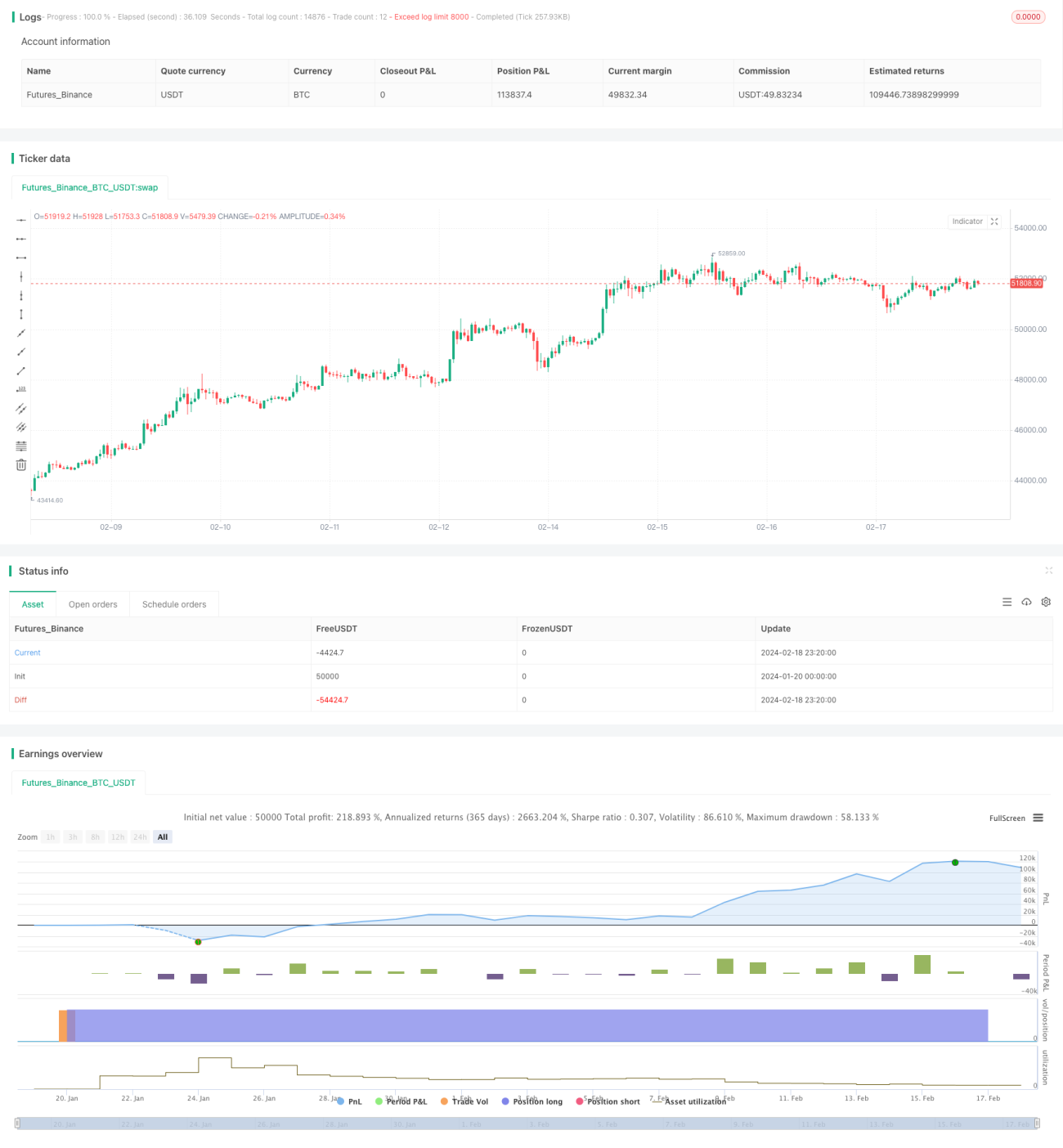

이 전략의 주요 아이디어는 시스템 신호에 따라 동적으로 포지션을 추가하며, 상승장에서 점진적으로 포지션을 구축하여 리스크를 통제하고 낮은 평균 진입가를 확보하는 것입니다.

전략 원리

해당 전략은 우선 초기 자본과 DCA 설정 비율을 정합니다. 각 캔들 종가에서 가격 변동에 따라 조정된 설정 비율을 계산합니다. 가격이 상승하면 비율을 낮추고, 가격이 하락하면 비율을 높입니다. 이를 통해 가격이 낮을 때 포지션을 늘릴 수 있습니다. 그런 다음 조정된 비율과 남은 자금을 바탕으로 주문 규모를 산출합니다. 각 캔들 종가에서 초기 자본이 소진될 때까지 포지션을 추가하는 주문을 실행합니다.

이를 통해 시장 변동성이 있을 때 리스크를 통제하고 낮은 평균 진입가를 얻을 수 있습니다. 또한 평균 진입가와 중간 가격을 통계로 제공하여 현재 진입 상황을 직관적으로 판단할 수 있습니다.

장점 분석

해당 전략은 다음과 같은 장점을 가집니다:

-

동적으로 포지션을 추가하여 시세 하락 시 포지션을 늘리고 상승 시 포지션을 줄여 리스크를 통제할 수 있습니다.

-

중간 가격보다 낮은 평균 진입가를 확보하여 더 높은 수익 공간을 얻는 데 유리합니다.

-

상승장에서 변동성이 있는 시장에 적합하며, 좋은 위험-수익 비율을 얻을 수 있습니다.

-

초기 자본과 DCA 비율을 미리 설정하여 매번 포지션 추가 자금 규모를 통제하고 과도한 리스크를 방지할 수 있습니다.

-

평균 진입가와 중간 가격 통계를 제공하여 진입의优劣를 직관적으로 판단할 수 있습니다.

위험 분석

해당 전략은 다음과 같은 위험도 존재합니다:

-

시장이 급락할 경우 지속적으로 포지션을 추가하게 되어 상당한 자금 손실이 발생할 수 있습니다. 손절매를 설정하여 리스크를 통제할 수 있습니다.

-

시장이 급등할 경우 포지션 추가 폭이 줄어들어 대부분의 상승 기회를 놓칠 수 있습니다. 이때 다른 신호를 활용하여 민첩하게 대응해야 합니다.

-

매개변수 설정이 부적절할 경우 리스크가 커질 수 있습니다. 초기 자본이 과도하거나 DCA 비율이 너무 높으면 손실이 확대됩니다.

최적화 방향

해당 전략은 다음과 같은 측면에서 최적화할 수 있습니다:

-

손절매 로직을 추가하여 큰 폭의 하락 시 포지션 추가를 중단할 수 있습니다.

-

변동성이나 다른 지표에 따라 DCA 비율을 동적으로 조정할 수 있습니다.

-

머신러닝 모델을 추가하여 가격 변동을 예측하고 포지션 추가 결정을 지원할 수 있습니다.

-

다른 기술 지표를 결합하여 시장 구조를 판단하고 구조 전환점에서 포지션 추가를 중단할 수 있습니다.

-

자금 관리 모듈을 추가하여 계좌 자금 상황에 따라 매번 포지션 추가 자금을 동적으로 조정할 수 있습니다.

요약

해당 전략은 매우 실용적인 동적 포지션 추가 전략입니다. 시장 변동에 따라 유연하게 포지션을 조정하며, 상승장에서 낮은 평균 진입가를 확보할 수 있습니다. 동시에 리스크 통제를 위한 매개변수 설정이 내장되어 있습니다. 다른 기술 지표나 모델과 결합하면 더 나은 효과를 얻을 수 있습니다. 이 전략은 장기 투자 수익을 추구하는 투자자에게 적합합니다.

- 1