Strategi Pengesanan Trend Golden Cross Dwi EMA

Gambaran Keseluruhan

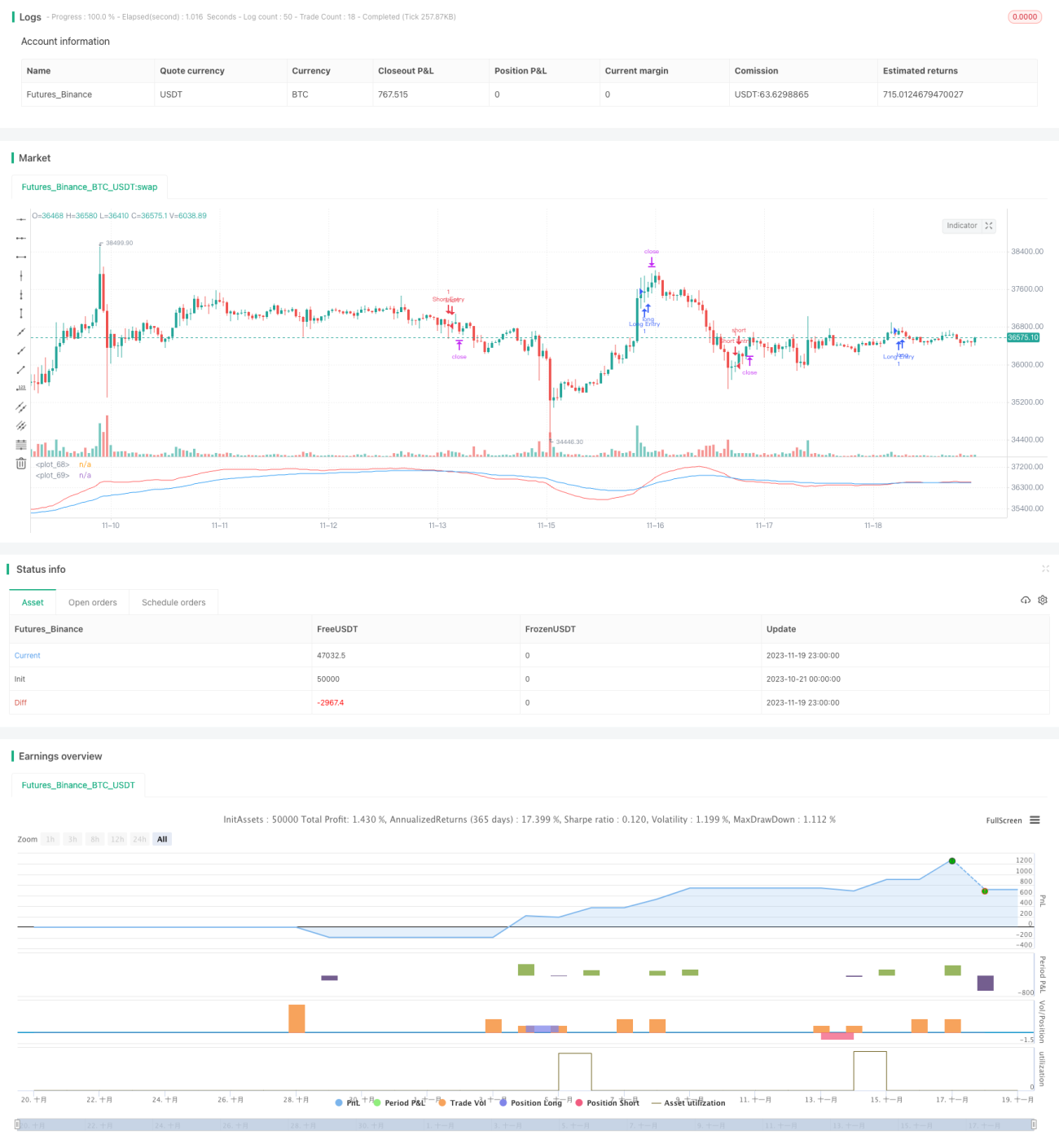

Strategi ini mengira EMA pantas dan EMA perlahan, dan membandingkan hubungan saiz antara kedua-dua EMA untuk menentukan arah aliran pasaran. Ia adalah strategi pengesanan arah aliran yang mudah. Apabila EMA pantas menembusi ke atas EMA perlahan, posisi beli dibuka; apabila EMA pantas menembusi ke bawah EMA perlahan, posisi jual dibuka. Ini adalah strategi persilangan emas EMA berganda yang tipikal.

Prinsip Strategi

Indikator teras strategi ini ialah EMA pantas dan EMA perlahan. Tempoh EMA pantas ditetapkan kepada 21 kitaran, manakala tempoh EMA perlahan ditetapkan kepada 55 kitaran. EMA pantas dapat bertindak balas dengan lebih cepat terhadap perubahan harga, mencerminkan arah aliran jangka pendek terkini; EMA perlahan bertindak balas lebih perlahan terhadap perubahan harga, dapat menapis sebahagian bunyi bising, dan mencerminkan arah aliran jangka sederhana hingga panjang.

Apabila EMA pantas menembusi ke atas EMA perlahan, ini menunjukkan arah aliran jangka pendek bertukar menaik, dan arah aliran jangka sederhana hingga panjang mungkin mengalami perubahan; ini adalah isyarat untuk membeli. Apabila EMA pantas menembusi ke bawah EMA perlahan, ini menunjukkan arah aliran jangka pendek bertukar menurun, dan arah aliran jangka sederhana hingga panjang mungkin mengalami perubahan; ini adalah isyarat untuk menjual.

Melalui perbandingan EMA pantas dan perlahan, titik perubahan arah aliran pada dua skala masa (jangka pendek dan jangka sederhana/panjang) dapat dikesan. Ini adalah strategi pengesanan arah aliran yang tipikal.

Kelebihan Strategi

- Konsep yang mudah dan jelas, mudah difahami dan dilaksanakan

- Fleksibel dalam pelarasan parameter, tempoh EMA pantas dan perlahan boleh disesuaikan

- Boleh dikonfigurasikan dengan stop loss dan take profit berdasarkan ATR untuk risiko terkawal

Risiko Strategi

- Pemilihan titik masa persilangan EMA berganda mungkin tidak tepat, terdapat risiko terlepas titik masuk yang optimum

- Apabila pasaran berayun, mungkin terdapat isyarat tidak sah yang kerap, menyebabkan risiko kerugian

- Tetapan parameter ATR yang tidak sesuai boleh menyebabkan stop loss dan take profit terlalu longgar atau terlalu agresif

Langkah-langkah mengatasi risiko:

- Mengoptimumkan parameter EMA pantas dan perlahan untuk mencari kombinasi parameter yang optimum

- Menambah mekanisme penapisan untuk mengelakkan isyarat tidak sah semasa pasaran berayun

- Menguji dan mengoptimumkan parameter ATR untuk memastikan tetapan stop loss dan take profit yang munasabah

Hala Tuju Pengoptimuman Strategi

- Menguji kestabilan parameter tempoh EMA yang berbeza berdasarkan kaedah statistik

- Menambah syarat penapisan dengan menggabungkan indikator lain untuk mengelakkan isyarat tidak sah

- Mengoptimumkan parameter ATR untuk mendapatkan nisbah stop loss dan take profit yang terbaik

Kesimpulan

Strategi ini menggunakan persilangan antara EMA pantas dan EMA perlahan untuk menentukan arah aliran pasaran. Ia ringkas dan jelas, mudah dilaksanakan. Pada masa yang sama, ia menggabungkan ATR untuk menetapkan stop loss dan take profit, membolehkan risiko terkawal. Dengan pengoptimuman parameter dan penambahan syarat penapisan, kestabilan dan keuntungan strategi dapat dipertingkatkan lagi.

- 1