Strategi Henti Rugi dan Ambil Untung Adaptif Berdasarkan Rangka Masa Dwi dan Penunjuk Momentum

Gambaran Keseluruhan

Strategi ini menggunakan gabungan dua jangka masa dan penunjuk momentum untuk mencapai ambang ambil untung dan henti rugi yang adaptif. Jangka masa utama memantau arah aliran, manakala jangka masa bantu digunakan untuk mengesahkan isyarat. Apabila kedua-dua arah aliran sepadan, isyarat dagangan dijana. Selepas masuk pasaran, kaedah ambil untung progresif digunakan untuk mengemas kini tahap ambil untung dan henti rugi.

Prinsip Strategi

-

Jangka masa utama menggunakan penunjuk regresi linear Sqqueeze Momentum (SQM) untuk menilai arah aliran, manakala jangka masa bantu menggunakan gabungan EMA penunjuk SQM untuk menapis isyarat palsu.

-

Apabila SQM carta utama menembusi ke atas dan SQM carta bantu juga menaik, lakukan posisi beli; apabila SQM carta utama menembusi ke bawah dan SQM carta bantu juga menurun, lakukan posisi jual.

-

Selepas masuk pasaran, tetapkan tahap ambil untung dan henti rugi awal berdasarkan parameter input. Apabila harga mencapai tahap ambil untung, kemas kini tahap ambil untung dan henti rugi. Caranya ialah: tahap ambil untung meningkat mengikut nisbah yang ditetapkan, manakala tahap henti rugi menurun mengikut nisbah, mencapai ambil untung progresif.

Kelebihan Strategi

-

Dua jangka masa menapis isyarat palsu, memastikan ketepatan isyarat.

-

Penunjuk SQM menilai arah aliran, mengelakkan gangguan bunyi pasaran.

-

Mekanisme ambil untung dan henti rugi adaptif memaksimumkan penguncian keuntungan dan mengawal risiko dengan berkesan.

Analisis Risiko

-

Penetapan parameter penunjuk SQM yang tidak sesuai mungkin terlepas titik perubahan arah aliran, menyebabkan kerugian.

-

Pemilihan jangka masa carta bantu yang tidak sesuai mungkin gagal menapis bunyi dengan berkesan, menghasilkan dagangan yang salah.

-

Julat henti rugi yang terlalu besar boleh menyebabkan kerugian tunggal yang agak besar.

Arah Pengoptimuman

-

Parameter penunjuk SQM perlu diselaraskan mengikut pasaran yang berbeza untuk memastikan sensitivitinya.

-

Jangka masa carta bantu juga perlu diuji dengan kitaran yang berbeza untuk melihat kitaran mana yang memberikan penapisan terbaik.

-

Julat henti rugi boleh ditetapkan dengan julat turun naik dan bukannya nilai tetap, supaya boleh diselaraskan mengikut tahap turun naik pasaran.

Kesimpulan

Secara keseluruhannya, strategi ini sangat praktikal. Dua jangka masa digabungkan dengan penunjuk momentum untuk menilai arah aliran, dan menggunakan kaedah ambil untung dan henti rugi adaptif untuk mencapai keuntungan yang stabil. Dengan mengoptimumkan parameter penunjuk SQM, kitaran carta bantu dan penetapan julat henti rugi, strategi ini boleh menjadi lebih berkesan dan sesuai digunakan serta dioptimumkan dalam dagangan sebenar.

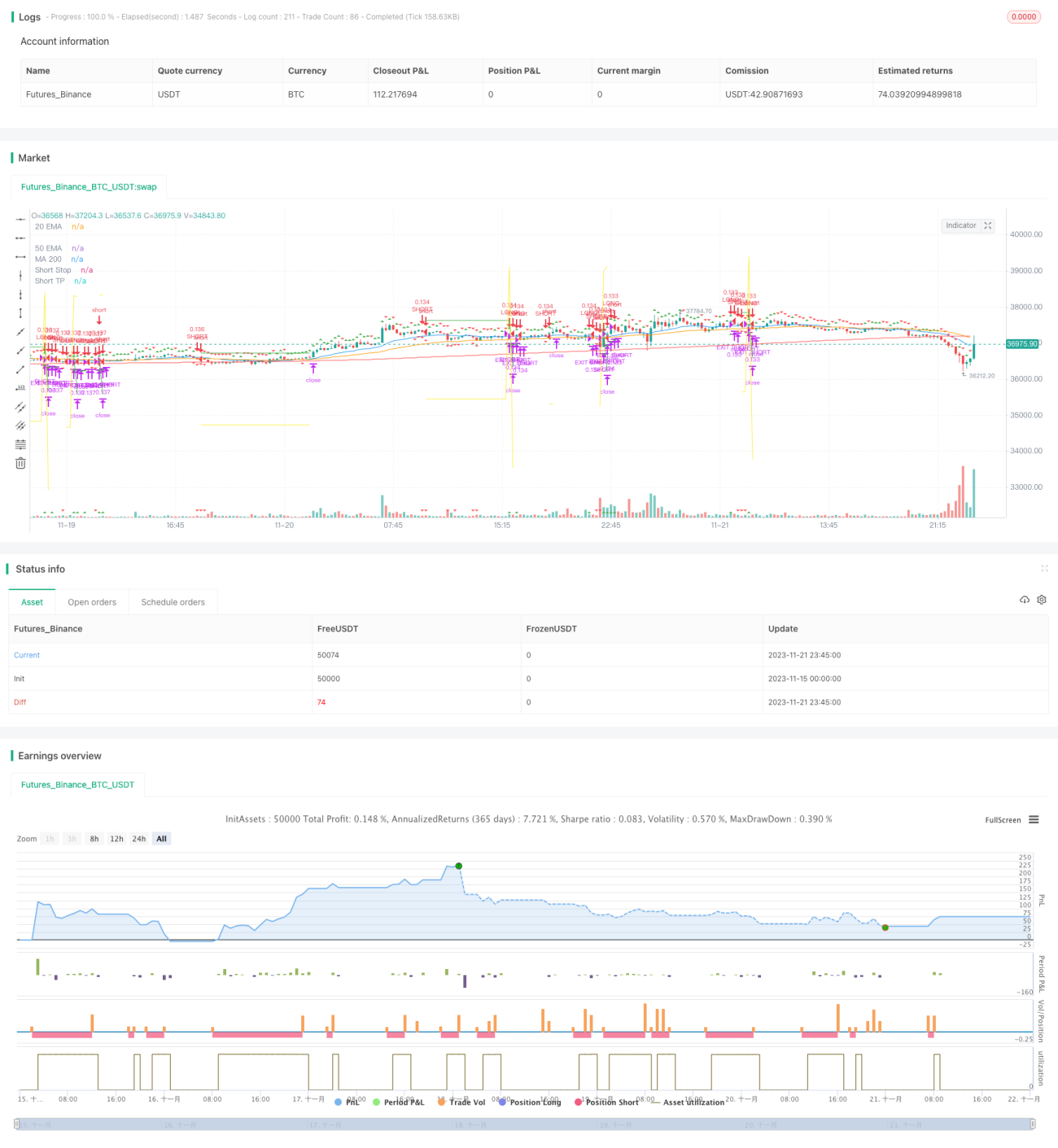

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1