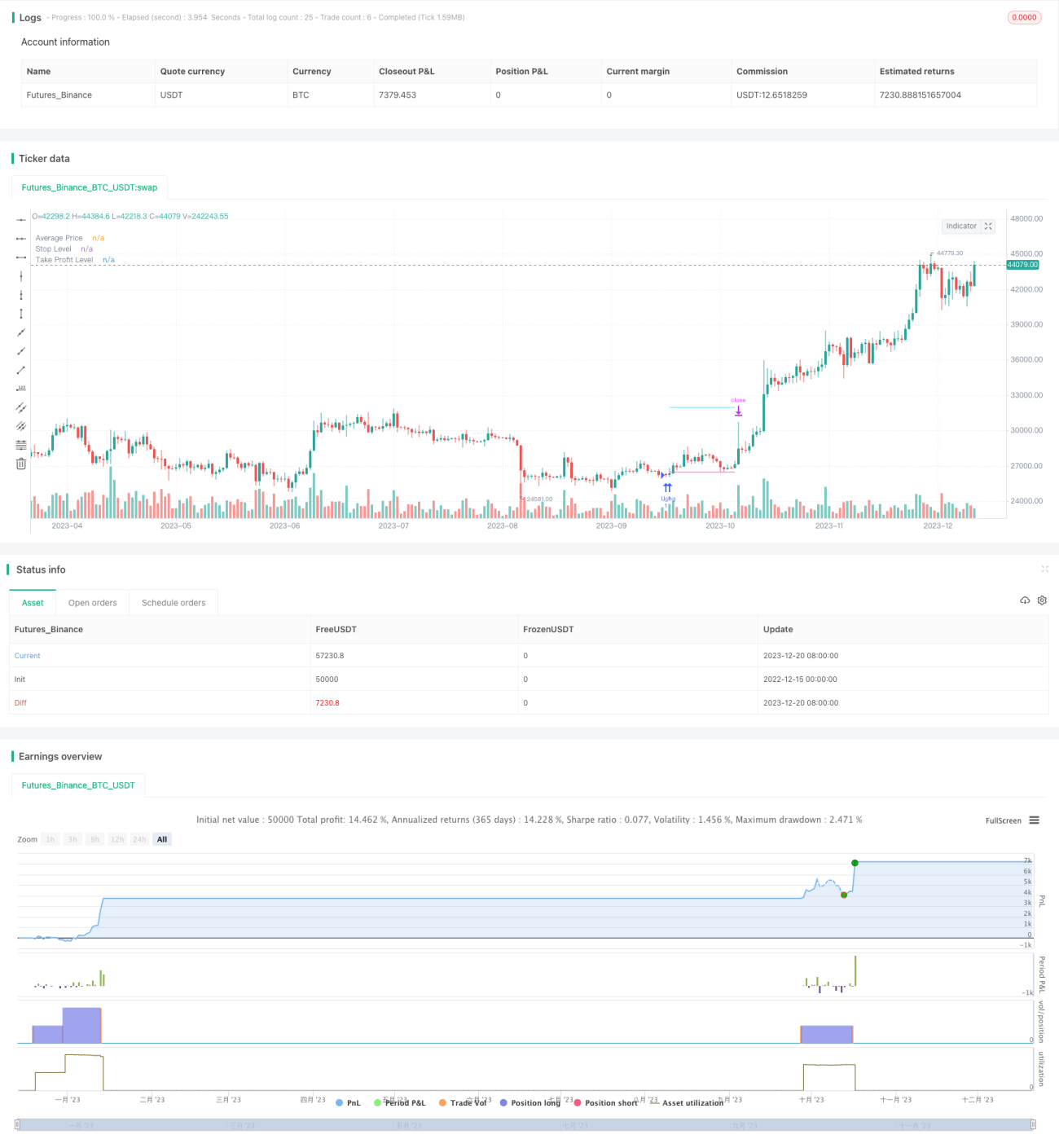

Strategi Penjejakan Risiko Rendah Piramid Titik Rendah

Strategi ini mengenal pasti potensi titik rendah dalam pergerakan harga dengan menggabungkan pelbagai penunjuk, dan mengurangkan risiko melalui pembinaan kedudukan secara piramid menjejak. Strategi ini juga menggabungkan fungsi seperti stop loss, take profit, dan trailing stop loss untuk mengawal risiko dengan berkesan.

Gambaran Keseluruhan Strategi

Strategi ini pertama sekali menggunakan perbezaan antara RSI dan EMA RSI untuk mengenal pasti potensi titik rendah harga. Untuk menapis isyarat palsu, strategi ini juga menggabungkan purata bergerak dan stokastik pelbagai jangka masa untuk pengesahan. Setelah isyarat titik rendah disahkan, kedudukan beli akan dibuka secara berperingkat sedikit di bawah titik tersebut, iaitu konsep piramid menjejak. Strategi ini membenarkan pembukaan sehingga 12 pesanan menjejak, dengan kuantiti setiap pesanan meningkat secara berurutan, yang dapat menyebarkan risiko dengan berkesan. Semua pesanan akan ditutup berdasarkan satu stop loss keseluruhan, dan juga membenarkan penetapan take profit secara individu untuk setiap pesanan. Untuk mengawal risiko selanjutnya, strategi ini juga menetapkan stop loss keseluruhan berdasarkan peratusan ekuiti akaun.

Prinsip Strategi

Strategi ini terdiri daripada tiga bahagian utama: modul pengenalan titik rendah, modul piramid menjejak, dan modul kawalan risiko.

Modul pengenalan titik rendah menggunakan perbezaan antara penunjuk RSI dan EMA RSI untuk mengenal pasti potensi titik rendah harga. Untuk meningkatkan ketepatan, purata bergerak dan penunjuk stokastik pelbagai jangka masa juga diperkenalkan untuk menapis isyarat. Isyarat titik rendah hanya akan disahkan apabila harga berada di bawah purata bergerak dan garis K stokastik berada di bawah 30.

Modul piramid menjejak adalah teras strategi ini. Setelah isyarat titik rendah disahkan, strategi akan membuka pesanan pertama pada harga 0.1% di bawah titik rendah tersebut. Selepas itu, selagi harga terus menurun dan berada di bawah harga masuk purata pada kadar tertentu, pesanan beli tambahan akan terus ditambah. Kuantiti pesanan baru akan meningkat secara berurutan, contohnya kuantiti pesanan ketiga adalah tiga kali ganda daripada pesanan pertama. Kaedah piramid menjejak ini dapat meratakan risiko. Strategi ini membenarkan sehingga 12 pesanan menjejak.

Modul kawalan risiko terutamanya merangkumi tiga aspek. Pertama, stop loss keseluruhan dikira berdasarkan harga tertinggi dalam tempoh tertentu baru-baru ini. Semua pesanan akan mengikuti stop loss ini dan ditutup serentak. Kedua, take poison bebas untuk setiap pesanan membenarkan take profit berdasarkan peratusan tertentu daripada harga masuk. Ketiga, stop loss keseluruhan berdasarkan peratusan ekuiti akaun, yang merupakan alat kawalan risiko paling kuat.

Kelebihan Strategi

- Mengurangkan risiko pesanan individu melalui piramid menjejak, sambil menyebarkan risiko keseluruhan

- Gabungan pelbagai penunjuk meningkatkan ketepatan pengenalan titik rendah

- Fungsi stop loss keseluruhan, take profit, dan trailing stop loss dapat mengawal risiko dengan berkesan

- Mekanisme stop loss berdasarkan peratusan ekuiti melindungi akaun daripada kerugian besar

- Keseimbangan antara risiko dan pulangan boleh dicapai dengan melaraskan parameter

Risiko Strategi

- Ketepatan pengenalan titik rendah masih terhad, mungkin terlepas titik masuk optimum atau memasuki isyarat palsu

- Keadaan pasaran yang tidak menguntungkan semasa menambah pesanan boleh memburukkan kerugian

- Memerlukan kitaran operasi yang lebih panjang untuk menunjukkan kelebihan strategi

- Tetapan parameter yang tidak sesuai boleh menyebabkan kawalan risiko yang tidak mencukupi

Untuk mengurangkan risiko di atas, pengoptimuman boleh dilakukan dari aspek berikut:

- Menukar atau menambah penunjuk untuk meningkatkan ketepatan pengenalan titik rendah

- Mengoptimumkan parameter seperti kuantiti pesanan, jarak, dan amplitud take profit untuk mengurangkan risiko setiap pesanan

- Memendekkan amplitud stop loss dengan sesuai untuk melindungi keuntungan

- Menguji pelbagai instrumen, memilih instrumen dengan kecairan yang baik dan turun naik yang tinggi

Hala Tuju Pengoptimuman Strategi

Strategi ini masih mempunyai ruang untuk pengoptimuman selanjutnya:

- Cuba perkenalkan teknologi yang lebih maju seperti pembelajaran mesin untuk mengenal pasti titik rendah

- Laraskan parameter seperti kuantiti pesanan dan amplitud stop loss secara dinamik berdasarkan keadaan pasaran

- Tambah strategi stop loss dalam julat untuk mengelakkan kerugian melebar

- Tambah mekanisme kemasukan semula

- Optimumkan parameter strategi untuk saham dan mata wang kripto

Kesimpulan

Strategi ini berkesan mengurangkan risiko setiap pesanan individu melalui konsep piramid menjejak, dan fungsi seperti stop loss keseluruhan, take profit, dan trailing stop loss juga memainkan peranan kawalan risiko yang baik. Walau bagaimanapun, masih ada ruang untuk pengoptimuman dalam pengenalan titik rendah. Jika teknologi yang lebih maju diperkenalkan, fungsi pelarasan parameter dinamik ditambah, dan digabungkan dengan pengoptimuman parameter, nisbah risiko-pulangan strategi ini akan meningkat dengan ketara.

- 1