Strategi Kuantitatif Penjejakan Trend Dwi

Ringkasan

Idea teras strategi ini adalah menggabungkan strategi pembalikan 123 dan penunjuk rainbow oscillator untuk mencapai penjejakan arah aliran berganda, bagi meningkatkan kadar kemenangan strategi. Strategi ini menjejak arah aliran harga jangka pendek dan sederhana, melaraskan kedudukan secara dinamik, untuk mencapai pulangan lebih tinggi berbanding pasaran.

Prinsip Strategi

Strategi ini terdiri daripada dua bahagian:

- Strategi pembalikan 123: Jika harga tutup dua hari sebelumnya menurun dan harga tutup hari ini meningkat, dan garis Slow K 9 hari di bawah 50, maka buka posisi panjang (long); jika harga tutup dua hari sebelumnya meningkat dan harga tutup hari ini menurun, dan garis Fast K 9 hari melebihi 50, maka buka posisi pendek (short).

- Penunjuk rainbow oscillator: Penunjuk ini mencerminkan tahap sisihan harga daripada purata bergerak. Apabila penunjuk melebihi 80, ia menunjukkan pasaran cenderung tidak stabil; apabila penunjuk di bawah 20, ia menunjukkan pasaran cenderung berbalik.

Strategi ini menggabungkan kedua-duanya, dan membuka posisi apabila isyarat beli dan jual muncul serentak, jika tidak ia menutup posisi.

Analisis Kelebihan

Strategi ini mempunyai kelebihan berikut:

- Penapis berganda, meningkatkan kualiti isyarat, mengurangkan kadar kesilapan.

- Pelarasan kedudukan secara dinamik, mengurangkan kerugian dalam pergerakan sehala.

- Mengintegrasikan penunjuk jangka pendek dan sederhana, meningkatkan kestabilan strategi.

Analisis Risiko

Strategi ini juga mempunyai risiko berikut:

- Pengoptimuman parameter yang tidak betul boleh menyebabkan overfitting.

- Pembukaan posisi berganda akan meningkatkan kos urus niaga.

- Apabila harga aset turun naik secara mendadak, titik henti rugi mudah ditembusi.

Risiko-risiko ini boleh dikurangkan dengan melaraskan parameter, mengoptimumkan pengurusan kedudukan, dan menetapkan henti rugi yang munasabah.

Arah Pengoptimuman

Strategi ini boleh dioptimumkan dari aspek berikut:

- Mengoptimumkan parameter untuk mencari kombinasi parameter terbaik.

- Menambah modul pengurusan kedudukan, melaraskan kedudukan secara dinamik berdasarkan volatiliti dan pengeluaran.

- Menambah modul henti rugi, menetapkan henti rugi bergerak yang munasabah.

- Menambah algoritma pembelajaran mesin untuk membantu menentukan titik perubahan arah aliran.

Kesimpulan

Strategi ini mengintegrasikan strategi pembalikan 123 dan penunjuk rainbow oscillator untuk mencapai penjejakan arah aliran berganda. Sambil mengekalkan kestabilan yang tinggi, ia mempunyai ruang pulangan lebih yang tertentu. Melalui pengoptimuman berterusan, ia dijangka dapat meningkatkan kadar pulangan strategi.

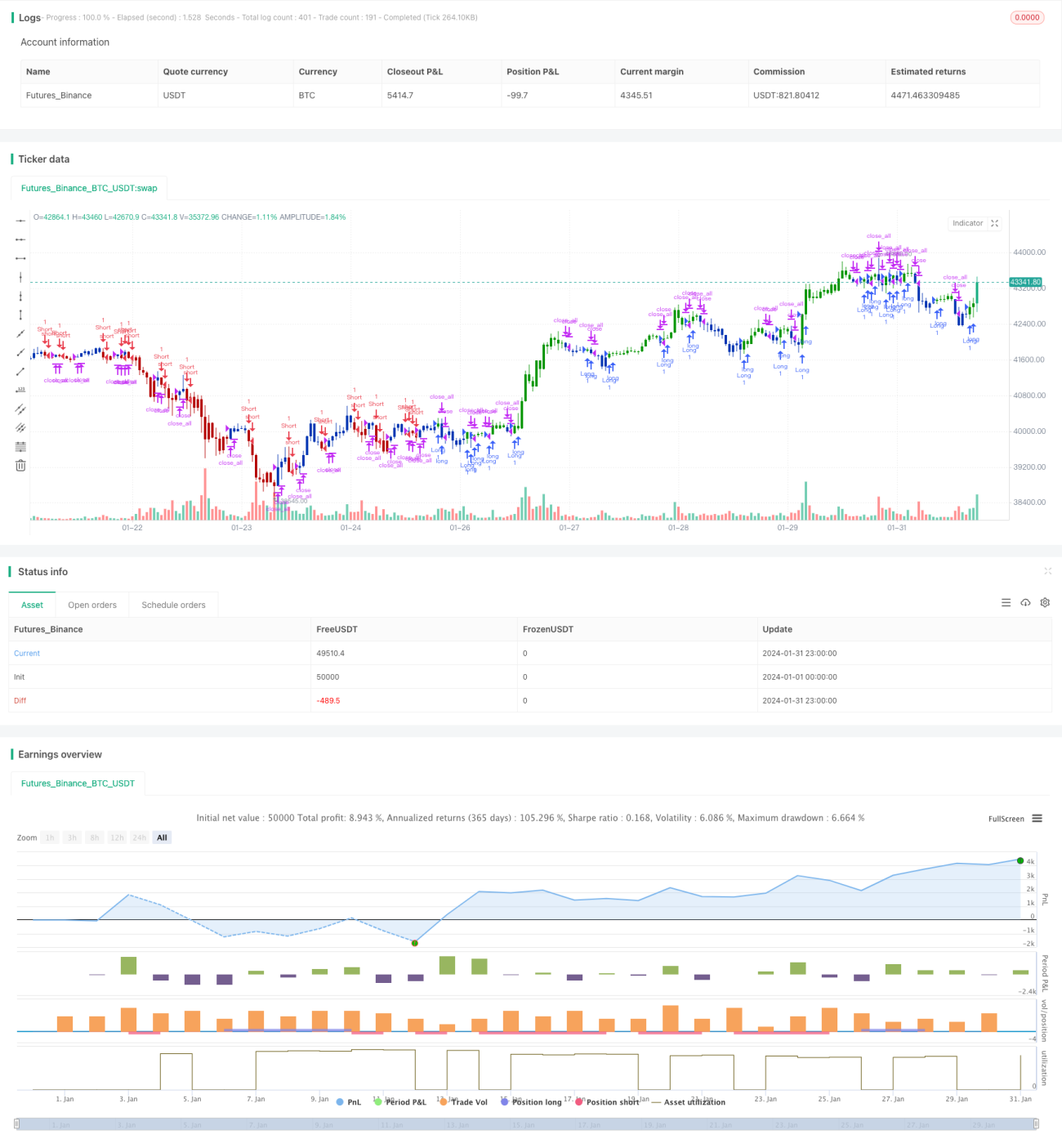

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/05/2021

// This is combo strategies for get a cumulative signal. - 1