Strategi Dagangan Pelbagai Jangka Masa Berdasarkan Petunjuk Pemampatan

Gambaran Keseluruhan

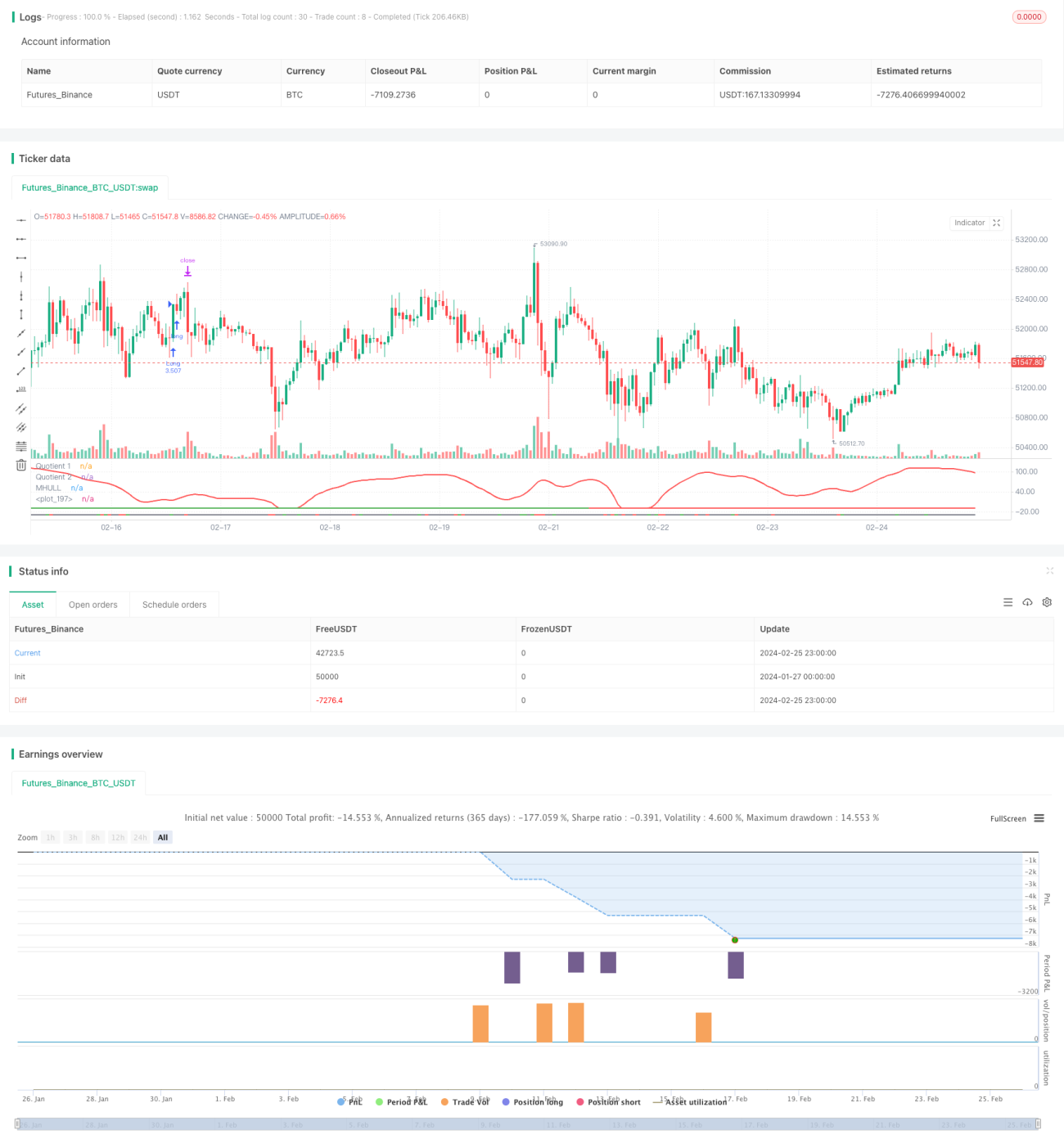

Strategi ini menggabungkan tiga penunjuk iaitu Boom Hunter, Hull Suite dan Volatility Oscillator untuk melaksanakan strategi kuantitatif bagi mengesan trend dan perdagangan pecahan (breakout) dalam rangka masa berbilang. Strategi ini sesuai untuk aset digital seperti Bitcoin yang mempunyai volatiliti tinggi dan pergerakan harga secara mendadak.

Prinsip

Logik teras strategi ini berdasarkan tiga penunjuk berikut:

-

Boom Hunter: Satu osilator yang menggunakan teknik pemampatan penunjuk, menjana isyarat beli dan jual melalui persilangan dua penunjuk (Quotient1 dan Quotient2).

-

Hull Suite: Satu set penunjuk purata bergerak licin yang menentukan arah trend melalui hubungan antara jalur tengah, jalur atas dan jalur bawah.

-

Volatility Oscillator: Satu osilator yang mengukur maklumat volatiliti harga.

Logik kemasukan strategi ini adalah apabila dua penunjuk Quotient Boom Hunter bersilang ke atas atau ke bawah, pada masa yang sama harga perlu menembusi jalur tengah Hull dan menunjukkan perbezaan (divergence) dengan jalur atas atau bawah, manakala penunjuk Volatility berada di zon terlebih beli atau terlebih jual. Ini dapat menapis isyarat pecahan palsu dan meningkatkan ketepatan kemasukan.

Henti rugi (stop loss) ditetapkan dengan mencari lembah terendah atau puncak tertinggi dalam tempoh tertentu (lalai 20 batang lilin), manakala keuntungan diperoleh melalui peratusan henti rugi didarab dengan nisbah ambil untung yang dikonfigurasikan (lalai 3 kali ganda). Saiz posisi dikira berdasarkan peratusan jumlah aset akaun (lalai 3%) dan jarak henti rugi spesifik instrumen.

Kelebihan

- Menggunakan teknik penunjuk mampatan untuk mengekstrak isyarat perdagangan utama daripada harga, meningkatkan kebarangkalian keuntungan

- Gabungan berbilang penunjuk untuk mengesahkan, mengelakkan pecahan palsu, dan menentukan arah trend dengan tepat

- Penetapan henti rugi dan ambil untung dinamik untuk menjejak trend dengan risiko terkawal

- Menggunakan penunjuk volatiliti untuk memastikan perdagangan dalam persekitaran volatiliti tinggi

- Analisis rangka masa berbilang untuk meningkatkan kestabilan strategi

Risiko

- Penunjuk Boom Hunter mungkin mengalami herotan mampatan, menyebabkan isyarat palsu

- Jalur tengah Hull Suite mempunyai ketinggalan, tidak dapat menjejak perubahan harga dengan segera

- Apabila volatiliti menurun, peluang perdagangan mungkin terlepas atau mencetuskan kerugian penutupan

Kaedah penyelesaian:

- Laraskan parameter penunjuk mampatan untuk mengimbangi sensitiviti penunjuk

- Cuba gunakan purata bergerak eksponen seperti EHMA untuk menggantikan penunjuk jalur tengah

- Tambah penunjuk penilaian lain untuk mengelakkan kekeliruan daripada volatiliti

Pengoptimuman

Strategi ini boleh dioptimumkan dari beberapa aspek berikut:

-

Pengoptimuman Parameter: Tukar parameter penunjuk seperti tempoh kitaran, faktor mampatan, dsb. untuk mendapatkan kombinasi parameter terbaik.

-

Pengoptimuman Rangka Masa: Uji rangka masa yang berbeza (1 minit, 5 minit, 30 minit, dsb.) untuk mencari kitaran perdagangan yang paling sesuai.

-

Pengoptimuman Saiz Posisi: Ubah saiz dan nisbah posisi setiap dagangan untuk mencari skim penggunaan dana yang optimum.

-

Pengoptimuman Henti Rugi: Laraskan kedudukan henti rugi mengikut pasangan dagangan yang berbeza untuk mencapai nisbah risiko-pulangan terbaik.

-

Pengoptimuman Syarat: Tambah atau kurangkan syarat penapisan penunjuk untuk mendapatkan masa kemasukan yang lebih tepat.

Kesimpulan

Strategi ini menggunakan gabungan tiga penunjuk iaitu Boom Hunter, Hull Suite dan Volatility Oscillator untuk melaksanakan perdagangan menjejak trend dalam berbilang rangka masa, mampu mengenal pasti pergerakan harga secara mendadak dengan berkesan, sesuai untuk aset digital yang mempunyai volatiliti tinggi. Strategi ini mempunyai risiko terkawal, dan melalui pengoptimuman pelbagai aspek seperti parameter, syarat penapisan dan henti rugi, ia mempunyai kebolehpraktisan dan kebolehkembangan yang tinggi.

- 1