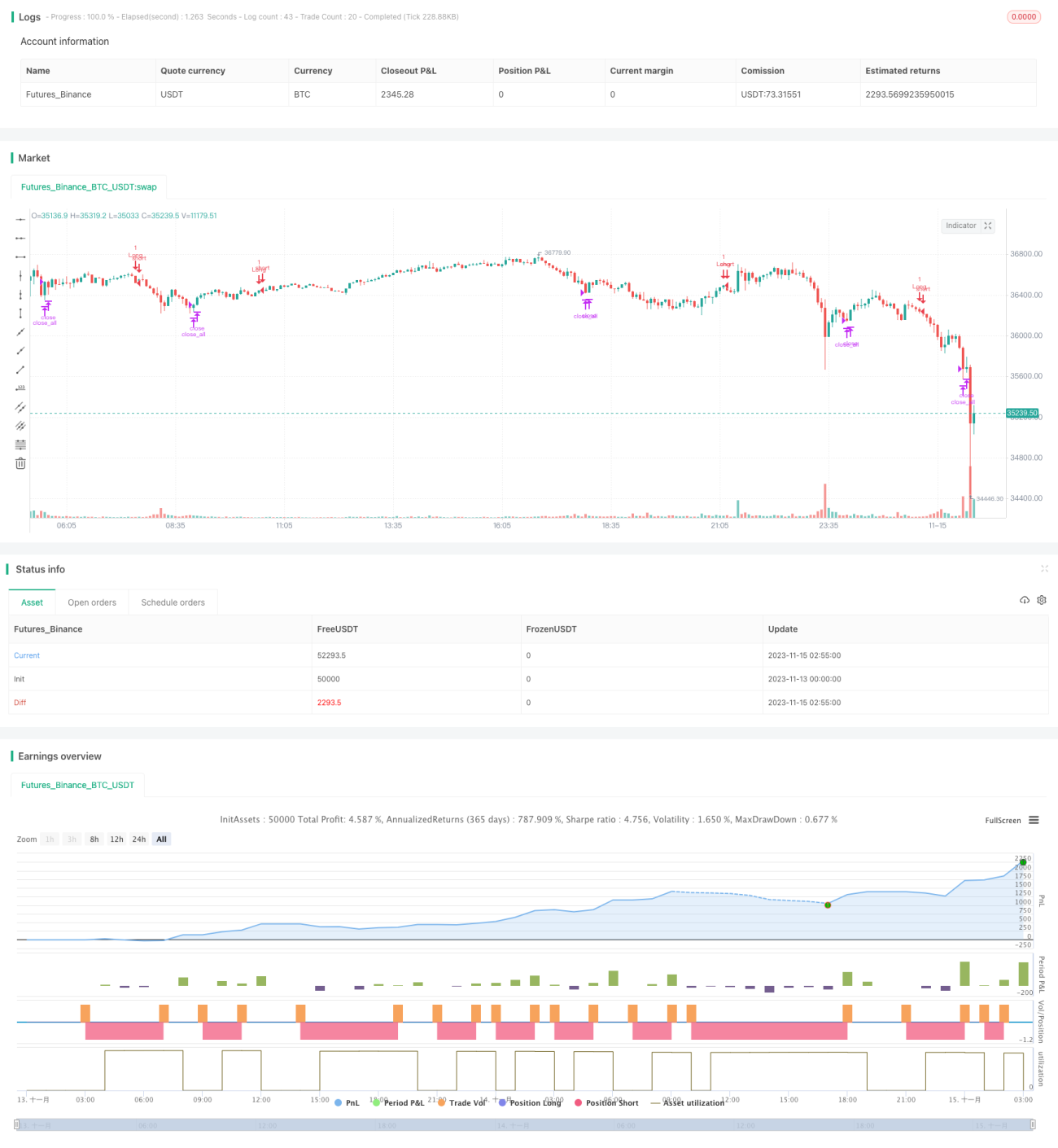

Estratégia de Reversão Múltipla Baseada em Média de Tendência

Visão Geral

Esta estratégia calcula vários indicadores de tendência e realiza operações de compra e venda quando eles se invertem. Os principais indicadores de tendência são TDI, TCF, TTF e TII. A estratégia seleciona na configuração qual indicador utilizar para gerar sinais de negociação.

Princípio da Estratégia

-

Indicador TDI

O indicador TDI é calculado com base no momentum da variação de preço, utilizando técnicas de soma e suavização. Quando o indicador de direção TDI cruza acima da curva TDI, assume-se posição comprada (long); quando cruza abaixo, fecha-se a posição.

-

Indicador TCF

O indicador TCF calcula as variações positivas e negativas do preço para determinar a força dos compradores e vendedores. Quando a força das variações positivas é maior que a das variações negativas, assume-se posição comprada; caso contrário, fecha-se a posição.

-

Indicador TTF

O indicador TTF compara a força das máximas e mínimas para determinar a tendência. O sinal de compra ocorre quando o TTF cruza acima de 100; caso contrário, fecha-se a posição.

-

Indicador TII

O indicador TII combina médias móveis e faixas de preço para identificar reversões de tendência. Ele considera tendências de curto e longo prazo. O sinal de compra ocorre quando o TII cruza acima de 80, e o de fechamento quando cruza abaixo de 80.

A lógica de entrada em posição comprada e de fechamento seleciona o sinal de negociação apropriado de acordo com o indicador configurado.

Vantagens da Estratégia

Esta estratégia combina vários indicadores comuns de negociação de tendências, permitindo adaptação flexível às condições do mercado. As vantagens específicas incluem:

- Utilizar sinais de reversão de tendência para capturar oportunidades de mudança de tendência em tempo hábil.

- Configurar diferentes indicadores para otimização direcionada.

- Rica combinação de indicadores que pode ser utilizada em conjunto para confirmar sinais.

Riscos da Estratégia

Esta estratégia enfrenta principalmente os seguintes riscos:

- Sinais de negociação gerados por indicadores de tendência podem resultar em falsos alarmes, levando a perdas.

- Um único indicador não consegue avaliar completamente a tendência, estando suscetível a ruídos do mercado.

- Parâmetros de indicadores e de negociação configurados incorretamente podem distorcer a leitura do mercado, gerando operações errôneas.

As seguintes medidas podem ser adotadas para reduzir os riscos:

- Otimizar os parâmetros dos indicadores para encontrar a melhor combinação.

- Combinar sinais de múltiplos indicadores para negociação, melhorando a qualidade dos sinais.

- Ajustar a estratégia de gerenciamento de posição para controlar perdas individuais.

Direções de Otimização da Estratégia

Esta estratégia pode ser otimizada nos seguintes aspectos:

- Testar as melhores combinações de indicadores e parâmetros para diferentes ciclos de mercado.

- Adicionar ou remover indicadores para encontrar a combinação ideal.

- Filtrar os sinais de negociação para eliminar falsos alarmes.

- Otimizar a estratégia de gerenciamento de posição, como posição variável, stop-loss móvel, etc.

- Adicionar pontuações de aprendizado de máquina para auxiliar na avaliação da qualidade dos sinais.

Resumo

Esta estratégia combina as vantagens de vários indicadores de reversão de tendência, otimizando a configuração de indicadores e parâmetros para se adaptar a diferentes condições de mercado, operando nos pontos de reversão. O essencial é encontrar a melhor combinação de parâmetros e indicadores, ao mesmo tempo que se controlam os riscos. Através de otimização e validação contínuas, é possível construir uma estratégia estável com alpha.

- 1