Estratégia adaptativa de stop loss e take profit baseada em duplo timeframe e indicador de momentum

Visão Geral

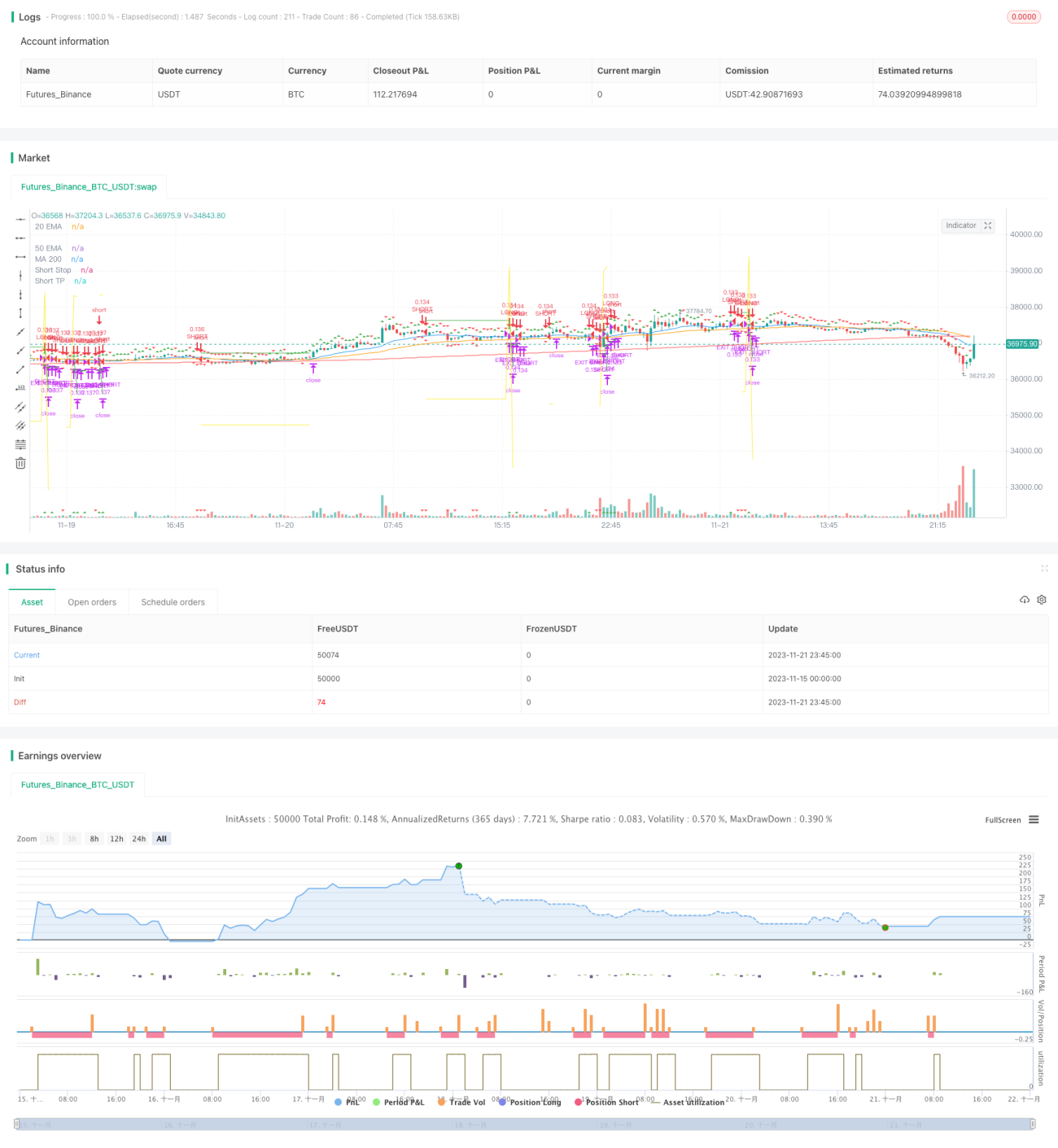

Esta estratégia utiliza uma combinação de dois períodos de tempo e indicadores de momentum para implementar stop loss e take profit adaptativos. O período de tempo principal monitora a direção da tendência, enquanto o período de tempo auxiliar é usado para confirmar os sinais. Quando ambos estão alinhados na mesma direção, um sinal de negociação é gerado. Após a entrada, utiliza-se um método progressivo de take profit para atualizar os níveis de take profit e stop loss.

Princípio da Estratégia

-

O período de tempo principal usa o indicador de regressão linear Squeeze Momentum (SQM) para determinar a tendência. O período de tempo auxiliar utiliza uma combinação de médias exponenciais (EMA) do SQM para filtrar sinais falsos.

-

Quando o SQM do gráfico principal rompe para cima e o SQM do gráfico auxiliar também está para cima, opera-se comprado. Quando o SQM do gráfico principal rompe para baixo e o SQM do gráfico auxiliar também está para baixo, opera-se vendido.

-

Após a entrada, os níveis iniciais de take profit e stop loss são definidos com base nos parâmetros de entrada. Quando o preço atinge o nível de take profit, os níveis de take profit e stop loss são atualizados. Especificamente: o take profit aumenta progressivamente de acordo com a proporção definida, enquanto o stop loss diminui proporcionalmente, realizando um take profit gradual.

Vantagens da Estratégia

-

O uso de dois períodos de tempo filtra sinais falsos, garantindo a precisão dos sinais.

-

O indicador SQM determina a direção da tendência, evitando interferências do ruído do mercado.

-

O mecanismo adaptativo de take profit e stop loss maximiza a retenção de lucros e controla efetivamente os riscos.

Análise de Riscos

-

A configuração inadequada dos parâmetros do indicador SQM pode perder pontos de reversão da tendência, resultando em perdas.

-

A escolha inadequada do período de tempo do gráfico auxiliar pode não filtrar efetivamente o ruído, gerando negociações errôneas.

-

A amplitude do stop loss pode ser excessiva, resultando em perdas significativas por operação.

Direções de Otimização

-

Os parâmetros do indicador SQM precisam ser ajustados de acordo com os diferentes mercados para garantir sua sensibilidade.

-

O período de tempo do gráfico auxiliar também deve ser testado em diferentes ciclos para determinar qual oferece a melhor filtragem.

-

A amplitude do stop loss pode ser definida como um intervalo variável, em vez de um valor fixo, permitindo ajustes conforme a volatilidade do mercado.

Resumo

No geral, esta estratégia é bastante prática. A combinação de dois períodos de tempo com o indicador de momentum para julgar a tendência, juntamente com o método adaptativo de take profit e stop loss, permite obter lucros estáveis. Otimizando os parâmetros do SQM, o período do gráfico auxiliar e a configuração da amplitude do stop loss, é possível melhorar ainda mais o desempenho da estratégia, tornando-a digna de aplicação e otimização em negociações reais.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1