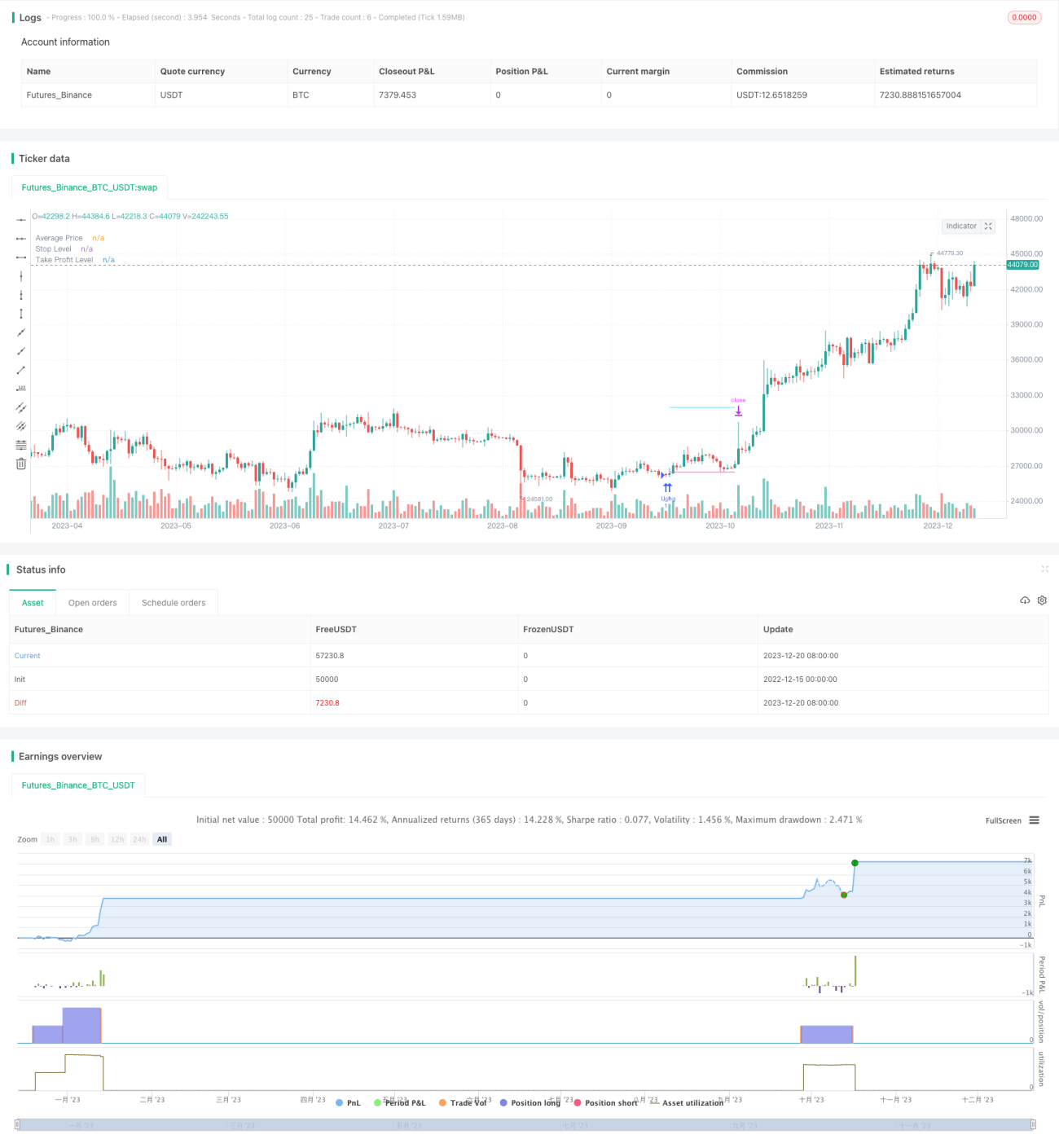

Estratégia de rastreamento de baixo risco da pirâmide de mínimos

Esta estratégia combina diferentes indicadores para identificar potenciais pontos baixos no movimento de preços e utiliza um rastreamento em pirâmide para construir posições gradualmente, reduzindo o risco. A estratégia também incorpora funções como stop loss, take profit e stop loss móvel, permitindo um controle de risco eficaz.

Visão Geral da Estratégia

A estratégia primeiro usa a diferença entre o RSI e a EMA do RSI para identificar potenciais pontos baixos nos preços. Para filtrar sinais falsos, a estratégia também combina médias móveis e um oscilador estocástico de múltiplos períodos de tempo para confirmação. Uma vez que um sinal de ponto baixo é confirmado, posições longas são abertas gradualmente em um nível ligeiramente inferior a esse ponto – este é o conceito de rastreamento em pirâmide. A estratégia permite abrir até 12 ordens de rastreamento, com o volume de cada ordem aumentando sequencialmente, o que efetivamente diversifica o risco. Todas as ordens seguem um stop loss geral para saída, e também é possível definir um take profit individual para cada ordem. Para controlar ainda mais o risco, a estratégia também possui um stop loss geral baseado em uma porcentagem do patrimônio da conta.

Princípio da Estratégia

A estratégia é composta por três módulos principais: o módulo de identificação de pontos baixos, o módulo de rastreamento em pirâmide e o módulo de controle de risco.

Módulo de Identificação de Pontos Baixos: Utiliza a diferença entre o indicador RSI e sua EMA para identificar potenciais pontos baixos dos preços. Para melhorar a precisão, são introduzidos indicadores de média móvel e o oscilador estocástico de múltiplos períodos de tempo para filtrar os sinais. O sinal de ponto baixo é confirmado apenas quando o preço está abaixo da média móvel e a linha K do oscilador estocástico está abaixo de 30.

Módulo de Rastreamento em Pirâmide: Este é o núcleo da estratégia. Uma vez que o sinal de ponto baixo é confirmado, a estratégia abre a primeira ordem em um nível 0,1% abaixo desse ponto baixo. A partir daí, se o preço continuar caindo e ficar abaixo do preço médio de entrada por uma certa proporção, ordens longas adicionais são abertas. O volume das novas ordens aumenta progressivamente; por exemplo, o volume da terceira ordem é três vezes o da primeira. Esse método de rastreamento em pirâmide permite distribuir o risco. A estratégia permite abrir até 12 ordens de rastreamento.

Módulo de Controle de Risco: Inclui principalmente três aspectos. Primeiro, o stop loss geral, calculado com base no preço mais alto de um período recente. Todas as ordens seguem esse stop loss simultaneamente. Segundo, o take profit independente para cada ordem, que pode ser definido como uma porcentagem do preço de entrada. Terceiro, um stop loss geral baseado na porcentagem do patrimônio da conta, que é a medida de controle de risco mais forte.

Vantagens da Estratégia

- Utiliza o rastreamento em pirâmide para reduzir o risco de ordens individuais, ao mesmo tempo que distribui o risco geral.

- Combinação de múltiplos indicadores melhora a precisão na identificação de pontos baixos.

- Funções de stop loss geral, take profit e stop loss móvel controlam o risco efetivamente.

- Mecanismo de stop loss baseado em porcentagem do patrimônio protege a conta de perdas significativas.

- Permite ajustar parâmetros para encontrar um equilíbrio entre risco e retorno.

Riscos da Estratégia

- A precisão na identificação de pontos baixos ainda tem limitações, podendo perder o ponto de entrada ideal ou entrar em sinais falsos.

- Ao adicionar ordens, pode-se enfrentar movimentos desfavoráveis do mercado, agravando as perdas.

- Requer um período de operação mais longo para que as vantagens da estratégia se manifestem.

- Uma configuração inadequada de parâmetros pode levar a um controle de risco insuficiente.

Para mitigar os riscos acima, pode-se otimizar nos seguintes aspectos:

- Substituir ou adicionar indicadores para melhorar a precisão da identificação de pontos baixos.

- Otimizar parâmetros como quantidade de ordens, intervalo e amplitude do take profit para reduzir o risco de cada ordem.

- Encurtar adequadamente a amplitude do stop loss para proteger os lucros.

- Testar em diferentes ativos, escolhendo aqueles com boa liquidez e maior volatilidade.

Direções de Otimização da Estratégia

A estratégia ainda possui espaço para otimização adicional:

- Introduzir técnicas mais avançadas, como aprendizado de máquina, para identificar pontos baixos.

- Ajustar dinamicamente parâmetros como quantidade de ordens e amplitude do stop loss de acordo com as condições do mercado.

- Adicionar uma estratégia de stop loss dentro de uma faixa para evitar o agravamento das perdas.

- Adicionar um mecanismo de reentrada.

- Otimizar parâmetros da estratégia para ações e criptomoedas.

Resumo

Esta estratégia reduz efetivamente o risco de ordens individuais através do conceito de rastreamento em pirâmide, e funções como stop loss geral, take profit e stop loss móvel também desempenham um bom papel no controle de risco. No entanto, ainda há espaço para otimização na identificação de pontos baixos e outros aspectos. Se técnicas mais avançadas forem introduzidas, juntamente com a capacidade de ajustar parâmetros dinamicamente e combinadas com a otimização de parâmetros, a relação risco-retorno desta estratégia será significativamente melhorada.

- 1