Estratégia Otimizada de Cruzamento de Médias Móveis em Múltiplos Períodos

1

Follow

1802

Followers

Visão Geral

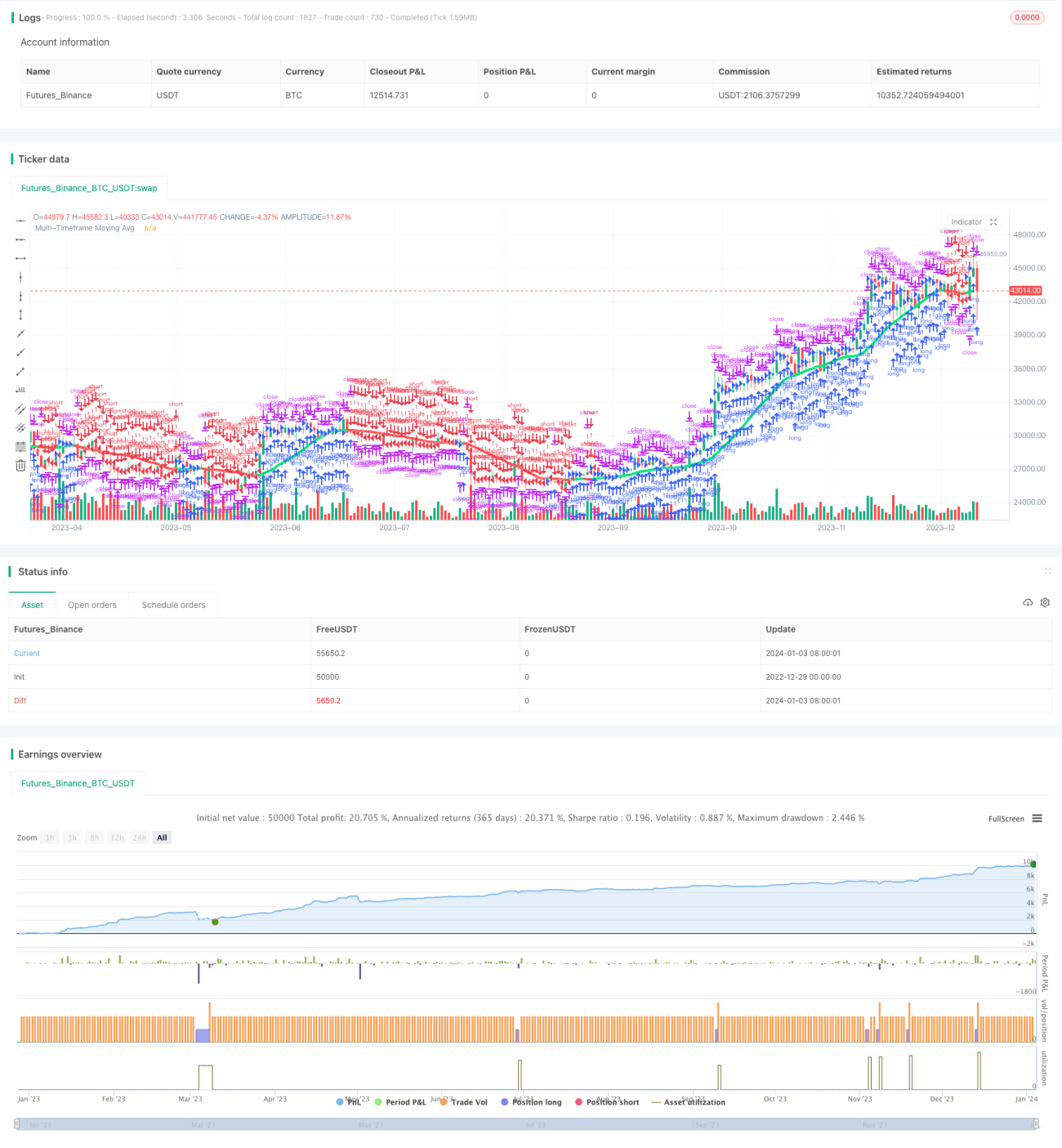

Esta estratégia é baseada na reescrita do famoso indicador CM_Ultimate_MA_MTF, permitindo traçar médias móveis em múltiplas escalas de tempo e realizar operações de cruzamento entre médias móveis de diferentes períodos. A estratégia também inclui uma função de stop loss móvel.

Princípio da Estratégia

- De acordo com a escolha do usuário, diferentes tipos de indicadores de média móvel são usados para traçar linhas de MA no período principal do gráfico e em períodos superiores.

- Quando a MA de ciclo rápido cruza acima da MA de ciclo lento, é gerado sinal de compra (long); quando a MA de ciclo rápido cruza abaixo da MA de ciclo lento, é gerado sinal de venda (short).

- Adiciona um mecanismo de stop loss móvel para controlar ainda mais o risco.

Análise de Vantagens

- O cruzamento de MAs em múltiplas escalas de tempo pode melhorar a qualidade dos sinais e reduzir sinais falsos.

- A combinação de diferentes tipos de MA aproveita as vantagens de cada indicador, aumentando a estabilidade.

- O stop loss móvel ajuda a limitar perdas em tempo hábil, reduzindo a probabilidade de grandes prejuízos.

Análise de Riscos

- Os indicadores de MA são defasados, podendo perder oportunidades de curto prazo.

- É necessário otimizar adequadamente os parâmetros dos períodos das MAs, caso contrário podem ser gerados muitos sinais falsos.

- Uma configuração inadequada do nível de stop loss pode causar saídas desnecessárias.

Direções de Otimização

- Testar diferentes combinações de parâmetros de MA para encontrar os melhores valores.

- Adicionar filtros de outros indicadores para melhorar a qualidade dos sinais.

- Otimizar a estratégia de stop loss para torná-la mais adequada às características do mercado.

Conclusão

Esta estratégia integra a análise de médias móveis em múltiplos períodos com o método de stop loss móvel, visando melhorar a qualidade dos sinais e controlar o nível de risco. Através da otimização de parâmetros e da adição de outros indicadores, é possível aprimorar ainda mais o desempenho da estratégia.

Source

Pine

Strategy parameters

Related strategies

Comment

All comments (0)

No data

- 1