Estratégia Quantitativa de Seguimento de Tendência Dupla

Visão Geral

A ideia central desta estratégia é combinar a estratégia de reversão 123 com o indicador oscilador Rainbow, realizando um duplo rastreamento de tendência para aumentar a taxa de acerto. A estratégia ajusta dinamicamente as posições acompanhando as tendências de preço de curto e médio prazo, buscando obter retornos excedentes em relação ao mercado.

Princípio da Estratégia

A estratégia é composta por duas partes:

-

Estratégia de reversão 123: Se o preço de fechamento caiu nos dois dias anteriores e subiu no dia de hoje, e a linha lenta K de 9 períodos está abaixo de 50, então comprar; se o preço de fechamento subiu nos dois dias anteriores e caiu no dia de hoje, e a linha rápida K de 9 períodos está acima de 50, então vender.

-

Indicador oscilador Rainbow: Este indicador reflete o desvio do preço em relação às médias móveis. Quando o indicador está acima de 80, indica que o mercado tende à instabilidade; quando abaixo de 20, indica que o mercado tende à reversão.

Esta estratégia combina ambos: quando os sinais de compra e venda aparecem simultaneamente, abre-se posição; caso contrário, fecha-se a posição.

Análise de Vantagens

A estratégia apresenta as seguintes vantagens:

- Dupla filtragem, melhorando a qualidade do sinal e reduzindo a taxa de falso julgamento.

- Ajuste dinâmico de posições, reduzindo perdas em movimentos direcionais.

- Integração de indicadores de curto e médio prazo, aumentando a estabilidade da estratégia.

Análise de Riscos

A estratégia também apresenta os seguintes riscos:

- A otimização inadequada dos parâmetros pode levar ao overfitting.

- A abertura dupla de posições aumenta os custos de transação.

- Em momentos de forte volatilidade do preço do ativo, o stop loss pode ser facilmente rompido.

Esses riscos podem ser mitigados ajustando os parâmetros, otimizando o gerenciamento de posições e configurando stop losses de forma adequada.

Direções de Otimização

A estratégia pode ser otimizada nos seguintes aspectos:

- Otimizar os parâmetros para encontrar a melhor combinação.

- Adicionar um módulo de gerenciamento de posições que ajuste dinamicamente conforme a volatilidade e o drawdown.

- Adicionar um módulo de stop loss com stop loss móvel adequado.

- Incorporar algoritmos de aprendizado de máquina para auxiliar na identificação de pontos de reversão de tendência.

Resumo

Esta estratégia integra a estratégia de reversão 123 com o oscilador Rainbow, realizando um duplo rastreamento de tendência. Mantendo uma estabilidade relativamente alta, oferece espaço para retornos excedentes. Com otimizações contínuas, espera-se aumentar ainda mais a taxa de retorno da estratégia.

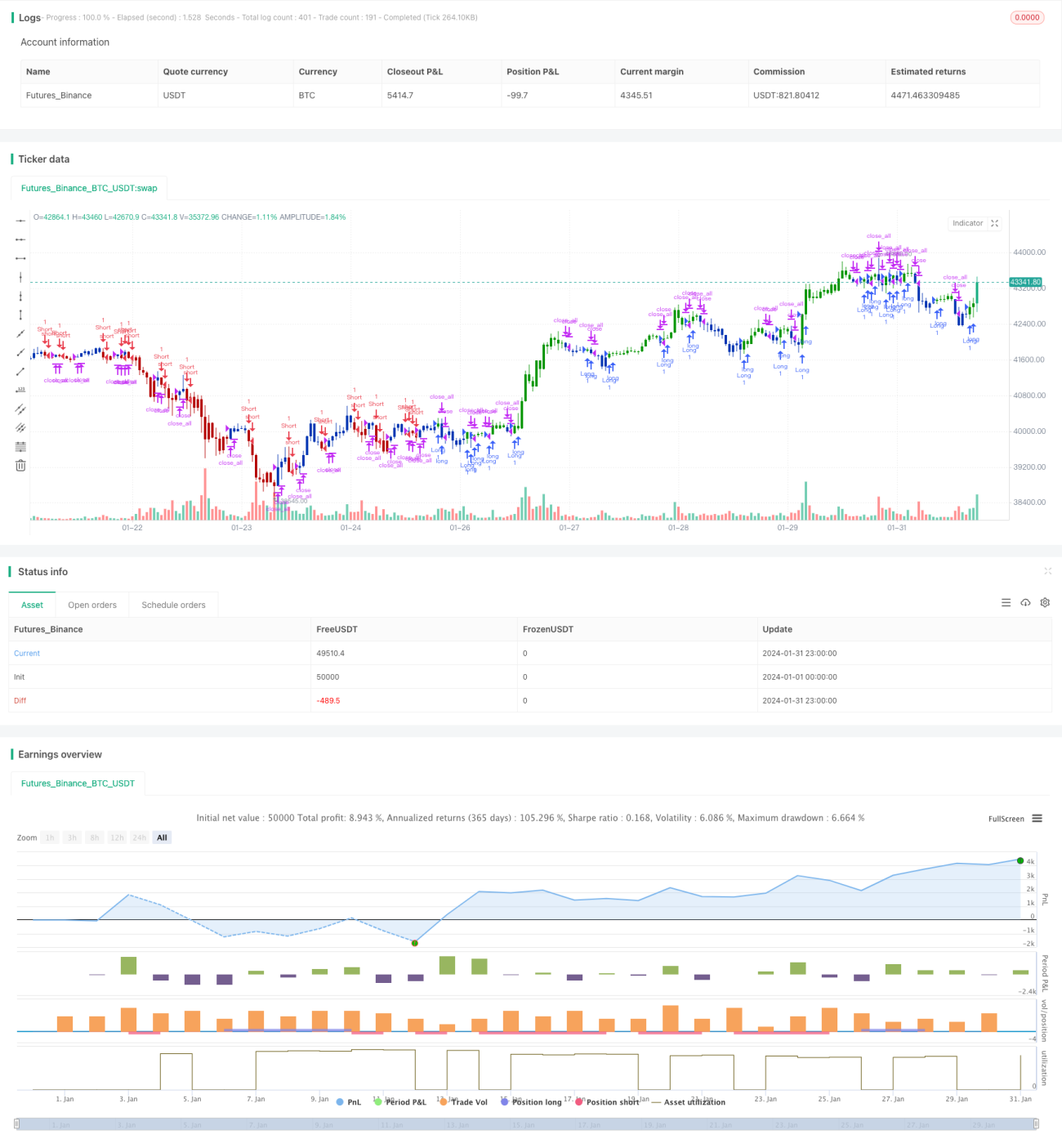

/*backtest

start: 2024-01-01 00:00:00

end: 2024-01-31 23:59:59

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 25/05/2021

// This is combo strategies for get a cumulative signal. - 1