Стратегия пересечения скользящих средних

Обзор

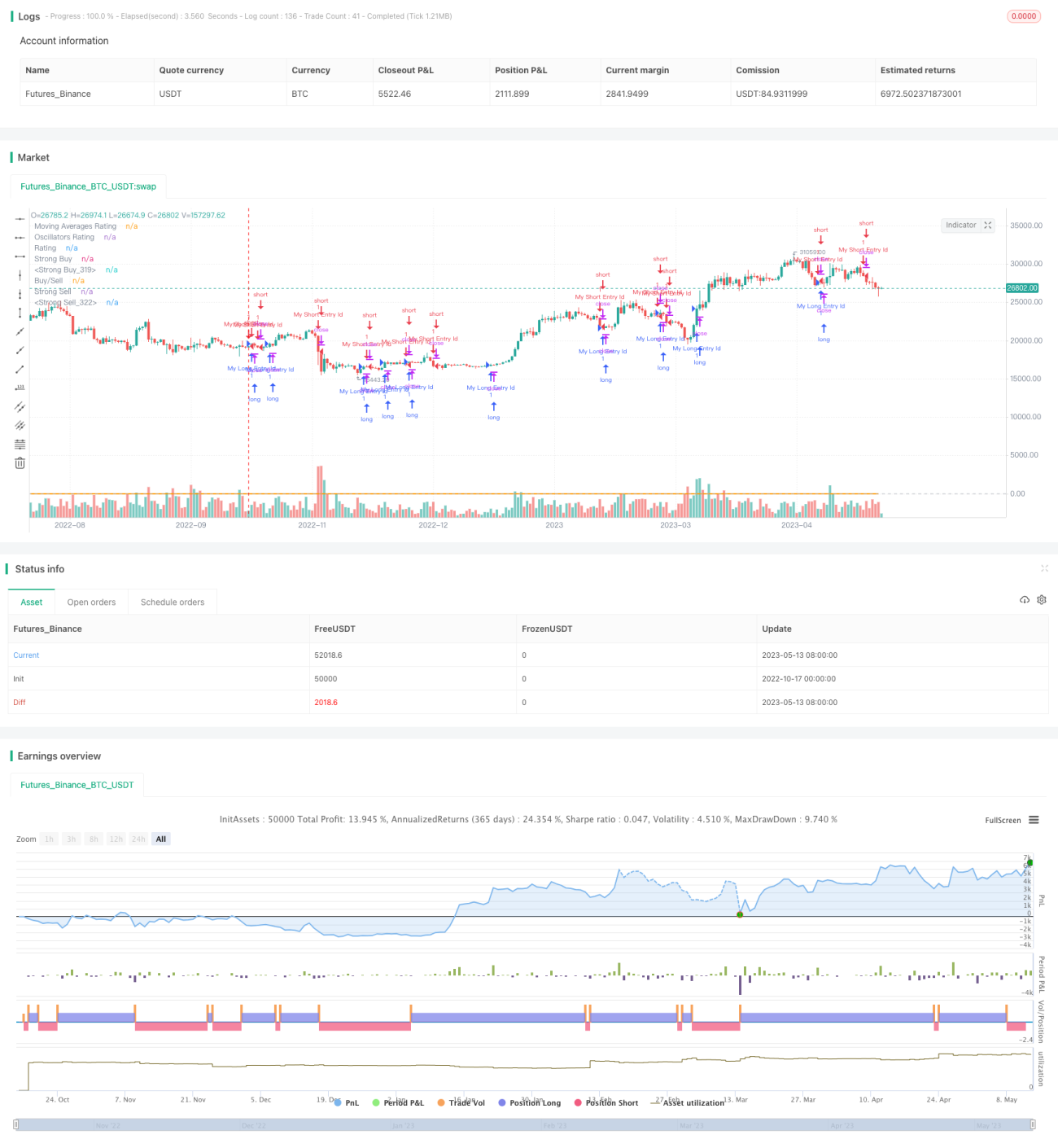

Данная стратегия использует различные технические индикаторы, такие как скользящие средние и осцилляторы, в сочетании с паттернами пересечения скользящих средних для идентификации тенденций цен акций и точек разворота, а также для выполнения операций покупки и продажи.

Принцип

Стратегия в основном состоит из следующих частей:

- Выбор интервала: Установка временного интервала для свечного графика, например, 1 минута, 5 минут и т.д.

- Выбор скользящих средних: Настройка параметров常用的 EMA, SMA и других скользящих средних, например, 10-дневная, 20-дневная линии и т.д.

- Выбор осцилляторов: Настройка параметров осцилляторов, таких как RSI, MACD, Williams %R и других.

- Расчет сигналов покупки и продажи: С помощью пользовательских функций вычисляются значения скользящих средних и осцилляторов. Когда краткосрочная скользящая средняя пересекает долгосрочную скользящую среднюю снизу вверх, генерируется сигнал покупки; когда краткосрочная скользящая средняя пересекает долгосрочную сверху вниз, генерируется сигнал продажи. При этом используются индикаторы перекупленности/перепроданности для выявления экстремальных точек.

- Рейтинговая система: Каждый индикатор получает числовую оценку сигналов покупки и продажи, затем вычисляется среднее значение, что дает общий рейтинговый индекс. Если рейтинговый индекс больше 0, это сигнал покупки; если меньше 0 – сигнал продажи.

- Торговые сигналы: На основе того, больше или меньше рейтинговый индекс нуля, генерируется окончательный торговый сигнал для выполнения операции покупки или продажи.

Стратегия использует комбинацию нескольких индикаторов, что позволяет эффективно определять ценовые тенденции и точки разворота, повышая надежность сигналов. Пересечение скользящих средних является проверенным техническим сигналом тренда, а его комбинация с осцилляторами помогает избежать ложных пробоев. Рейтинговая система также делает торговые сигналы более четкими.

Преимущества

- Сочетание пересечения скользящих средних и нескольких осцилляторов делает торговые сигналы более надежными, избегая ложных сигналов.

- Рейтинговая система делает сигналы покупки и продажи более четкими.

- Модульное программирование с использованием пользовательских функций обеспечивает четкую структуру кода.

- Использование нескольких временных периодов для комбинированного анализа повышает точность.

- Оптимизированы настройки параметров, такие как длина RSI, периоды быстрой и медленной скользящих средних MACD и т.д.

- Возможность настройки индикаторов и параметров скользящих средних через параметры повышает гибкость.

Существующие риски

- В условиях общего рыночного тренда существуют различия в поведении отдельных акций.

- Частота торговли может быть высокой, что увеличивает транзакционные издержки и риск проскальзывания.

- Требуется многократное тестирование и оптимизация параметров для адаптации к характеристикам различных акций.

- Существует определенный риск просадки и убытков.

Следующие методы могут снизить указанные выше риски:

- Отбор акций с учетом общего рыночного тренда.

- Соответствующая корректировка времени удержания позиции для снижения частоты торговли.

- Оптимизация настроек параметров для лучшего соответствия характеристикам конкретной акции.

- Использование стратегии стоп-лосса для контроля убытков.

Направления оптимизации

Данную стратегию можно дополнительно оптимизировать в следующих аспектах:

- Добавление большего количества индикаторов, таких как индикаторы волатильности, для усиления сигналов.

- Использование методов машинного обучения для автоматической оптимизации параметров.

- Добавление модулей выбора отдельных акций и отраслей.

- Интеграция методов количественного отбора акций.

- Использование адаптивных стоп-лоссов, трейлинг-стопов и других методов.

- Учет состояния рынка, избегание неопределенных условий.

- Анализ результатов реальной торговли, корректировка весовых коэффициентов оценок.

Таким образом, стратегия, интегрирующая пробой скользящих средних и несколько индикаторов, может эффективно определять ценовое движение. Однако необходимо постоянно тестировать и оптимизировать ее для контроля рисков. В будущем возможны улучшения в области комбинированного отбора акций, оптимизации параметров и стоп-лоссов.

Заключение

Данная стратегия использует пересечение скользящих средних в качестве основного торгового сигнала, дополненного подтверждением от нескольких осцилляторов, и использует систему оценки для генерации четких сигналов покупки и продажи. Она способна эффективно определять ценовые тенденции и точки разворота, но требует контроля частоты торговли для снижения транзакционных издержек и рисков, а также постоянной оптимизации параметров. Стратегия имеет определенную практическую ценность и потенциал для улучшения.

/*backtest

start: 2022-10-17 00:00:00

end: 2023-05-14 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("TV Signal", overlay=true, initial_capital = 500, currency = "USD")

// -------------------------------------- GLOBAL SELECTION --------------------------------------------- //- 1