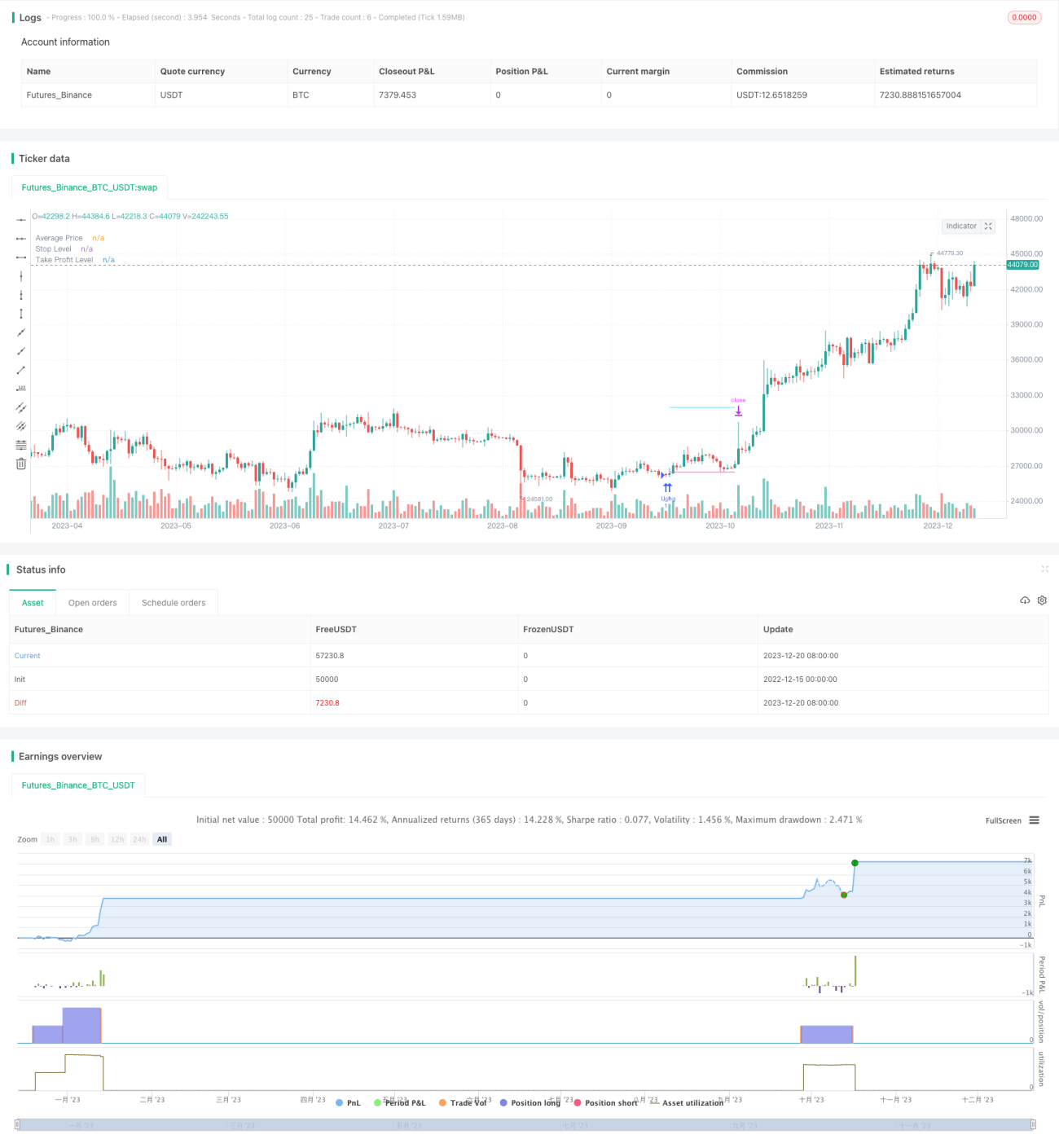

Низкорисковая стратегия пирамидинга от минимумов

Эта стратегия выявляет потенциальные минимумы ценового движения путем комбинации различных индикаторов и снижает риск, используя пирамидальное отслеживание для постепенного открытия позиций. Стратегия также включает функции стоп-лосса, тейк-профита и трейлинг-стопа, что позволяет эффективно контролировать риски.

Обзор стратегии

Стратегия сначала использует разницу между RSI и EMA RSI для выявления потенциальных ценовых минимумов. Для фильтрации ложных сигналов стратегия также использует скользящие средние и мультитаймфреймовый стохастический осциллятор для подтверждения. После подтверждения сигнала минимума позиции открываются постепенно чуть ниже этой точки — это и есть идея отслеживающей пирамиды. Стратегия позволяет открывать до 12 ордеров отслеживания, причем объем каждого последующего ордера увеличивается, что эффективно распределяет риск. Все ордера закрываются по единому общему стоп-лоссу, а также для каждого ордера можно установить индивидуальный тейк-профит. Для дополнительного контроля риска стратегия включает общий стоп-лосс на основе процента от собственного капитала счета.

Принцип работы стратегии

Стратегия состоит из трех основных модулей: модуль выявления минимумов, модуль пирамидального отслеживания и модуль управления рисками.

Модуль выявления минимумов использует разницу между индикатором RSI и его EMA для идентификации потенциальных ценовых минимумов. Для повышения точности также внедряются скользящие средние и мультитаймфреймовый стохастический осциллятор для фильтрации сигналов. Сигнал минимума считается действительным только тогда, когда цена ниже скользящей средней, а линия K стохастического осциллятора ниже 30.

Модуль пирамидального отслеживания является ядром стратегии. После подтверждения сигнала минимума стратегия открывает первый ордер на 0,1% ниже этого минимума. Затем, если цена продолжает снижаться и опускается ниже средней цены входа на определенный процент, добавляются новые лонг-позиции. Объем новых ордеров увеличивается последовательно: например, объем третьего ордера в 3 раза больше первого. Такой пирамидальный подход позволяет усреднять риск. Максимальное количество ордеров отслеживания — 12.

Модуль управления рисками включает три аспекта. Первый — общий стоп-лосс, рассчитываемый на основе максимальной цены за последний заданный период. Все ордера закрываются одновременно по этому стопу. Второй — независимые тейк-профиты для каждого ордера, устанавливаемые как процент от цены входа. Третий — общий стоп-лосс на основе процента от собственного капитала счета, который является самым сильным средством контроля риска.

Преимущества стратегии

- Использование пирамидального отслеживания снижает риск отдельных ордеров, одновременно распределяя общий риск.

- Комбинация нескольких индикаторов повышает точность выявления минимумов.

- Функции общего стоп-лосса, тейк-профита и трейлинг-стопа эффективно контролируют риски.

- Механизм стоп-лосса на основе доли капитала защищает счет от значительных потерь.

- Возможность настройки параметров для поиска баланса между риском и доходностью.

Риски стратегии

- Точность выявления минимумов все еще ограничена, возможны пропуск лучших точек входа или ложные сигналы.

- При добавлении ордеров можно столкнуться с неблагоприятным движением цены, усугубляющим убытки.

- Для демонстрации преимуществ стратегии требуется длительный период работы.

- Неправильная настройка параметров может привести к недостаточному контролю рисков.

Для снижения перечисленных рисков можно провести оптимизацию по следующим направлениям:

- Заменить или добавить индикаторы для повышения точности выявления минимумов.

- Оптимизировать параметры количества ордеров, интервалов и размера тейк-профита, чтобы уменьшить риск по отдельному ордеру.

- Соответственно сократить дистанцию стоп-лосса для защиты прибыли.

- Протестировать на разных инструментах, выбирая высоколиквидные и волатильные.

Направления оптимизации стратегии

Стратегия имеет потенциал для дальнейшего улучшения:

- Попробовать внедрить более продвинутые методы, такие как машинное обучение, для выявления минимумов.

- Динамически регулировать количество ордеров, дистанцию стоп-лосса и другие параметры в зависимости от рыночных условий.

- Добавить стратегию стоп-лосса в рамках диапазона, чтобы избежать расширения убытков.

- Добавить механизм повторного входа.

- Оптимизировать параметры стратегии для акций и криптовалют.

Заключение

Данная стратегия эффективно снижает риск отдельного ордера за счет пирамидального отслеживания, а функции общего стоп-лосса, тейк-профита и трейлинг-стопа обеспечивают хороший контроль рисков. Однако выявление минимумов все еще требует оптимизации. Если внедрить более передовые технологии, добавить динамическую настройку параметров и провести оптимизацию параметров, соотношение доходности к риску данной стратегии значительно возрастет.

- 1