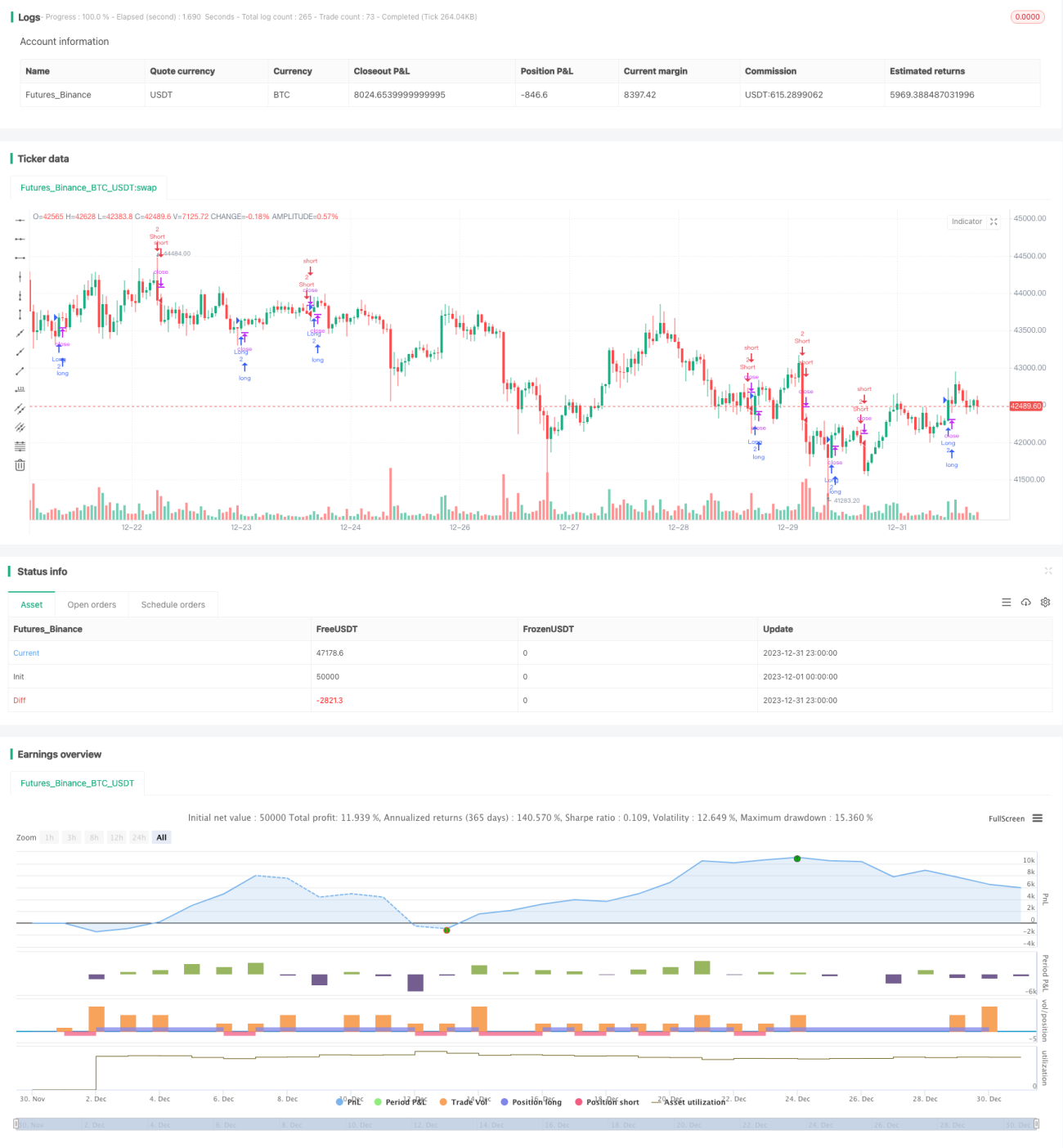

Стратегия двустороннего пробоя на основе K-линий

Обзор

Это торговая стратегия, основанная на двустороннем пробое по свечным графикам. Она генерирует торговые сигналы, когда цена закрытия текущей свечи пробивает максимум и минимум двух предыдущих свечей.

Принцип стратегии

Базовая логика стратегии следующая:

-

Определение бычьего сигнала:

bull = close > open and close > math.max(close[2], open[2]) and low[1] < low[2] and high[1] < high[2]. То есть цена закрытия текущей свечи больше цены открытия и больше максимума двух свечей назад, при этом минимум текущей свечи ниже минимума предыдущей свечи. -

Определение медвежьего сигнала:

bear = close < open and close < math.min(close[2], open[2]) and low[1] > low[2] and high[1] > high[2]. То есть цена закрытия текущей свечи меньше цены открытия и меньше минимума двух свечей назад, при этом максимум текущей свечи выше максимума предыдущей свечи. -

При появлении бычьего сигнала открывается длинная позиция; при появлении медвежьего сигнала — короткая.

-

Можно установить уровни стоп-лосса и тейк-профита.

Стратегия использует характеристику двустороннего пробоя: пробитие ключевых ценовых диапазонов позволяет определить смену тренда и сгенерировать торговый сигнал.

Преимущества

Это относительно простая и интуитивно понятная стратегия пробоя, обладающая следующими преимуществами:

-

Логика ясна, легко понять и реализовать, низкий порог входа.

-

Пробой — распространённый торговый сигнал, который часто приводит к формированию тренда.

-

Одновременная торговля в обе стороны (лонг и шорт) увеличивает возможности получения прибыли.

-

Гибкая настройка стоп-лосса и тейк-профита для контроля риска.

Анализ рисков

Стратегия также имеет некоторые риски:

-

Торговля в обе стороны сопряжена с повышенным риском, требует пристального мониторинга.

-

Пробой может быть ложным, возможны ложные сигналы.

-

Неправильные настройки параметров могут привести к чрезмерной торговле.

-

Неправильная установка стоп-лосса и тейк-профита также влияет на доходность.

Риски можно снизить за счёт оптимизации параметров и тщательного отбора инструментов.

Направления оптимизации

Стратегию можно оптимизировать по следующим направлениям:

-

Оптимизация параметров, например, периода пробоя, размера стоп-лосса и тейк-профита и т.д.

-

Добавление фильтров для исключения ложных сигналов во время флэта или проскальзываний.

-

Комбинирование с трендовыми индикаторами для избежания диапазонной торговли.

-

Оптимизация управления капиталом, улучшение алгоритмов расчёта размера позиции.

-

Для разных инструментов параметры могут отличаться, поэтому их следует тестировать и оптимизировать отдельно.

Заключение

Это простая стратегия, основанная на идее двустороннего пробоя. Она обладает преимуществами ясной логики и лёгкой реализации, но также несёт определённый риск, требующий мониторинга. С помощью оптимизации параметров и условий можно добиться хороших результатов стратегии.

- 1