Chiến lược Siêu xu hướng V

Tổng quan

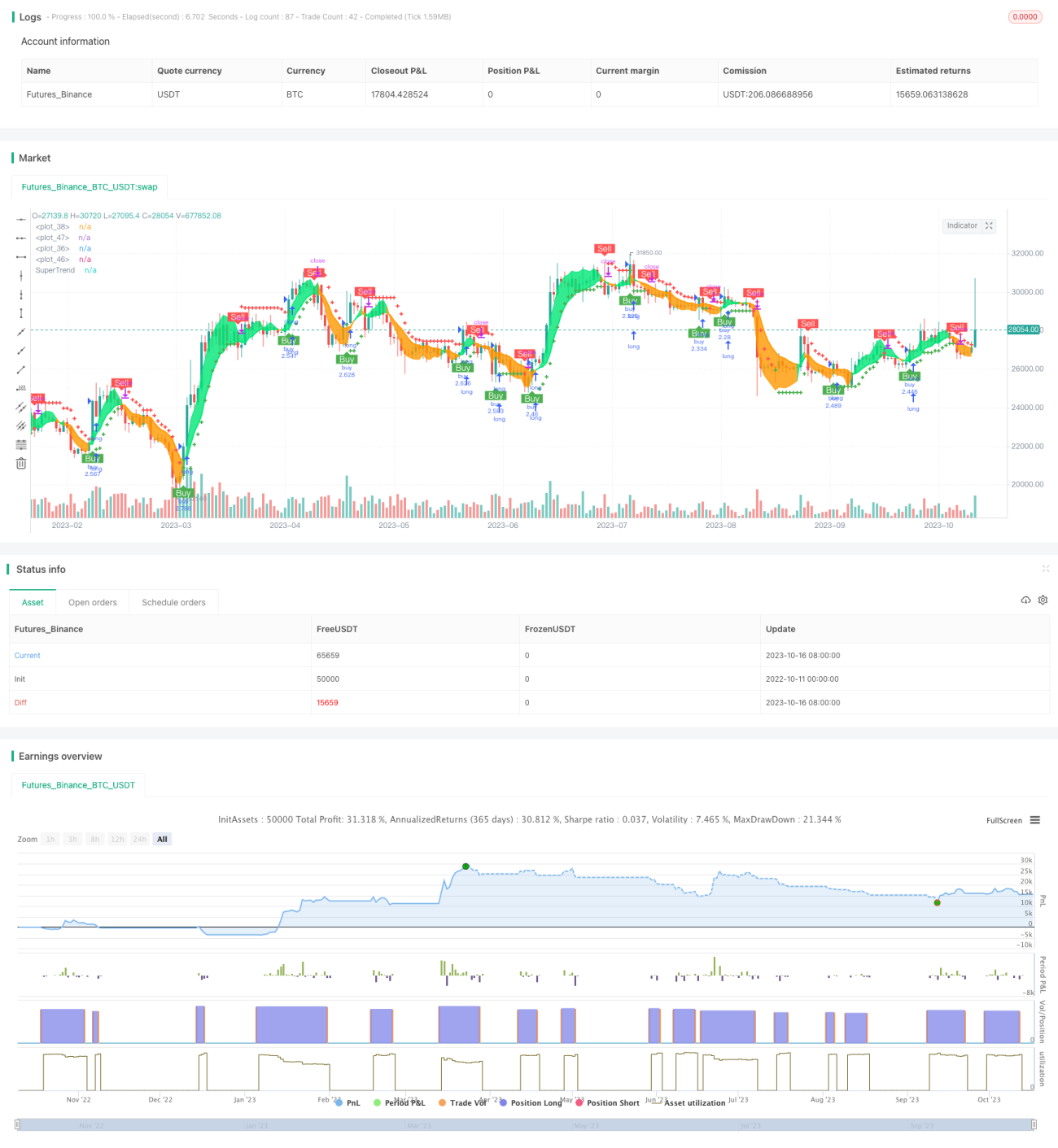

Chiến lược Siêu Xu Hướng V là một chiến lược giao dịch ngắn hạn dựa trên đường trung bình động và độ lệch chuẩn. Nó sử dụng chỉ báo Super Trend để xác định hướng xu hướng giá, kết hợp với hỗ trợ và kháng cự được hình thành từ đường trung bình động để xác định điểm vào lệnh. Đồng thời, nó sử dụng kênh độ lệch chuẩn để dự đoán các vùng hỗ trợ và kháng cự tiềm năng của giá, thiết lập khoảng giá cắt lỗ và chốt lời, tạo thành chiến lược giao dịch ngắn hạn theo xu hướng và thoát lệnh hiệu quả.

Nguyên lý chiến lược

Chiến lược này trước tiên tính toán chỉ báo Super Trend, sử dụng mối quan hệ giữa ATR và giá để xác định hướng xu hướng. Khi giá cao hơn đường xu hướng tăng thì là tín hiệu tăng giá, khi giá thấp hơn đường xu hướng giảm thì là tín hiệu giảm giá.

Sau đó tính đường trung bình động EMA của giá và EMA của giá mở cửa. Khi giá cắt lên trên đường trung bình động và cao hơn EMA giá mở cửa là tín hiệu mua, khi giá cắt xuống dưới đường trung bình động và thấp hơn EMA giá mở cửa là tín hiệu bán.

Tiếp theo, sử dụng độ lệch chuẩn để tính toán dải trên và dải dưới của kênh giá, và làm mịn chúng. Khi giá phá vỡ dải trên của độ lệch chuẩn là tín hiệu cắt lỗ, khi giá phá vỡ dải dưới của độ lệch chuẩn là tín hiệu chốt lời.

Cuối cùng, kết hợp các đường trung bình động với các khung thời gian khác nhau để xác định hướng xu hướng, kết hợp với chỉ báo Super Trend, tạo thành một đánh giá xu hướng ổn định.

Lợi thế của chiến lược

- Sử dụng chỉ báo Super Trend để xác định hướng xu hướng giá, tránh thua lỗ do đảo chiều xu hướng

- Đường trung bình động kết hợp với giá mở cửa hỗ trợ xác định thời điểm vào lệnh, tránh đột phá giả

- Kênh độ lệch chuẩn dự đoán các vùng hỗ trợ và kháng cự tiềm năng, thiết lập giá cắt lỗ và chốt lời

- Kết hợp nhiều khung thời gian để đánh giá hướng xu hướng, tăng tính ổn định

Rủi ro của chiến lược

- Chỉ báo Super Trend có độ trễ, có thể bỏ lỡ điểm chuyển đổi xu hướng

- Tín hiệu giao cắt của đường trung bình động có độ trễ, thời điểm vào lệnh không chính xác

- Phạm vi kênh độ lệch chuẩn quá cố định, không phản ánh được biến động thị trường theo thời gian thực

- Đánh giá từ nhiều khung thời gian có thể gây ra xung đột

Cách khắc phục rủi ro:

- Rút ngắn tham số Super Trend phù hợp để tăng độ nhạy

- Tối ưu hóa chu kỳ đường trung bình động hoặc thêm các chỉ báo khác để xác định thời điểm vào lệnh

- Điều chỉnh động các tham số kênh độ lệch chuẩn để phạm vi phù hợp với thị trường

- Xác định rõ logic đánh giá đa chu kỳ, xử lý xung đột có thể xảy ra

Hướng tối ưu hóa chiến lược

- Tối ưu hóa tham số Super Trend, tìm kiếm tổ hợp tham số tốt nhất

- Thử nghiệm kết hợp các chỉ báo khác với đường trung bình động để xác định thời điểm vào lệnh

- Thử nghiệm điều chỉnh động tham số kênh độ lệch chuẩn

- Kiểm tra các tổ hợp đa chu kỳ khác nhau để tìm chu kỳ phù hợp nhất

- Tối ưu hóa chiến lược cắt lỗ chốt lời nhằm nâng cao không gian lợi nhuận

Tổng kết

Chiến lược Siêu Xu Hướng V tích hợp các ưu điểm của xu hướng, đường trung bình, kênh độ lệch chuẩn, giúp xác định ổn định hướng xu hướng, chọn thời điểm vào lệnh phù hợp, và thiết lập cắt lỗ chốt lời theo vùng giá trong giao dịch ngắn hạn. Thông qua việc cải tiến như tối ưu hóa tham số, tối ưu hóa chỉ báo, tối ưu hóa cắt lỗ chốt lời, có thể nâng cao tính ổn định và khả năng sinh lời của chiến lược. Logic vững chắc và tư duy chặt chẽ của nó đáng để học hỏi và nghiên cứu.

/*backtest

start: 2022-10-11 00:00:00

end: 2023-10-17 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

// © theCrypster 2020

//@version=4

strategy(title = "Super trend V Strategy version", overlay = true, pyramiding=1,initial_capital = 1000, default_qty_type= strategy.percent_of_equity, default_qty_value = 100, calc_on_order_fills=false, slippage=0,commission_type=strategy.commission.percent,commission_value=0.075)- 1