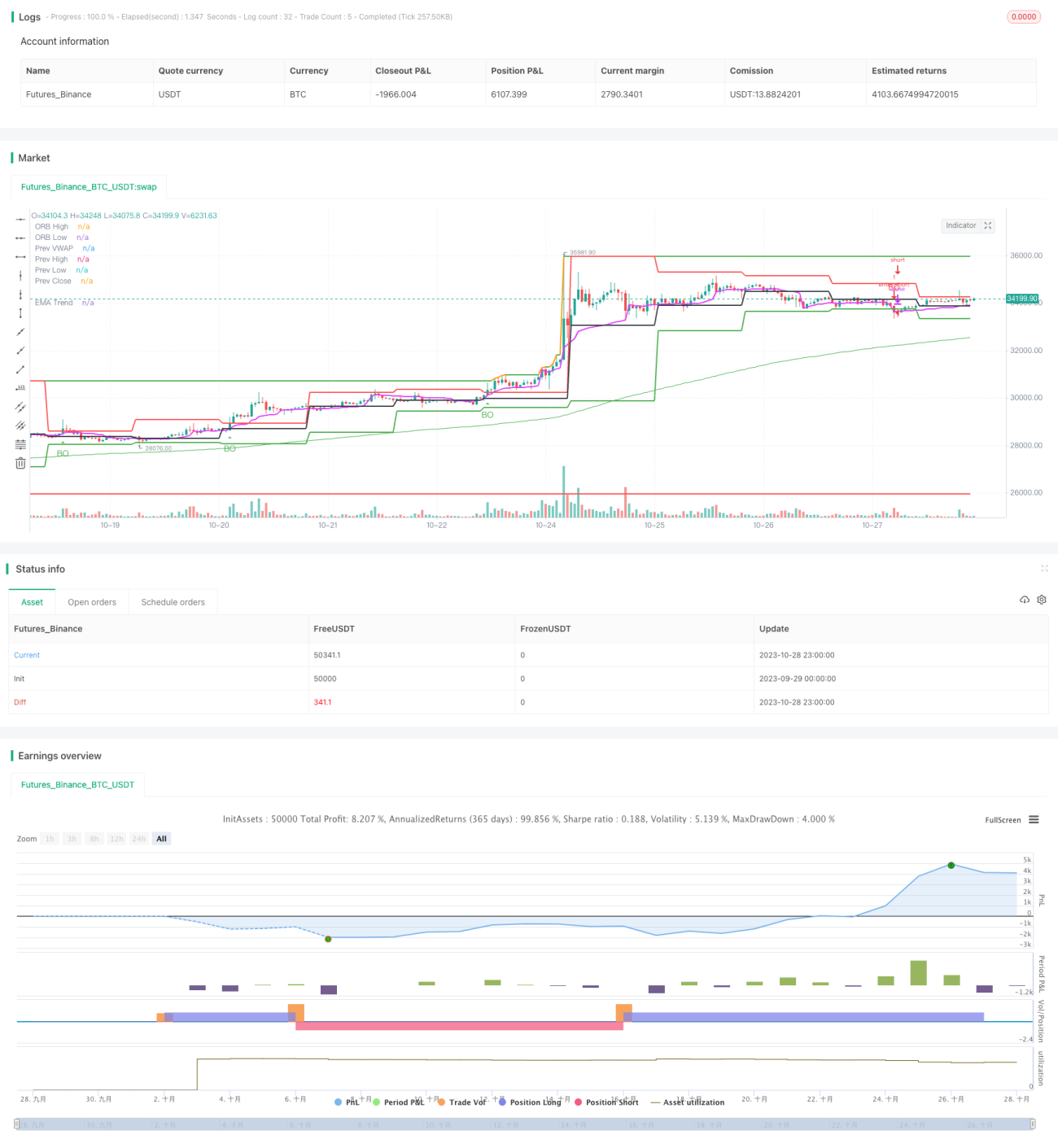

Chiến lược breakout đường trung bình động cấp cao

Tổng quan

Ý tưởng chính của chiến lược này là sử dụng sự phá vỡ đường trung bình động ở khung thời gian cao để thực hiện giao dịch theo xu hướng. Trên khung thời gian cao, khi giá phá vỡ lên trên hoặc xuống dưới đường trung bình động, có thể xác định được sự bắt đầu của xu hướng, khi đó có thể chọn hướng thích hợp để bám theo.

Nguyên lý chiến lược

Chiến lược này được phát triển bằng ngôn ngữ Pine Script, chủ yếu bao gồm các phần sau:

-

Tham số đầu vào

Xác định tham số chu kỳ đường trung bình động

period, giá trị mặc định là 200; xác định tham số chu kỳ thời gian nếntimeframe, giá trị mặc định là ngày "D". -

Tính toán đường trung bình động

Sử dụng hàm

ta.emađể tính đường trung bình động hàm mũ (Exponential Moving Average). -

Xác định sự phá vỡ

Sử dụng các hàm

ta.crossovervàta.crossunderđể xác định xem giá có phá vỡ lên trên hoặc xuống dưới đường trung bình động hay không. -

Vẽ tín hiệu

Khi xảy ra phá vỡ, vẽ các mũi tên hướng lên hoặc xuống trên nến.

-

Mở và đóng vị thế

Khi xảy ra phá vỡ, chọn hướng để mở vị thế, đóng vị thế khi đạt khoảng cách dừng lỗ gấp đôi.

Chiến lược này chủ yếu dựa vào khả năng xác định xu hướng của đường trung bình động ở khung thời gian cao, thông qua thao tác phá vỡ đơn giản để thực hiện bám theo xu hướng, thuộc loại chiến lược phá vỡ truyền thống.

Phân tích ưu điểm

Chiến lược này có những ưu điểm sau:

- Khái niệm đơn giản, dễ hiểu và dễ nắm bắt.

- Chỉ dựa vào một chỉ báo đường trung bình động, việc điều chỉnh tham số đơn giản.

- Hành động phá vỡ dễ hình thành xu hướng, không giao dịch quá thường xuyên.

- Khung thời gian cao hiển thị rõ ràng xu hướng lớn, khó bị ảnh hưởng bởi biến động ngắn hạn.

- Có thể cấu hình các tổ hợp chu kỳ thời gian khác nhau, thích ứng với nhiều loại sản phẩm.

- Có thể dễ dàng theo dõi nhiều sản phẩm cùng lúc, khó bị mắc kẹt đồng thời.

Phân tích rủi ro

Chiến lược này cũng tồn tại một số rủi ro:

- Tín hiệu phá vỡ có thể xảy ra phá vỡ giả, không thể lọc hiệu quả sự dao động của thị trường.

- Không thể tận dụng hiệu quả các cơ hội ngắn hạn để kiếm lời.

- Khi xác định sai hướng lớn, thua lỗ có thể khá nghiêm trọng.

- Khi chu kỳ đường trung bình động và chu kỳ giao dịch không khớp nhau, có thể xảy ra giao dịch quá mức hoặc bỏ sót.

- Không thể dừng lỗ theo thời gian thực, khả năng mở rộng thua lỗ khá lớn.

Các giải pháp cho rủi ro tương ứng bao gồm: kết hợp các chỉ báo xu hướng, thêm bộ lọc, rút ngắn chu kỳ nắm giữ phù hợp, điều chỉnh vị trí dừng lỗ động, v.v.

Hướng tối ưu hóa

Chiến lược này có thể xem xét tối ưu hóa từ các khía cạnh sau:

- Thêm tổ hợp các chỉ báo xu hướng, chẳng hạn như MACD, KD, v.v., để tăng độ tin cậy của các phá vỡ.

- Thêm các bộ lọc như khối lượng giao dịch hoặc dải Bollinger để tránh phá vỡ giả.

- Tối ưu hóa sự phù hợp của các tham số chu kỳ, làm cho chu kỳ nắm giữ phù hợp hơn với chu kỳ xu hướng.

- Thêm chiến lược dừng lỗ theo thời gian thực, sử dụng dừng lỗ bám theo để kiểm soát thua lỗ từng lệnh.

- Cân nhắc kết hợp kỹ thuật học máy để thực hiện tối ưu hóa tham số động.

- Thử nghiệm nhiều tổ hợp phân bổ tài sản để tăng tính ổn định tổng thể.

Tổng kết

Nhìn chung, chiến lược này tương đối đơn giản và thực dụng, thông qua phá vỡ đường trung bình động đơn giản để thực hiện bám theo xu hướng, dễ nắm bắt và có thể coi là một trong những chiến lược nhập môn giao dịch định lượng. Tuy nhiên, nó cũng tồn tại một số vấn đề, cần được cải thiện thông qua việc kết hợp các chỉ báo, tối ưu hóa tham số, dừng lỗ động, v.v., để chiến lược trở nên ổn định và hiệu quả hơn. Nó có không gian tối ưu hóa và khả năng mở rộng lớn.

- 1