Chiến lược giao dịch định lượng áp lực hai chiều

Tổng quan

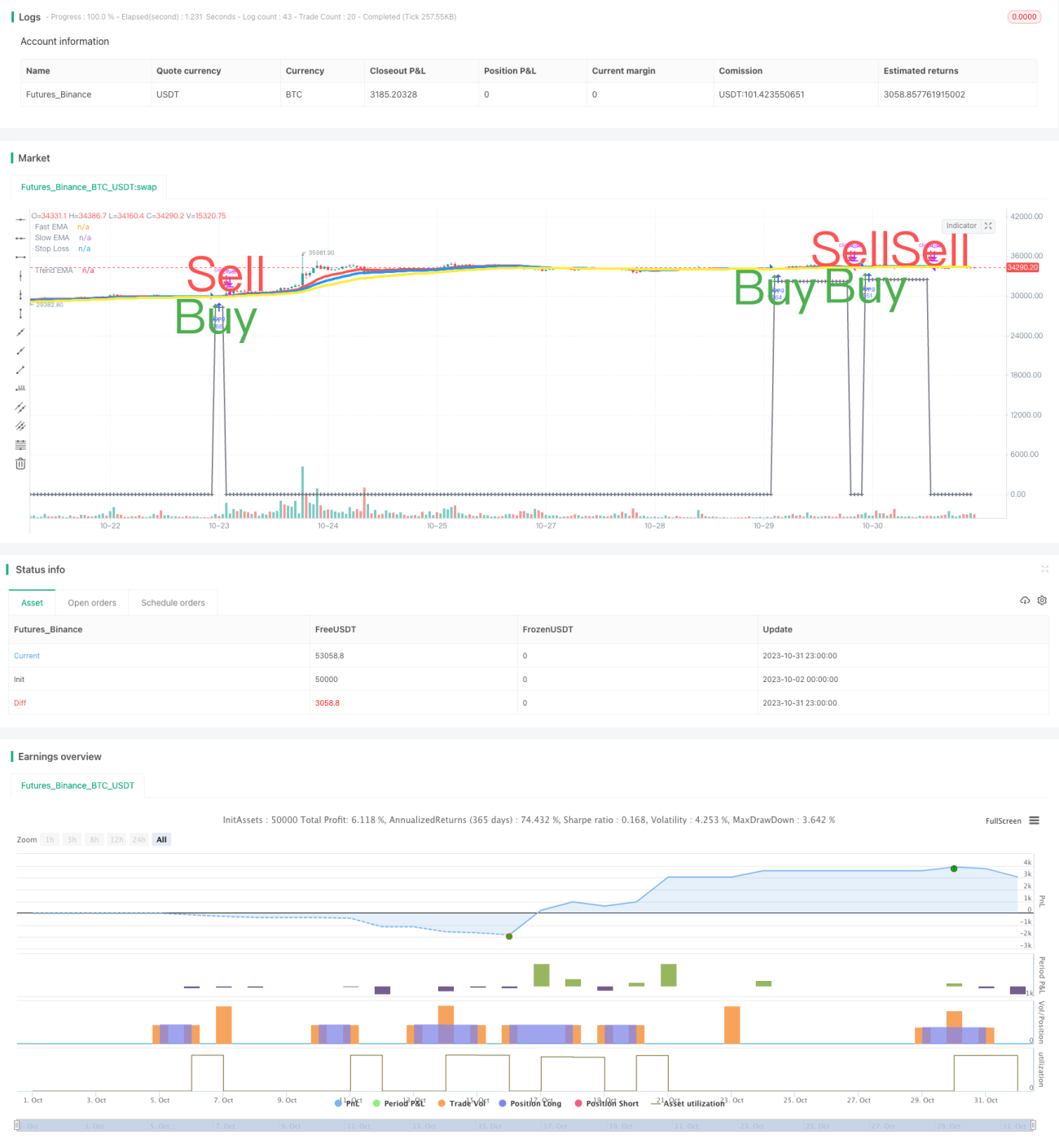

Chiến lược giao dịch định lượng áp lực hai chiều là một chiến lược theo xu hướng kết hợp chỉ báo ngẫu nhiên (Stochastic) và chỉ báo khối lượng. Chiến lược này chủ yếu sử dụng đường K và đường D của Stochastic cùng với chỉ báo khối lượng để tạo ra tín hiệu mua và bán, đồng thời bổ sung thêm tín hiệu từ giao cắt vàng và giao cắt tử thần của đường trung bình động.

Nguyên lý chiến lược

Tín hiệu mua

Logic kích hoạt chính của tín hiệu mua:

-

Đường K và đường D cùng phá xuống vùng quá bán (ví dụ 20), sau đó cắt lên nhau, đồng thời cả hai đường đều đang trong xu hướng tăng.

-

Khối lượng giao dịch cao hơn một ngưỡng nhất định (ví dụ 1,4 lần khối lượng trung bình).

-

Giá đóng cửa cao hơn giá mở cửa (nến trắng).

Các tín hiệu mua bổ sung có thể đến từ:

-

Giao cắt vàng: Đường EMA nhanh cắt lên đường EMA chậm, và cả hai đường trung bình đều đang tăng.

-

Đường K và đường D cùng từ vùng thấp đi vào vùng quá bán (ví dụ từ dưới 20 tăng lên vào khoảng 20-80).

Tín hiệu bán

Logic kích hoạt chính của tín hiệu bán:

-

Đường K và đường D cùng đi vào vùng quá mua (ví dụ 80).

-

Giao cắt tử thần: Đường EMA nhanh cắt xuống đường EMA chậm.

-

Đường K cắt xuống đường D, và cả hai đường đều đang trong xu hướng giảm.

Tín hiệu dừng lỗ

Đặt một tỷ lệ phần trăm nhất định (ví dụ 6%) so với giá mua làm đường dừng lỗ. Nếu giá phá vỡ đường này sẽ kích hoạt lệnh bán dừng lỗ.

Phân tích ưu điểm của chiến lược

- Sử dụng chỉ báo Stochastic kép để tránh tín hiệu giả.

- Kết hợp khối lượng để lọc nhiễu, đảm bảo tính xu hướng.

- Nhiều tín hiệu chồng lấp, tăng độ chính xác.

- Đường trung bình động hỗ trợ xác định xu hướng lớn.

- Thiết lập chiến lược dừng lỗ để kiểm soát rủi ro.

Ưu điểm 1: Chỉ báo Stochastic kép tránh tín hiệu giả

Một chỉ báo Stochastic đơn lẻ có thể tạo ra nhiều tín hiệu giả. Chiến lược này sử dụng tổ hợp đường K và đường D (đường trung bình động của đường K), giúp lọc hiệu quả các tín hiệu giả, đảm bảo độ tin cậy.

Ưu điểm 2: Khối lượng lọc nhiễu, đảm bảo tính xu hướng

Thêm điều kiện khối lượng làm tiêu chí hỗ trợ, yêu cầu khối lượng phải vượt một mức nhất định, từ đó lọc các điểm mua bán phi xu hướng có khối lượng thấp, giảm rủi ro bị kẹt hàng.

Ưu điểm 3: Nhiều tín hiệu chồng lấp, tăng độ chính xác

Chiến lược tổng hợp nhiều tín hiệu mua bán từ Stochastic, khối lượng và đường trung bình động. Các tín hiệu này cần cùng kích hoạt mới phát sinh tín hiệu giao dịch thực sự. Việc chồng lấp nhiều chỉ báo có thể tăng độ tin cậy của tín hiệu.

Ưu điểm 4: Đường trung bình động hỗ trợ xác định xu hướng lớn

Thêm quy tắc đường trung bình động, ví dụ chỉ xem xét tín hiệu mua khi cả hai đường trung bình nhanh và chậm cùng tăng. Điều này tránh mua ngược xu hướng hoặc đuổi đỉnh, xác định xu hướng từ khung thời gian lớn hơn.

Ưu điểm 5: Thiết lập chiến lược dừng lỗ kiểm soát rủi ro

Chiến lược có thiết kế tín hiệu dừng lỗ, nếu giá phá vỡ tỷ lệ nhất định so với giá mua thì tự động dừng lỗ. Điều này kiểm soát hiệu quả mức thua lỗ tối đa cho mỗi giao dịch.

Phân tích rủi ro

- Các tham số chiến lược cần tinh chỉnh cẩn thận, thiết lập không phù hợp có thể dẫn đến hiệu suất kém.

- Cài đặt điểm dừng lỗ cần xem xét rủi ro gap giá.

- Cần chú ý đến rủi ro thanh khoản của sản phẩm giao dịch.

- Cần lưu ý rủi ro về thứ tự của các chỉ báo đa khung thời gian.

Rủi ro 1: Các tham số chiến lược cần tinh chỉnh cẩn thận

Chiến lược này bao gồm nhiều tham số như tham số Stochastic, tham số đường trung bình, tham số khối lượng,... Các tham số này cần được tối ưu hóa cho từng sản phẩm khác nhau. Thiết lập không phù hợp có thể dẫn đến kết quả không như ý.

Rủi ro 2: Cài đặt điểm dừng lỗ cần xem xét rủi ro gap giá

Khi đặt điểm dừng lỗ, cần xem xét khả năng giá bị gap. Nếu điểm dừng lỗ quá gần giá mua, có thể bị gap gây ra dừng lỗ không cần thiết.

Rủi ro 3: Cần chú ý đến rủi ro thanh khoản của sản phẩm giao dịch

Đối với các sản phẩm có thanh khoản kém, quy tắc khối lượng có thể lọc bỏ quá nhiều tín hiệu. Khi đó cần giảm bớt ràng buộc về điều kiện khối lượng.

Rủi ro 4: Cần lưu ý rủi ro về thứ tự của các chỉ báo đa khung thời gian

Giữa các chỉ báo ở các khung thời gian khác nhau có thể xảy ra vấn đề không nhất quán về thứ tự, ảnh hưởng đến độ chính xác của tín hiệu. Cần xác minh tính nhất quán về thứ tự của điểm tín hiệu.

Hướng tối ưu hóa

Chiến lược này có thể được tối ưu hóa từ các khía cạnh sau:

-

Tối ưu tham số để tăng độ ổn định.

-

Thêm phương pháp học máy để điều chỉnh tham số động.

-

Tối ưu chiến lược dừng lỗ để giảm tỷ lệ dừng lỗ.

-

Thêm nhiều điều kiện lọc để giảm số lần giao dịch.

-

Thử nghiệm lệnh điều kiện hoặc chiến lược chốt lời để tăng tỷ suất lợi nhuận.

Hướng 1: Tối ưu tham số để tăng độ ổn định

Có thể sử dụng các phương pháp hệ thống hơn như giải thuật di truyền để tối ưu các tham số chính, đảm bảo tham số hoạt động ổn định trong các chu kỳ thị trường khác nhau.

Hướng 2: Thêm phương pháp học máy để điều chỉnh tham số động

Có thể huấn luyện mô hình đánh giá trạng thái thị trường theo thời gian thực, từ đó điều chỉnh tham số chiến lược, thực hiện tối ưu hóa tham số động.

Hướng 3: Tối ưu chiến lược dừng lỗ để giảm tỷ lệ dừng lỗ

Có thể nghiên cứu chiến lược dừng lỗ tốt hơn, vừa duy trì kiểm soát rủi ro vừa giảm thiểu các lệnh dừng lỗ không cần thiết, tăng không gian lợi nhuận.

Hướng 4: Thêm nhiều điều kiện lọc để giảm số lần giao dịch

Tăng cường điều kiện lọc một cách phù hợp để giảm số lần giao dịch, giảm tác động của chi phí giao dịch, giúp mỗi lần giao dịch có lợi nhuận cao hơn.

Hướng 5: Thử nghiệm lệnh điều kiện hoặc chiến lược chốt lời để tăng tỷ suất lợi nhuận

Dựa vào đặc điểm thị trường, thiết kế chiến lược lệnh điều kiện hoặc chiến lược chốt lời di động, vừa đảm bảo dừng lỗ vừa có thể đóng vị thế tại điểm lợi nhuận tối đa.

Tổng kết

Chiến lược này cân nhắc tổng thể nhiều khía cạnh như nhận định xu hướng, kiểm soát rủi ro, tần suất giao dịch,... Ưu điểm cốt lõi là sử dụng Stochastic kép kết hợp với chỉ báo khối lượng để nhận định xu hướng, cùng cơ chế dừng lỗ kiểm soát rủi ro. Bước tiếp theo có thể tối ưu hóa từ việc nâng cao độ ổn định tham số, điều chỉnh tham số động, giảm tỷ lệ dừng lỗ,... để chiến lược đạt được lợi nhuận ổn định trong nhiều môi trường thị trường hơn.

/*backtest

start: 2023-10-02 00:00:00

end: 2023-11-01 00:00:00

period: 1h

basePeriod: 15m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=3

// SW SVE - Stochastic+Vol+EMAs [Sergio Waldoke]

// Script created by Sergio Waldoke (BETA VERSION v0.5, fine tuning PENDING)

// Stochastic process is the main source of signals, reinforced on buying by Volume. Also by Golden Cross.- 1