Chiến lược chốt lời cắt lỗ thích ứng dựa trên khung thời gian kép và chỉ báo động lượng

Tổng quan

Chiến lược này sử dụng kết hợp khung thời gian kép và chỉ báo động lượng để thực hiện chốt lời cắt lỗ thích ứng. Khung thời gian chính theo dõi hướng xu hướng, khung thời gian phụ dùng để xác nhận tín hiệu. Khi cả hai khung thời gian cùng chiều, tín hiệu giao dịch được phát sinh. Sau khi vào lệnh, sử dụng phương pháp chốt lời dần dần để cập nhật mức chốt lời và cắt lỗ.

Nguyên lý chiến lược

-

Khung thời gian chính sử dụng chỉ báo hồi quy tuyến tính Squeeze Momentum (SQM) để đánh giá xu hướng, khung thời gian phụ sử dụng đường EMA của chỉ báo SQM để lọc nhiễu giả.

-

Khi SQM trên khung chính bứt phá lên và SQM trên khung phụ cũng hướng lên, vào lệnh mua; khi SQM trên khung chính bứt phá xuống và SQM trên khung phụ cũng hướng xuống, vào lệnh bán.

-

Sau khi vào lệnh, thiết lập mức chốt lời và cắt lỗ ban đầu dựa trên tham số đầu vào. Khi giá chạm mức chốt lời, cập nhật mức chốt lời và cắt lỗ. Cụ thể: mức chốt lời tăng dần theo tỷ lệ đặt trước, mức cắt lỗ giảm dần theo tỷ lệ, thực hiện chốt lời dần.

Ưu điểm của chiến lược

-

Khung thời gian kép lọc nhiễu giả, đảm bảo độ chính xác của tín hiệu.

-

Chỉ báo SQM xác định hướng xu hướng, tránh bị nhiễu thị trường làm phiền.

-

Cơ chế chốt lời cắt lỗ thích ứng, tối đa hóa lợi nhuận đã đạt được, kiểm soát rủi ro hiệu quả.

Phân tích rủi ro

-

Cài đặt tham số chỉ báo SQM không phù hợp có thể bỏ lỡ điểm đảo chiều xu hướng, gây thua lỗ.

-

Lựa chọn khung thời gian phụ không phù hợp, không lọc được nhiễu hiệu quả, dẫn đến giao dịch sai.

-

Mức cắt lỗ đặt quá rộng, mỗi lệnh thua lỗ có thể khá nặng.

Hướng tối ưu hóa

-

Tham số chỉ báo SQM cần điều chỉnh theo từng thị trường khác nhau để đảm bảo độ nhạy.

-

Khung thời gian phụ cũng cần thử nghiệm với các chu kỳ khác nhau, xem chu kỳ nào lọc hiệu quả nhất.

-

Mức cắt lỗ có thể thiết lập phạm vi dao động thay vì giá trị cố định, cho phép điều chỉnh theo biến động thị trường.

Tổng kết

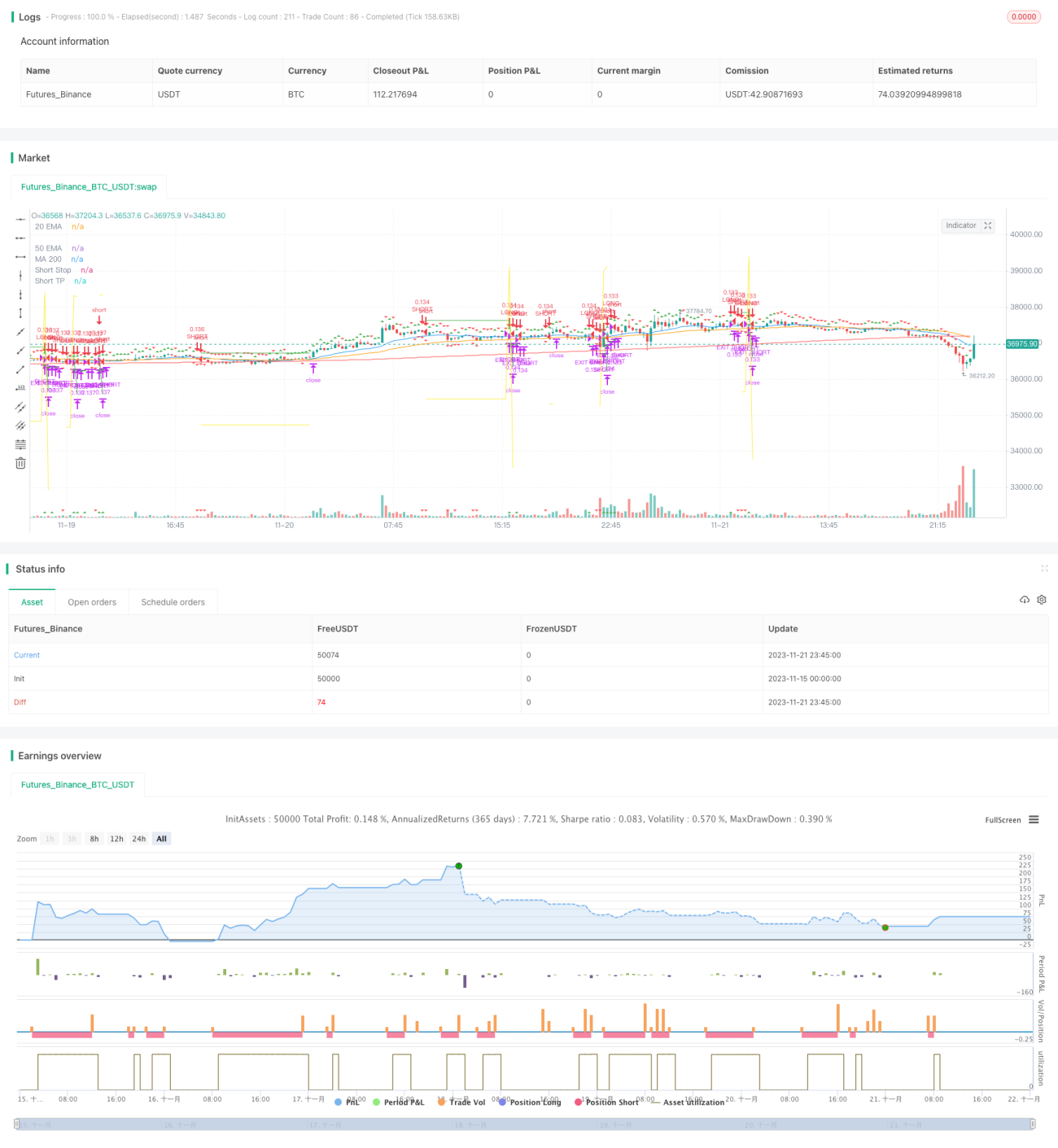

Nhìn chung, chiến lược này rất thực tế, kết hợp khung thời gian kép với chỉ báo động lượng để nhận diện xu hướng, đồng thời sử dụng cơ chế chốt lời cắt lỗ thích ứng để đạt lợi nhuận ổn định. Bằng cách tối ưu hóa tham số chỉ báo SQM, chu kỳ khung phụ và mức cắt lỗ, hiệu quả của chiến lược có thể được cải thiện, đáng để áp dụng và tối ưu trong giao dịch thực tế.

/*backtest

start: 2023-11-15 00:00:00

end: 2023-11-22 00:00:00

period: 15m

basePeriod: 5m

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=4

strategy("SQZ Multiframe Strategy", overlay=true, default_qty_type=strategy.percent_of_equity, default_qty_value=10)

fast_ema_len = input(11, minval=5, title="Fast EMA")

slow_ema_len = input(34, minval=20, title="Slow EMA")- 1