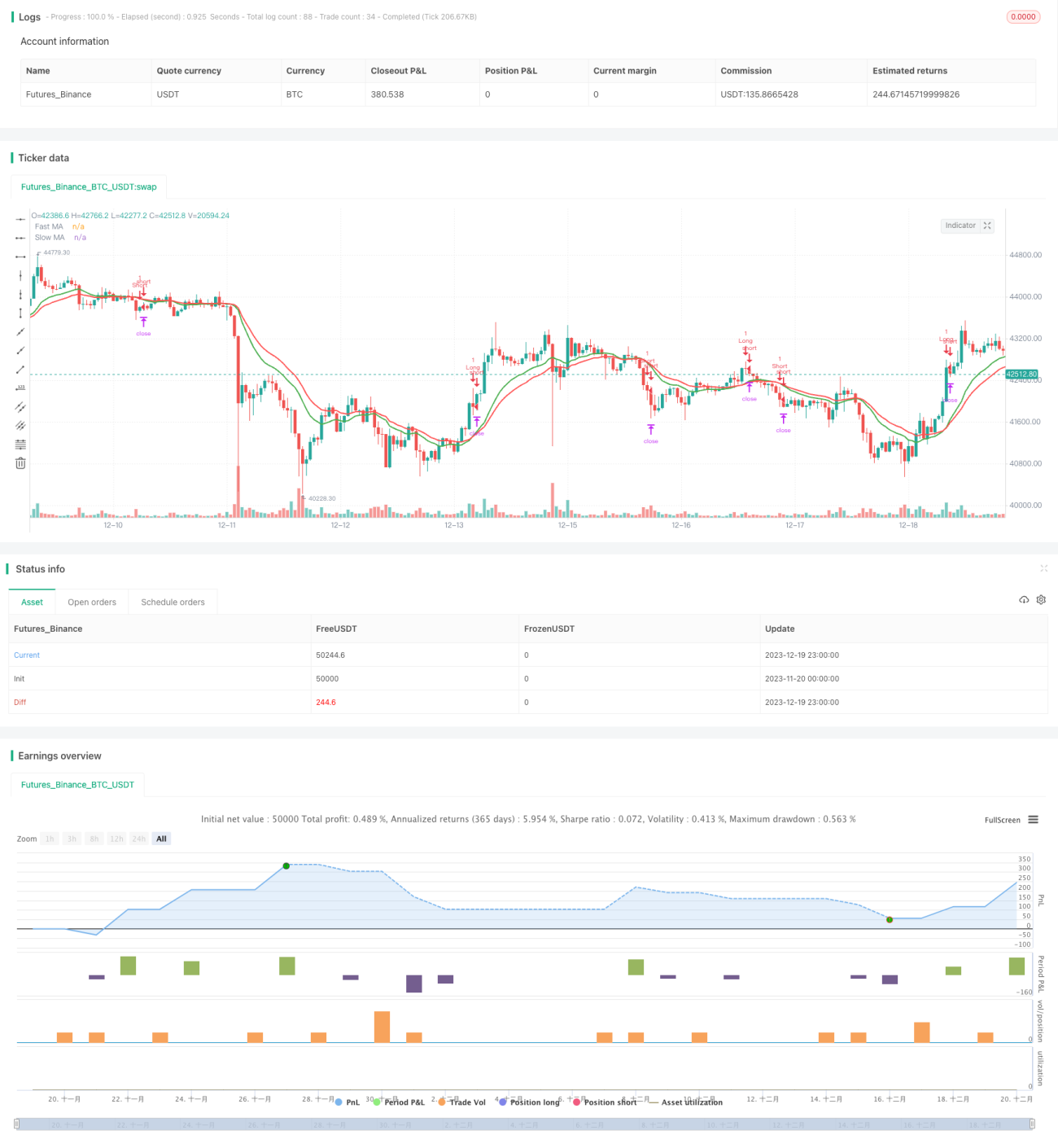

Chiến lược theo dõi xu hướng giao cắt hai đường MA

Tổng quan

Chiến lược này sử dụng phương pháp giao dịch theo xu hướng điển hình dựa trên giao cắt đường trung bình động kép, đồng thời kết hợp các cơ chế quản lý rủi ro như cắt lỗ, chốt lời và trailing stop, nhằm nắm bắt lợi nhuận lớn từ các đợt xu hướng.

Nguyên lý chiến lược

- Tính đường EMA trong khoảng thời gian nhanh n ngày, làm đường trung bình động ngắn hạn;

- Tính đường EMA trong khoảng thời gian chậm m ngày, làm đường trung bình động dài hạn;

- Khi đường trung bình ngắn hạn cắt lên trên đường trung bình dài hạn, mua lên; khi cắt xuống dưới, bán khống;

- Điều kiện đóng vị thế: cắt phá ngược chiều (ví dụ khi đang mua lên, nếu cắt phá ngược lại thì đóng vị thế).

- Sử dụng các biện pháp quản lý rủi ro như cắt lỗ, chốt lời, trailing stop.

Phân tích ưu điểm

- Sử dụng hai đường EMA, có thể đánh giá tốt điểm chuyển hướng xu hướng giá, nắm bắt xu hướng thị trường.

- Kết hợp cắt lỗ, chốt lời và trailing stop, có thể kiểm soát hiệu quả thua lỗ từng lệnh, khóa lợi nhuận, giảm drawdown.

- Có nhiều tham số có thể tùy chỉnh, có thể điều chỉnh và tối ưu theo từng sản phẩm và môi trường thị trường khác nhau.

- Logic chiến lược đơn giản rõ ràng, dễ hiểu và dễ sửa đổi.

- Hỗ trợ cả giao dịch mua lên và bán khống, có thể thích ứng với nhiều loại diễn biến thị trường.

Phân tích rủi ro

- Chiến lược đường trung bình động kép rất nhạy với phá vỡ giả (fake breakout), dễ bị mắc kẹt.

- Lựa chọn tham số không phù hợp có thể dẫn đến giao dịch quá thường xuyên, làm tăng chi phí giao dịch và tổn thất do trượt giá.

- Bản thân chiến lược không thể xác định điểm chuyển hướng xu hướng, cần kết hợp các chỉ báo khác để đánh giá hiệu quả hơn.

- Trong thị trường đi ngang (sideway), chiến lược dễ phát sinh tín hiệu giao dịch nhưng khả năng sinh lời thực tế kém.

- Cần tối ưu tham số để phù hợp với từng sản phẩm và môi trường thị trường.

Có thể giảm rủi ro bằng các cách sau:

- Kết hợp các chỉ báo khác để lọc nhiễu phá vỡ giả.

- Tối ưu hóa tham số, giảm tần suất giao dịch.

- Thêm các chỉ báo xác định xu hướng, tránh giao dịch trong thị trường đi ngang.

- Điều chỉnh quản lý vị thế, giảm rủi ro mỗi lệnh.

Hướng tối ưu

Chiến lược này có thể được tối ưu theo các hướng sau:

- Tối ưu chu kỳ tham số của đường EMA nhanh và chậm để phù hợp với các sản phẩm và môi trường thị trường khác nhau.

- Thêm các chỉ báo khác để đánh giá xu hướng và lọc tín hiệu phá vỡ giả. Điển hình có thể thêm MACD, KDJ, v.v.

- Có thể cân nhắc đổi EMA thành SMA hoặc đường trung bình động có trọng số WMA.

- Dựa trên ATR để điều chỉnh khoảng cách cắt lỗ một cách linh hoạt.

- Dựa trên phương pháp quản lý vị thế, có thể linh hoạt điều chỉnh khối lượng mỗi lệnh.

- Dựa trên tổ hợp các chỉ báo tương quan và biến động, thực hiện tối ưu tham số tự động thích ứng.

Tổng kết

Nhìn chung, chiến lược này là một chiến lược theo xu hướng dựa trên giao cắt hai đường EMA điển hình. Nó có ưu điểm nắm bắt các đợt xu hướng, đồng thời kết hợp các biện pháp quản lý rủi ro như cắt lỗ, chốt lời, trailing stop. Tuy nhiên, cũng tồn tại một số vấn đề điển hình như độ nhạy cao với nhiễu và thị trường đi ngang, dễ bị mắc kẹt. Bằng cách đưa vào các chỉ báo phụ trợ khác, tối ưu tham số, điều chỉnh động và kết hợp sử dụng, có thể tăng cường hiệu quả của chiến lược. Nhìn chung, nếu tham số được thiết lập phù hợp và phù hợp với diễn biến sản phẩm, chiến lược này có thể đạt được hiệu quả tốt.

- 1