Chiến lược theo dõi rủi ro thấp dạng kim tự tháp đáy

Chiến lược này kết hợp các chỉ báo khác nhau để xác định các điểm đáy tiềm năng trong biến động giá, đồng thời giảm thiểu rủi ro thông qua phương pháp xây dựng vị thế theo dõi kim tự tháp. Chiến lược cũng kết hợp các chức năng cắt lỗ, chốt lời, cắt lỗ di động, v.v., giúp kiểm soát rủi ro hiệu quả.

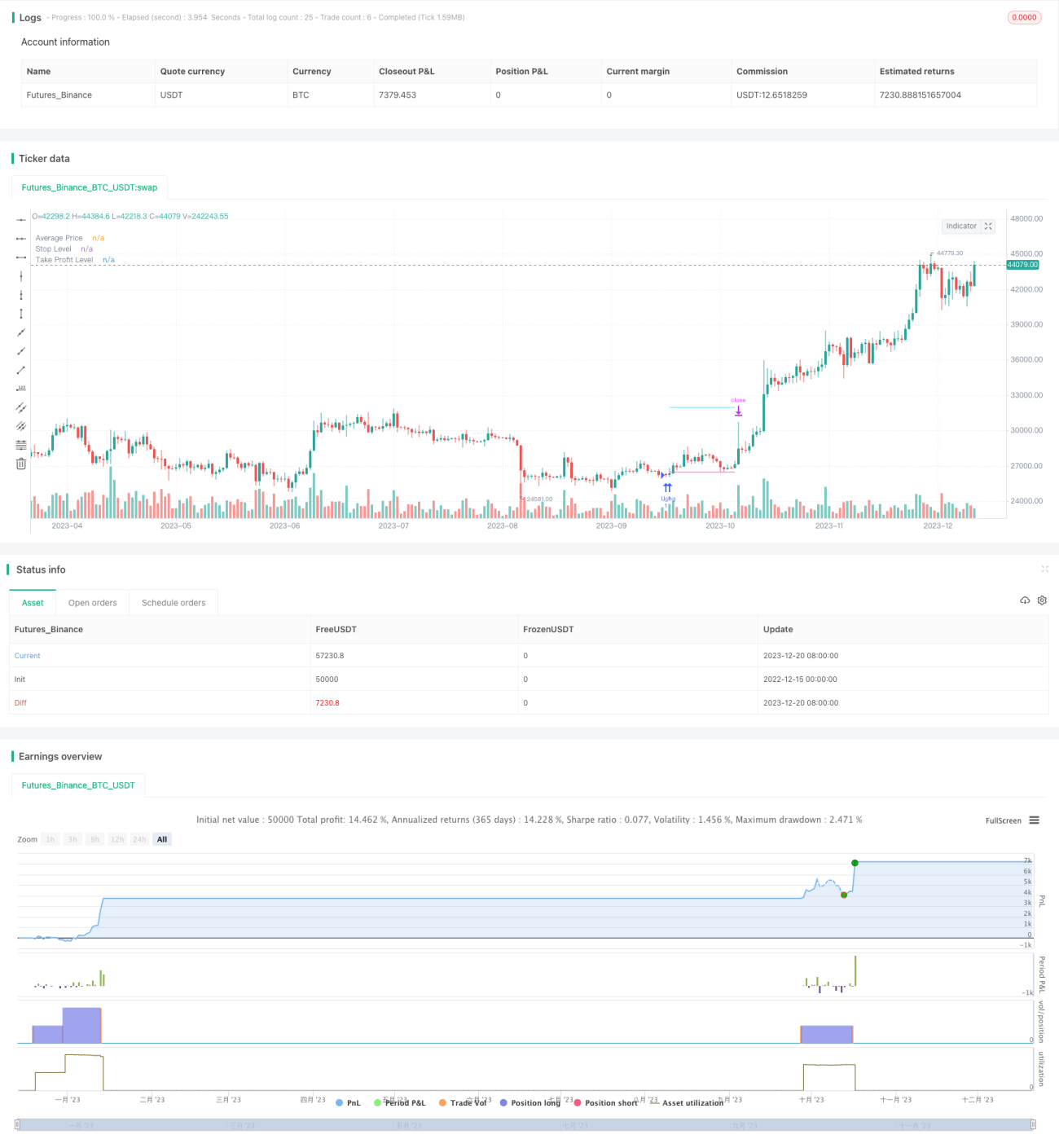

Tổng quan chiến lược

Chiến lược trước tiên sử dụng chênh lệch giữa RSI và EMA RSI để xác định các điểm đáy tiềm năng của giá. Để lọc các tín hiệu giả, chiến lược còn kết hợp đường trung bình động và chỉ báo Stochastic đa khung thời gian để xác nhận. Khi tín hiệu đáy được xác nhận, các lệnh mua sẽ được xây dựng dần ở mức giá thấp hơn một chút so với điểm đó, đây chính là ý tưởng theo dõi kim tự tháp. Chiến lược cho phép mở tối đa 12 lệnh theo dõi, số lượng mỗi lệnh sẽ tăng dần theo thứ tự, giúp phân tán rủi ro hiệu quả. Tất cả các lệnh sẽ thoát theo một mức cắt lỗ tổng thể, đồng thời cho phép thiết lập chốt lời riêng cho từng lệnh. Để kiểm soát rủi ro hơn nữa, chiến lược còn thiết lập mức cắt lỗ tổng thể dựa trên phần trăm vốn chủ sở hữu tài khoản.

Nguyên lý chiến lược

Chiến lược này chủ yếu bao gồm ba phần: mô-đun xác định đáy, mô-đun theo dõi kim tự tháp và mô-đun kiểm soát rủi ro.

Mô-đun xác định đáy sử dụng chênh lệch giữa chỉ báo RSI và EMA của nó để xác định các điểm đáy tiềm năng của giá. Để nâng cao độ chính xác, chỉ báo đường trung bình động và chỉ báo Stochastic đa khung thời gian cũng được đưa vào để lọc tín hiệu. Chỉ khi giá thấp hơn đường trung bình động và đường K của Stochastic dưới 30, tín hiệu đáy mới được xác nhận là hợp lệ.

Mô-đun theo dõi kim tự tháp là cốt lõi của chiến lược. Sau khi tín hiệu đáy được xác nhận, chiến lược sẽ mở lệnh đầu tiên tại mức giá thấp hơn điểm đáy đó 0,1%. Sau đó, nếu giá tiếp tục giảm và thấp hơn mức giá vào lệnh trung bình một tỷ lệ nhất định, sẽ tiếp tục thêm lệnh mua. Số lượng của các lệnh mới sẽ tăng dần, ví dụ lệnh thứ ba có số lượng gấp 3 lần lệnh đầu tiên. Phương pháp theo dõi kim tự tháp này giúp san bằng rủi ro. Chiến lược cho phép tối đa 12 lệnh theo dõi.

Mô-đun kiểm soát rủi ro chủ yếu bao gồm ba khía cạnh. Thứ nhất là cắt lỗ tổng thể, được tính dựa trên mức giá cao nhất trong một chu kỳ gần đây. Tất cả các lệnh sẽ cùng cắt lỗ theo mức này. Thứ hai là chốt lời độc lập cho từng lệnh, cho phép chốt lời theo một tỷ lệ nhất định so với giá vào lệnh. Thứ ba là cắt lỗ tổng thể dựa trên tỷ lệ vốn chủ sở hữu tài khoản, đây là biện pháp kiểm soát rủi ro mạnh nhất.

Ưu điểm của chiến lược

- Sử dụng theo dõi kim tự tháp giảm rủi ro cho từng lệnh riêng lẻ, đồng thời phân tán rủi ro tổng thể

- Kết hợp nhiều chỉ báo nâng cao độ chính xác của việc xác định đáy

- Các chức năng cắt lỗ tổng thể, chốt lời và cắt lỗ di động kiểm soát rủi ro hiệu quả

- Cơ chế cắt lỗ theo tỷ lệ vốn chủ sở hữu bảo vệ tài khoản khỏi thua lỗ lớn

- Có thể điều chỉnh thông số để tìm điểm cân bằng giữa rủi ro và lợi nhuận

Rủi ro của chiến lược

- Độ chính xác của việc xác định đáy vẫn còn hạn chế, có thể bỏ lỡ điểm vào lệnh tốt nhất hoặc vướng vào tín hiệu giả

- Khi thêm lệnh có thể gặp thị trường bất lợi, làm tăng thua lỗ

- Cần chu kỳ vận hành dài để thể hiện ưu điểm của chiến lược

- Cài đặt thông số không phù hợp có thể dẫn đến kiểm soát rủi ro không đủ

Để giảm thiểu các rủi ro trên, có thể tối ưu hóa từ các khía cạnh sau:

- Thay đổi hoặc bổ sung chỉ báo, nâng cao độ chính xác của việc xác định đáy

- Tối ưu hóa các thông số như số lượng lệnh, khoảng cách, biên độ chốt lời, v.v., giảm rủi ro cho từng lệnh riêng lẻ

- Rút ngắn biên độ cắt lỗ hợp lý để bảo vệ lợi nhuận

- Kiểm tra trên các loại tài sản khác nhau, chọn loại có tính thanh khoản tốt và biến động lớn

Hướng tối ưu hóa chiến lược

Chiến lược này vẫn còn không gian để tối ưu hóa thêm:

- Thử nghiệm đưa vào các công nghệ tiên tiến hơn như học máy để xác định đáy

- Điều chỉnh động các thông số như số lượng lệnh, biên độ cắt lỗ theo trạng thái thị trường

- Thêm chiến lược cắt lỗ trong khung giá để tránh thua lỗ lan rộng

- Thêm cơ chế vào lệnh lại

- Tối ưu hóa thông số chiến lược cho các loại tài sản như cổ phiếu và tiền điện tử

Tổng kết

Chiến lược này thông qua phương pháp theo dõi kim tự tháp đã giảm hiệu quả rủi ro cho từng lệnh đơn lẻ, các chức năng cắt lỗ tổng thể, chốt lời, cắt lỗ di động cũng đóng vai trò kiểm soát rủi ro tốt. Tuy nhiên, việc xác định đáy vẫn còn không gian tối ưu; nếu có thể đưa vào các công nghệ tiên tiến hơn, thêm chức năng điều chỉnh thông số động, kết hợp với tối ưu hóa thông số, tỷ lệ lợi nhuận/rủi ro của chiến lược này sẽ được cải thiện đáng kể.

- 1