Chiến lược giao dịch định lượng dựa trên phân rã mode thực nghiệm

Tổng quan

Chiến lược này dựa trên phương pháp Phân tích phương thức thực nghiệm (Empirical Mode Decomposition, EMD) để phân tách chuỗi giá, trích xuất các đặc trưng của các dải tần khác nhau, kết hợp với đường trung bình để tạo tín hiệu giao dịch. Chiến lược này chủ yếu phù hợp với giao dịch nắm giữ trung và dài hạn.

Nguyên lý chiến lược

- Sử dụng phương pháp EMD để thực hiện lọc dải thông (band-pass filter) trên giá, trích xuất các đặc trưng dao động trong giá.

- Tính toán đường trung bình động của chuỗi đỉnh và chuỗi đáy.

- Khi đường trung bình vượt quá một tỷ lệ nhất định so với đường đỉnh và đường đáy, sẽ tạo tín hiệu giao dịch.

- Thực hiện vị thế mua hoặc bán theo tín hiệu giao dịch.

Phân tích ưu điểm

- Phương pháp EMD có thể phân tách chuỗi giá hiệu quả, trích xuất các đặc trưng hữu ích.

- Đường đỉnh và đường đáy kiểm soát chiến lược chỉ giao dịch khi biến động giá đủ lớn.

- Kết hợp với đường trung bình, có thể lọc hiệu quả các tín hiệu phá vỡ giả.

Phân tích rủi ro

- Việc lựa chọn tham số của phương pháp EMD không phù hợp có thể dẫn đến quá khớp (overfitting).

- Cần chu kỳ dài để hình thành tín hiệu giao dịch, không thể thích ứng với giao dịch tần suất cao.

- Không thể đối phó với môi trường thị trường có biến động giá mạnh.

Hướng tối ưu hóa

- Tối ưu hóa tham số của mô hình EMD để cải thiện khả năng thích ứng với thị trường.

- Kết hợp với các chỉ báo khác làm tín hiệu dừng lỗ/chốt lời.

- Thử nghiệm các chuỗi giá khác nhau làm đầu vào chiến lược.

Tổng kết

Chiến lược này sử dụng phương pháp Phân tích phương thức thực nghiệm để trích xuất đặc trưng từ chuỗi giá, dựa trên các đặc trưng đó để tạo tín hiệu giao dịch, thực hiện một chiến lược giao dịch trung và dài hạn ổn định. Ưu điểm của chiến lược này là khả năng nhận diện hiệu quả các đặc trưng chu kỳ trong giá và đưa ra lệnh giao dịch trong các biến động lớn. Tuy nhiên, cũng tồn tại rủi ro nhất định, cần được tối ưu hóa thêm để thích ứng với môi trường thị trường phức tạp hơn.

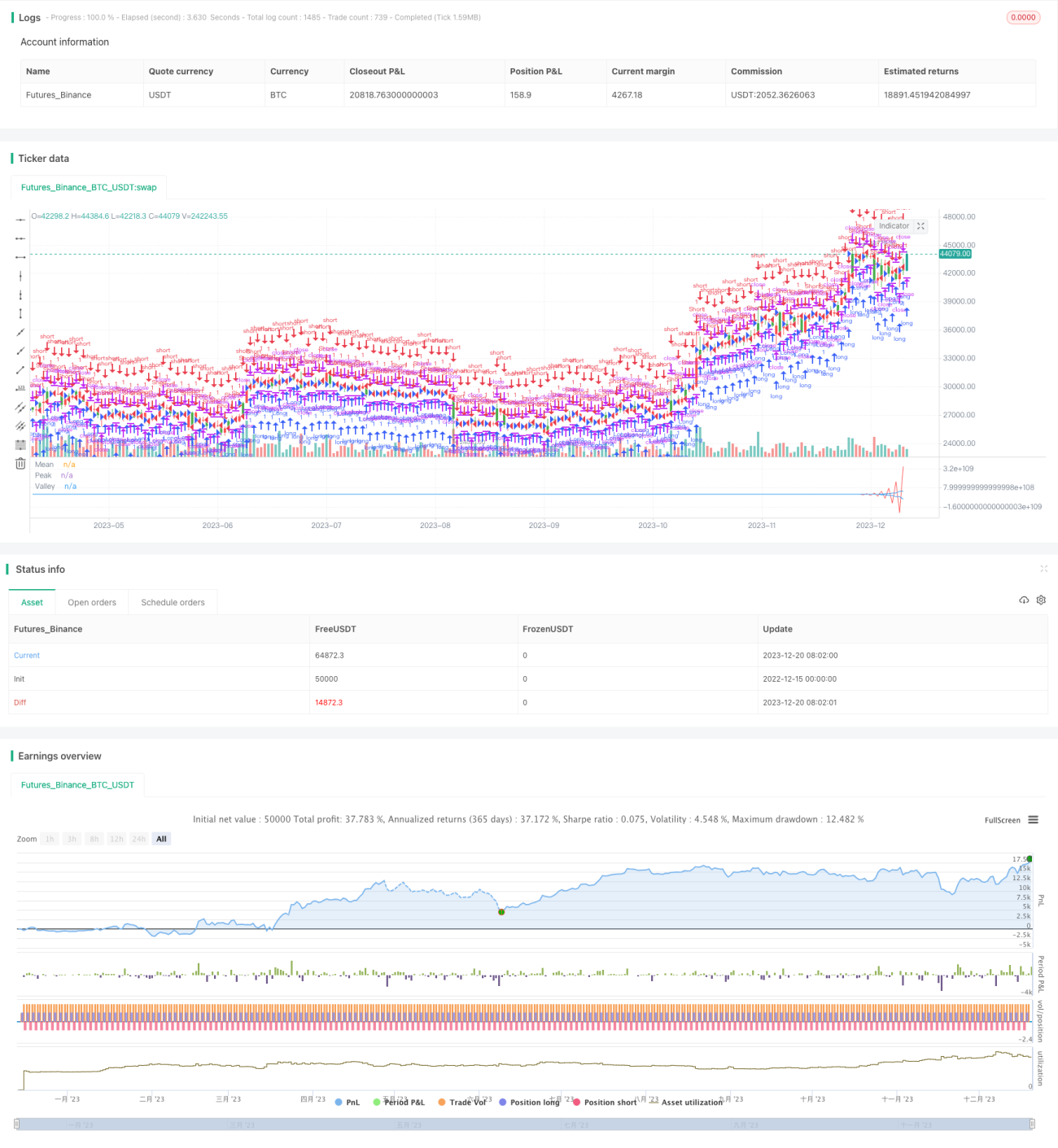

/*backtest

start: 2022-12-15 00:00:00

end: 2023-12-21 00:00:00

period: 1d

basePeriod: 1h

exchanges: [{"eid":"Futures_Binance","currency":"BTC_USDT"}]

*/

//@version=2

////////////////////////////////////////////////////////////

// Copyright by HPotter v1.0 12/04/2017

// The related article is copyrighted material from Stocks & Commodities Mar 2010- 1